Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MNI (Washington)

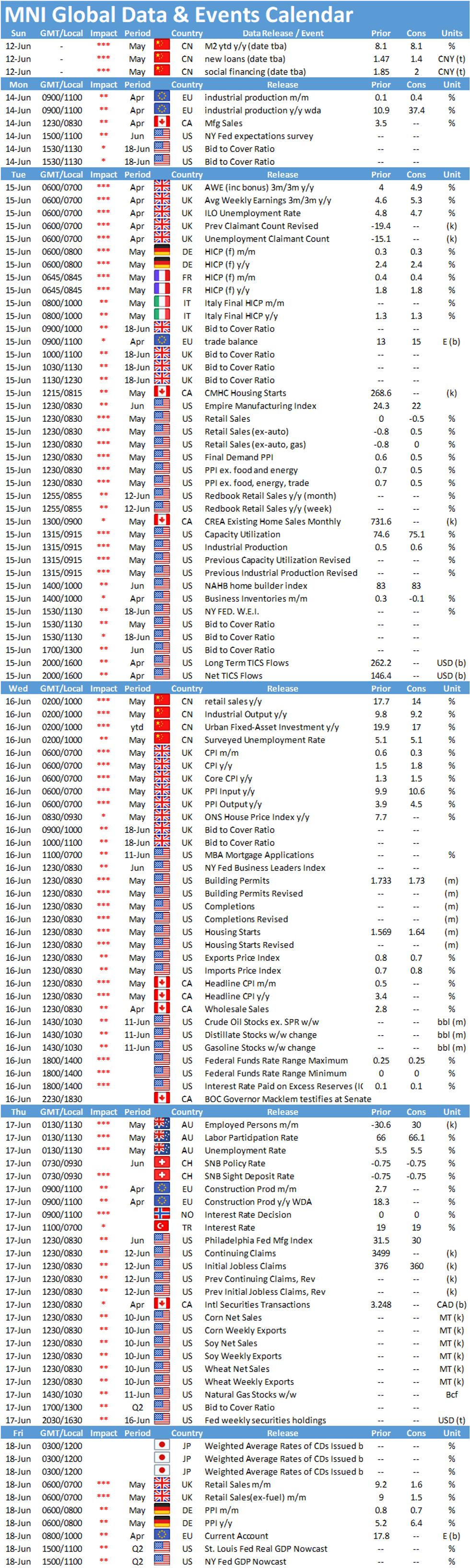

Key Things to Watch For:

- Tuesday, June 15 – U.S. Retail Sales

- Retail sales likely slipped further in May, with Bloomberg forecasting a decline of 0.5% after total sales were unchanged in April. Slowing vehicle sales through the month should drive that decline, analysts say.

- But excluding vehicle sales, retail sales in May were likely flat, according to Bloomberg, and retail sales excluding both vehicles and gas station sales should increase 0.5%. Restaurant spending is likely to lead that increase, with reservations nearing pre-pandemic levels in May, according to OpenTable. Sales at clothing stores should also see higher sales.

- Wednesday, June 16 – FOMC Policy Decision

- The FOMC is expected to cheer steady progress in the Covid recovery but maintain that it will still take time before the economy meets the Fed's "substantial further progress" bar for tapering asset purchases.

- Chair Jay Powell will likely play down any additional projections for liftoff by the end of 2023, though it's a close call whether the median dot will move forward into 2023.

- Forecasts for growth and inflation are expected to get a small upgrade, while projections for the labor market may be little changed.

- Friday, June 18 – Bank of Japan Policy Decision

- The Bank of Japan will likely stand pat on monetary policy Friday despite pointing to the current weaker-than-expected economy as the Covid-driven state of emergency is extended. Policymakers are set to downgrade their assessment on household spending as face-to-face services, particularly in the hospitality sector, remain weak.

- However, the overall assessment still points to a recovery in Q3 as the domestic vaccine rollout picks up steam and the global economy continues to recover.

- The BOJ is expected to extend its lending facility for smaller firms, currently due to end in September, taking a lead from the government that has already extended its zero interest, no collateral loans.

MNI Washington Bureau | +1 202-371-2121 | brooke.migdon@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok