Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

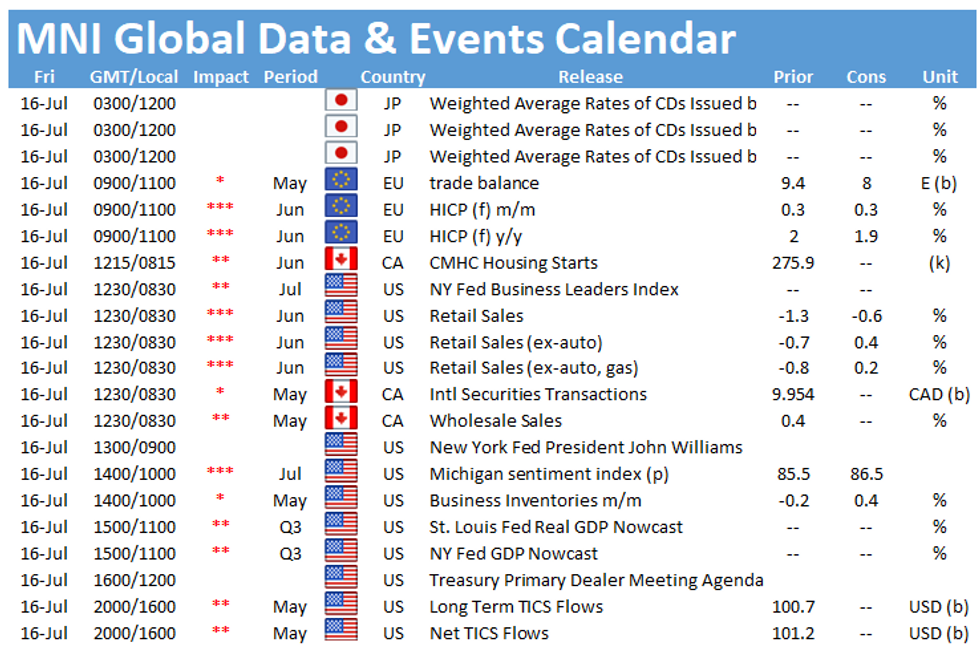

Friday throws up a quiet session in terms of European data. The final print of Eurozone inflation, published at 1000BST, is the highlight of the day this side of the Atlantic, whilst In the US, the release of retail sales at 1330BST and the Preliminary Michigan Sentiment index at 1500BST will be closely eyed.

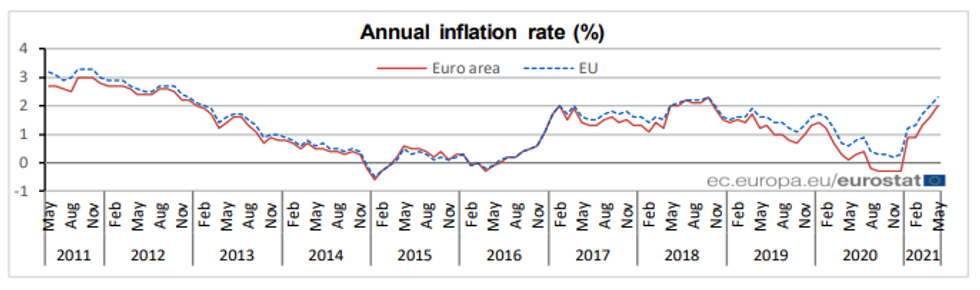

EZ final inflation seen at flash estimate

Eurozone flash inflation edged lower in June to 1.9%, down from 2.0% seen in May, as energy, services and food inflation decelerated. Only prices for non-energy industrial goods saw an increase in price growth in June. Markets expect the final print to register in line with the flash estimate.

The headline index is likely to see another uptick in July, due to base effects resulting from the German VAT cut last year. The ECB expects inflation to pick up significantly in 2021 but sees it moderating in the medium term as temporary factors fade out.

Source: Eurostat

US retail sales forecast to decline

U.S. retail sales likely dipped again in June as spending slowed further after a stimulus-fuelled surge in the spring. Total sales should fall 0.6% after dropping 1.3% in May, according to Bloomberg.

That should mostly be driven by a decline in vehicle sales, analysts say. Excluding car sales, retail sales should increase 0.4%, according to the Bloomberg consensus. Excluding both vehicle and gas station sales, retail sales are expected to increase 0.2% following May's 0.8% decline.

US preliminary Michigan sentiment index expected to rise

The University of Michigan consumer sentiment index rose to 85.5 in June, showing the second highest reading since the start of the pandemic. While Expectations increased in June compared to May, current conditions eased slightly. Meanwhile, inflation expectations for the year ahead dropped to 4.2%, down from 4.6% recorded in May. In July, markets expect the index to rise further to 86.5.

The only event scheduled on Friday is a speech by New York Fed's John Williams.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.