Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

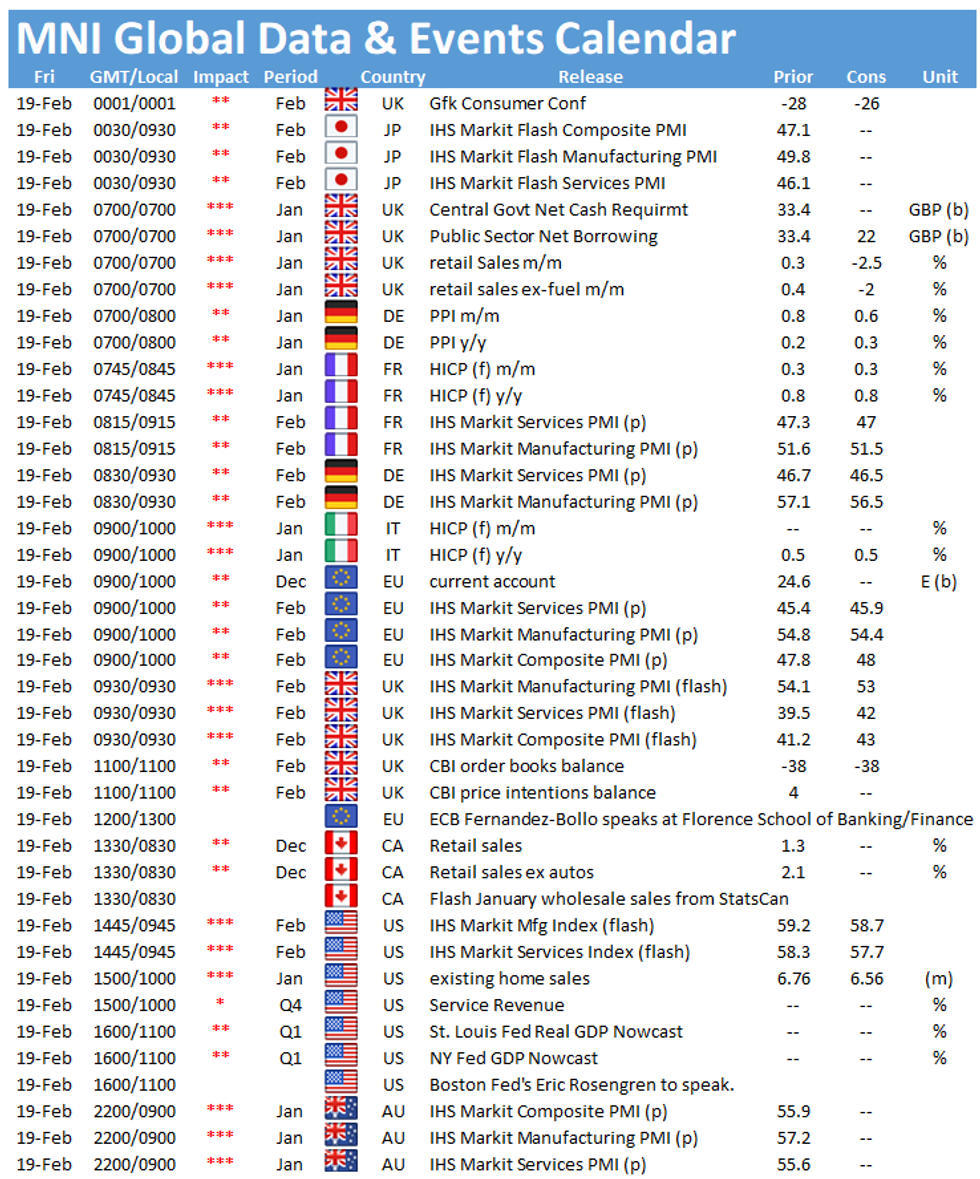

Friday sees a busy schedule in terms of data releases, starting with UK retail sales and public sector finances at 0700GMT. At 0815GMT the French flash PMI will be closely watched, followed by the German flash PMI at 0830GMT and the EZ index at 0900GMT. At 0930GMT the UK's flash PMI will be released before the US's PMI gets published at 1445GMT.

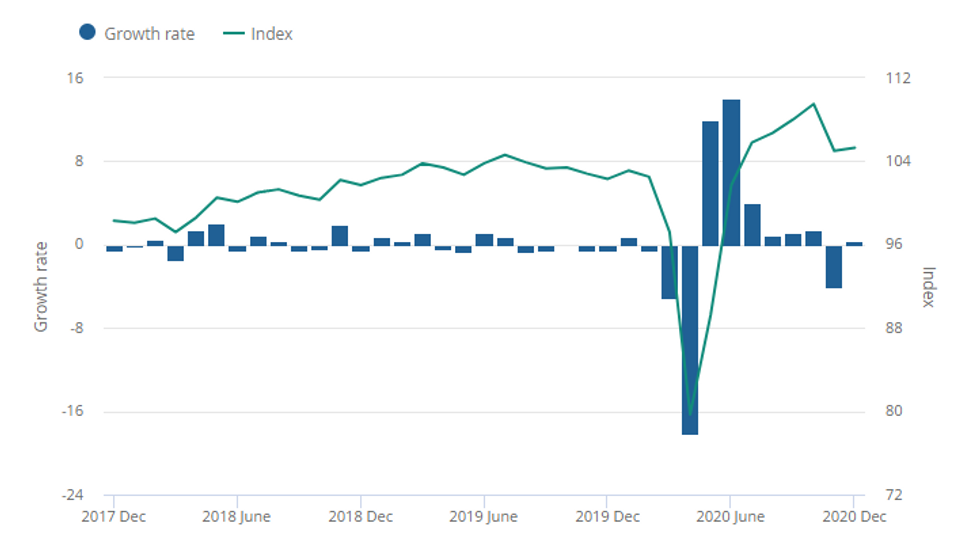

UK retail sales forecast to drop

The national lockdown led the closure of non-essential businesses at the end of December and shops are still shut at present. As a result, January retail sales are forecast to decline 3.0% on a monthly basis, while annual sales are expected to fall by 2.0%. However, retail sales plunged by 4.1% in November when shops were open the first five days of the months. In contrast, shops remained closed throughout January and MNI's Reality Check finds that sales could exceed the expected decline of 3.0%. Moreover, the BRC retail sales monitor fell to the lowest level since May with customers holding back on spending, especially on clothing and footwear.

Source: Office for National Statistics - Monthly Business Survey - Retail Sales Inquiry

Europe's flash PMIs to change only marginally

All services PMIs are expected to remain in contraction territory in February as most countries still have strict lockdown restrictions in place. The French and German services PMIs are both forecast to ease slightly in February to 47.0 and 46.5, respectively. On the other hand, the EZ's and the UK's indices are projected edge marginally higher by 0.5pt to 45.9 and 42.0, respectively. While France and Germany saw staff levels increase in January, the EZ overall and the UK recorded declines. However, firms in all countries remained optimistic regarding the outlook, reflecting the rollout of vaccination programs.

The manufacturing PMIs are holding up better with all four countries recording readings above the 50-mark. However, all January reports noted delivery delays and disruptions which in turn led to rising input costs. All four flash manufacturing PMIs are expected to ease further in February. The French index is seen at 51.5, the German index at 46.5 and the EZ manufacturing PMI is projected to drop to 54.4. Markets look for the UK's index to tick down to 53.0 in February.

US flash PMIs seen in expansion territory

Both the services and the manufacturing PMI increased in January with both indicators recording readings well above the 50-mark. The services PMI rose to 58.3 in January, however markets expect the index to ease to 57.7 in February. The manufacturing PMI is expected to slip to 58.7 in February, down from 59.2. January's survey noted severe delivery delays with lead times rising to a record high, which pushed up the headline index and led to higher input costs. Nevertheless, output and new orders grew strongly. Other survey evidence provides a mixed picture. While the Philadelphia Fed manufacturing index fell in February, the Empire State manufacturing index rose substantially.

The main events to look out for on Friday include speeches by ECB's Edouard Fernandez-Bollo, Richmond Fed's Tom Barkin and Boston Fed's Eric Rosengren.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.