Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Europe's data calendar is again quiet on Friday with the only release scheduled being final inflation figures from Spain at 0800BST. The main data publications to follow in the US include the release of retail sales at 1330BST and industrial production figures at 1415BST.

Final Spanish inflation seen at flash result

Inflation accelerated significantly in April, mainly on the back of electricity prices and energy price base effects as fuel and oil prices fell sharply at the same time a year ago. The annual HICP rose to 1.9%, while the CPI increased to 2.2%. Core inflation on the other hand, eased 0.3pp to 0.0% in April, according to the flash result. Markets are looking for an unchanged reading for the final print.

Survey evidence indicates rising prices as well with the Spanish services PMI noting that higher operating costs led to an increase in output charges. However, inflation remains modest as competitive pressures remain and weigh on pricing power.

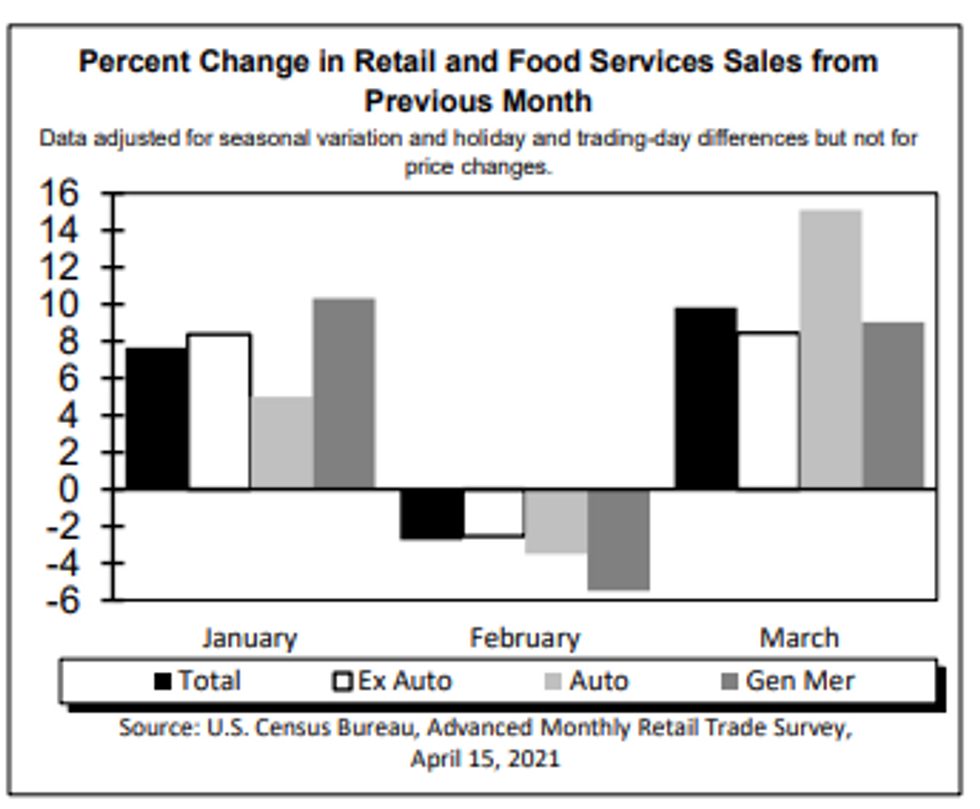

US retail sales forecast to rise at slower pace

Sales are expected to have slowed through April after a stronger-than-expected March reading of 9.8%, as highlighted in the latest MNI Reality Check, with Bloomberg forecasting a gain of 1.1%. Momentum from government stimulus and business re-openings that fuelled spending through March extended into April. Excluding motor vehicle sales, retail sales should have increased 0.8%, and excluding sales from both vehicles and gas stations, retail sales should rise 0.7%.

The conference board consumer confidence index noted that households are more optimistic about their income prospects, likely due to the improving job market and the recent stimulus checks. Moreover, the Michigan sentiment index is also forecast to rise in May, following an uptick in April. Both developments bode well with future gains of retail sales.

US industrial production expected to slow slightly

Monthly industrial production rebounded in March to 1.4% after dropping by 2.6% in the previous month. In March, manufacturing and mining output increased by 2.7% and 5.7%, respectively. On the other hand, utilities output dropped by 11.4% due to a change in demand for heating caused by temperature swings between February and March. In April, markets are looking for another gain of industrial production, although at a slower pace of 1.3%. Meanwhile, capacity utilisation is forecast to edge higher to 75.3% in April, up from 74.4% seen in the previous month. March's rate was still 5.2% below the long-run average.

Survey evidence is in line with market forecasts. The ISM manufacturing PMI eased slightly in April, however, the index remains well above the 50-mark, signalling expansion of business activity. The IHS manufacturing also suggests an expansion of output in April with the index ticking up slightly.

The only event scheduled on Friday is Dallas Fed's Rob Kaplan participating in a webinar.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.