Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI Fed Preview - June 2024: Analyst Outlook

MNI Fed Preview - June 2024: Analyst Outlook

- Note to readers: This is an update

to the MNI Fed preview published on Friday June 7. Please see Page 23-28 of

this document for sell-side analysts' outlooks for the June 12 FOMC decision and

future policy.

EXECUTIVE SUMMARY:

September In Focus

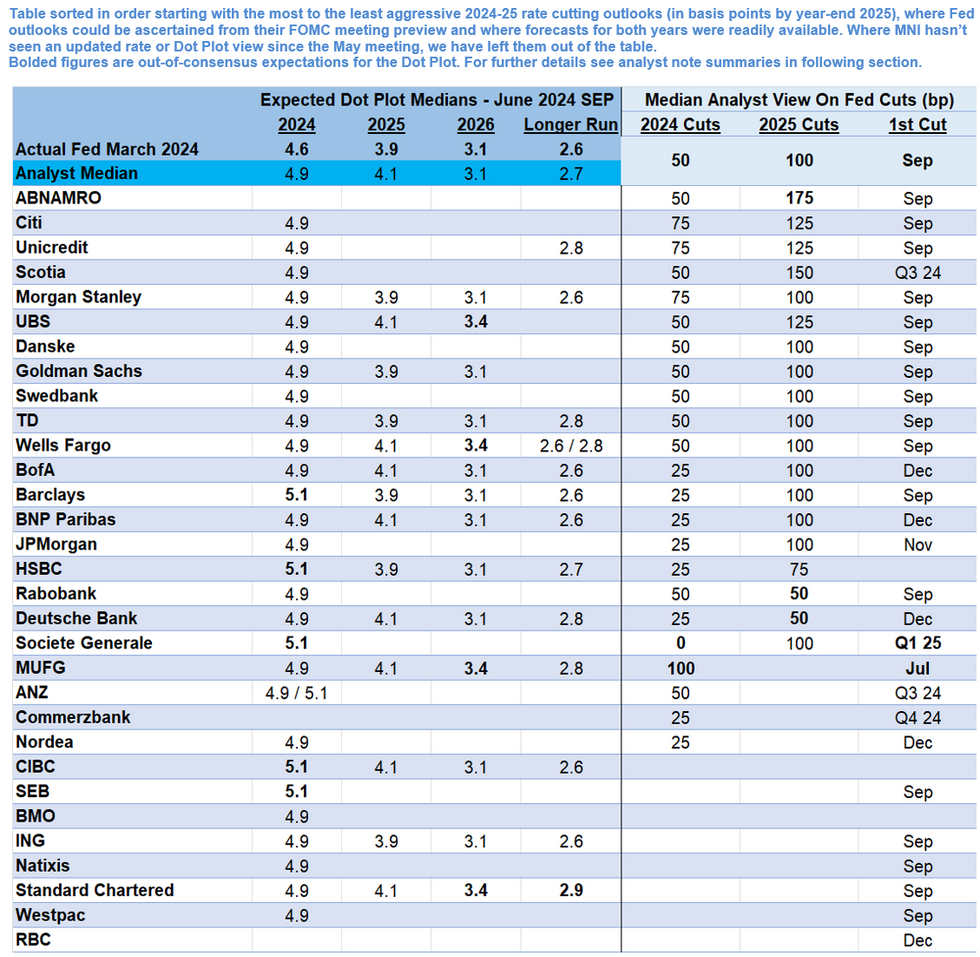

Sell-side Fed rate cut views continue to be pushed back as the June 2024 FOMC meeting approaches, now converging on September as the timing for the first cut. Ahead of March’s meeting, consensus was firmly on June.

- There are still one or two expectations for a July cut, but otherwise it’s nearly unanimous that the first Fed cut will come in Sep or Dec. JPMorgan eyes November, with SocGen the most hawkish on this front, eyeing Q1 2025.

- The median analyst sees 50bp of cuts this year, with a range of 0 (SocGen) to 100bp (MUFG) in cuts.

- For 2025, the general expectation is that the Fed will cut quarterly in 2025, though some see less (Deutsche/Rabobank, 50bp) or more (ABNAmro, 175bp; Scotia 150bp).

- For June’s Dot Plot, there are no expectations that the Fed will keep the 2024 rate median at 4.6% (3 cuts). The overwhelming consensus is that it will show 4.9% (2 cuts), with upside risks of a 1 cut median – the latter of which is the base case for a handful of analysts.

- Consensus is more split on the longer-run dot – our median of analysts’ expected medians is 2.7%, suggesting uncertainty over how much it will be raised at this meeting beyond March’s 2.56%. Some see 2.625% this time, some 2.75%, some higher, with many seeing it raised further yet over coming quarters.

- Most analysts expect the new economic projections to raise the 2024 core and headline PCE inflation forecasts by 0.1 to 0.2pp, with GDP growth downgraded slightly, and little change to 2025-26 estimates.

- There aren’t many changes expected to the FOMC statement, including on forward rate guidance.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK (ANALYST SECTION STARTS PG 23):

FedPrevJun2024 - With analysts.pdf

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok