Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

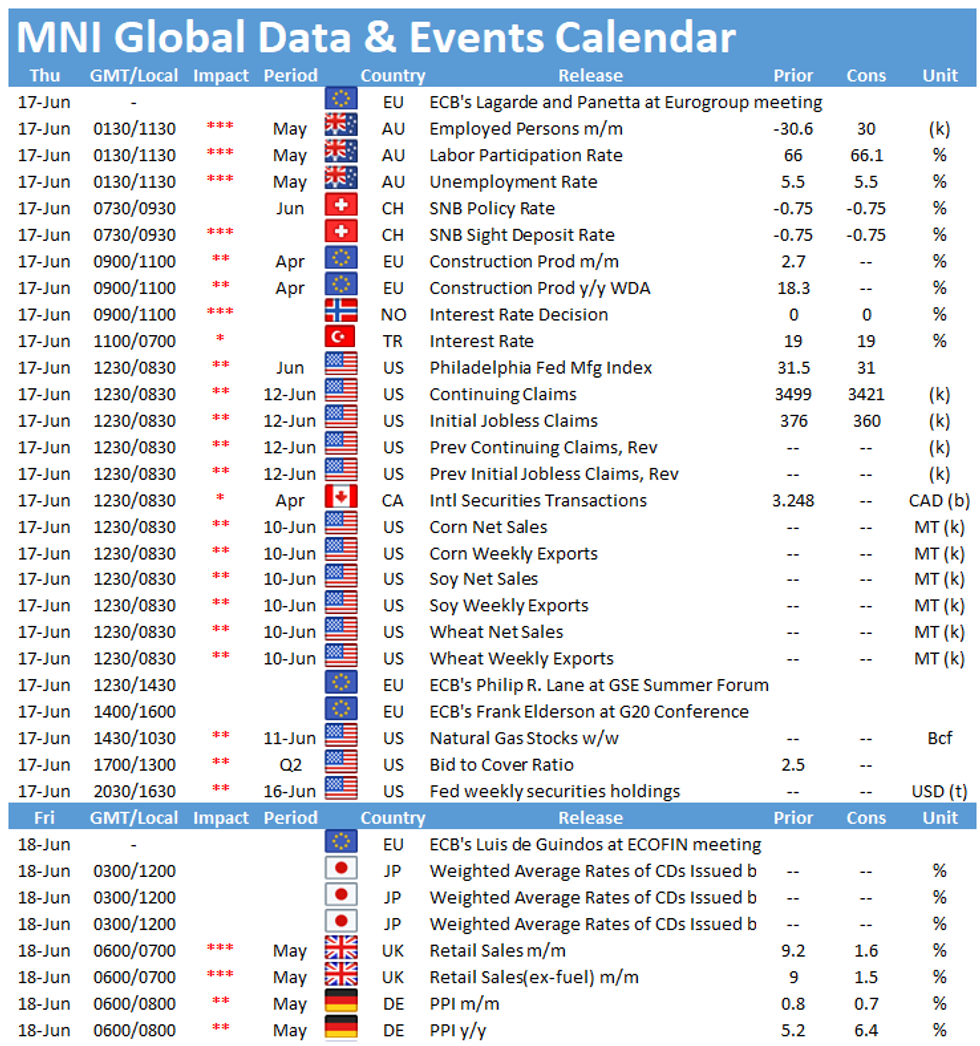

Thursday morning kicks off with the SNB's interest rate decision at 0830BST, followed by the release of EZ final inflation figures at 1000BST. In the US, the release of initial jobless claims will again be closely watched at 1330BST.

SNB rates seen unchanged

With the franc trading around its strongest level in four months at 1.09 to the euro, the Swiss National Bank is likely to repeat its assessment of the currency as "highly valued" and reaffirm its willingness to intervene if necessary at its June quarterly Monetary Policy Assessment on Thursday.

But the SNB, which dropped its commitment to intervene "more strongly" in FX markets in March, is under little pressure to move to keep the lid on the franc as it did last summer. It will leave its policy rate and interest on sight deposits at −0.75%.

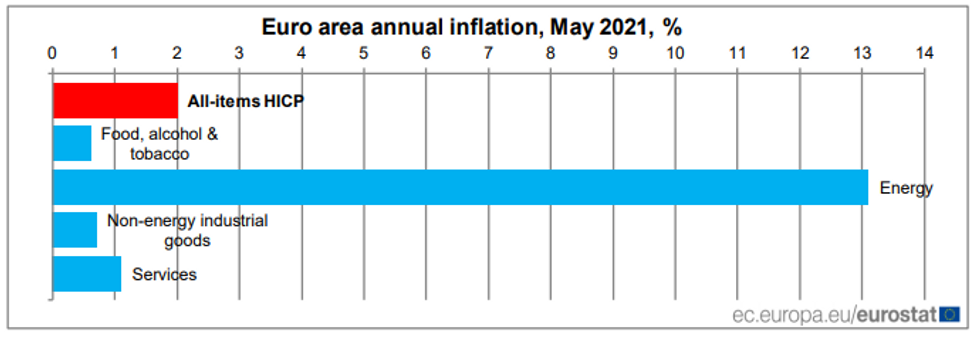

EZ inflation up in May

According to the flash estimate, EZ consumer prices rose 2.0% on an annual basis in May after increasing 1.6% in April. Markets expect the final print to register in line with the flash results. This would mark the first reading above the ECB's 2.0% target and the highest level since October 2018. May's increase was led by a sharp rise of energy inflation, up 13.1% in May after surging to 10.4% in April and was driven by base effects as energy prices fell sharply at the same time last year. While food inflation remained unchanged, prices for services and non-energy industrial goods accelerated.

The ECB expects inflation to rise significantly in 2021 and level off in 2022. The upward contributions in 2021 are coming from temporary factors such as a recovery of energy prices and the reversal of the German VAT cut. In 2022 these factors are expected to fade and the ECB's sees inflation at 1.5% in 2022 and at 1.4% in 2023.

Source: Eurostat

US jobless claims forecast to slow further

U.S. jobless claims filed through June 12 are expected to tick down, with Bloomberg forecasting a modest decline to 360,000 from 376,000 through June 5, a new pandemic low. Continuing claims filed through June 5 are projected to slow to 3,425,000, down from 3,499,000 through May 29.

The US labour market continues to be supported by the gradual reopening of the economy and the rapid pace of vaccinations. Additionally, many states plan to opt out of enhanced federal UI benefits, which should lead to another decline of both initial and continuing claims.

The main speakers to follow on Thursday include ECB's Christine Lagarde, Fabio Panetta, Philip Lane and Frank Elderson.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.