Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY

Tsys have receded all the way back to early Monday levels late Thursday. After a higher start to the session, futures trade broadly weaker after the close on heavier volumes (TYZ over 1.8M) as equities stage a strong rebound (ESZ0 +60.0) after Wed's rout. Yld curves sharply steeper, especially in the short end.

- Despite the apparent risk-off unwinds risk-metrics have not changed, virus case counts continue to rise, Europe contemplates broader lock-down measures to contain, will red-zones in the US be far behind?

- Election angst: countdown to next Wed's presidential elections winding down, trade has grown choppy amid a mix of unwinds and cross-current flow. Equities rallied sharply, partially driven by "fear of missing out" FOMO buying on the bounce; sources cited ongoing Asia bank selling Tsys to draw down Tsy positions after risk parity sold both Tsys and equities on Wednesday. Deal-tied hedging and month end flow also relevant.

- Another auction tail, US Tsy $53B 7Y Note auction (91282CAU5) drew 0.600% rate (0.462% last month) vs. 0.587% WI; 2.24 bid/cover vs. 2.42 prior.

- The 2-Yr yield is up 0.4bps at 0.1505%, 5-Yr is up 4bps at 0.3701%, 10-Yr is up 5.7bps at 0.828%, and 30-Yr is up 5.8bps at 1.6115%.

TECHNICALS

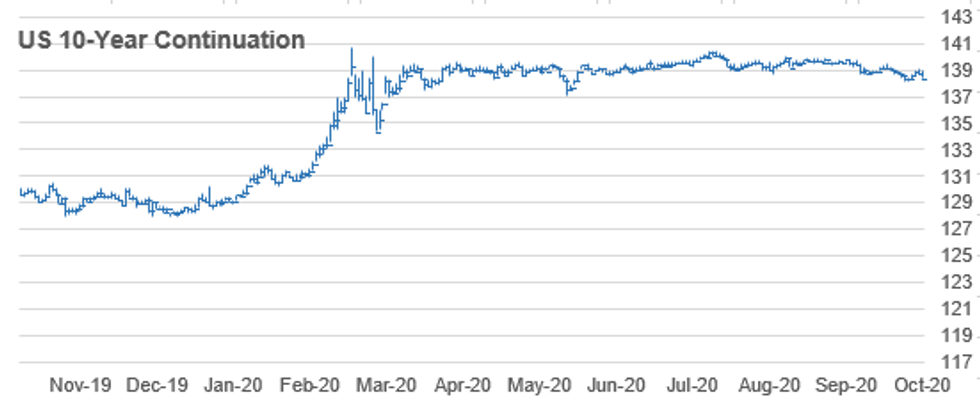

US 10YR FUTURE TECHS: (Z0) Focus Is On Trendline Resistance

- RES 4: 139-16+ Bear channel resistance drawn off the Aug 4 high

- RES 3: 139-14 High Oct 15 and a key resistance

- RES 2: 139-07+ High Oct 16

- RES 1: 139-02/03 Trendline resistance and High Oct 28

- PRICE: 138-17+ @16:20 GMT Oct 29

- SUP 1: 138-16+ Low Oct 29

- SUP 2: 138-05 Low Oct 23

- SUP 3: 138-04+ 1.00 proj of Aug 4 - 28 decline from Sep 3 high

- SUP 4: 138-00+ Bear channel base drawn off the Aug 4 high

After starting the session well, Treasuries hit reverse in the latter half of the US session, inching to the lowest levels since Monday at 138-16+. Nonetheless, the underlying outlook remains bullish and recent momentum behind the current rally suggests scope for further gains. Attention is on a short-term trendline resistance that intersects at 139-02. The trendline is drawn off the Oct 2 high. A break would strengthen the bullish theme and open 139-14, Oct 15 high.

AUSSIE 3-YR TECHS

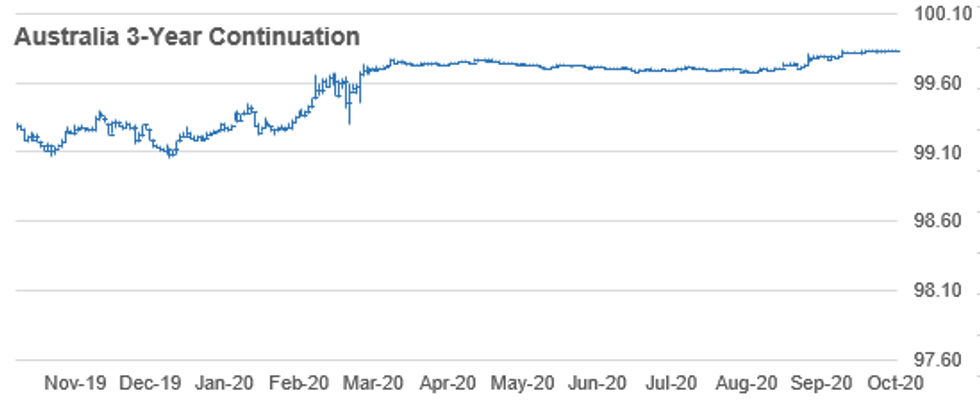

AUSSIE 3-YR TECHS: (Z0) Looking To Clear Resistance

- RES 3: 100.00 - Psychological round number

- RES 2: 99.886 - 3.0% Upper Bollinger Band

- RES 1: 99.845 - All time High Oct 20, 15 and the bull trigger

- PRICE: 99.840 @ 16:24 BST Oct 29

- SUP 1: 99.760 - Low Oct 1 and 2

- SUP 2: 99.705 - Low Sep 18, 21 and 22

- SUP 3: 99.675 - Low Sep 7 and key support

Aussie 3yr futures are largely unchanged and remain bullish. The price surge at the tail-end of September and early October confirmed bullish trend conditions. Recent activity is viewed as a pause in the uptrend and in pattern terms has taken on the appearance of a bull flag. This is a continuation pattern and reinforces current trend conditions. A break of 99.845, Oct 20 high and last week's high would open 99.889. Support is at 99.760.

AUSSIE 10-YR TECHS

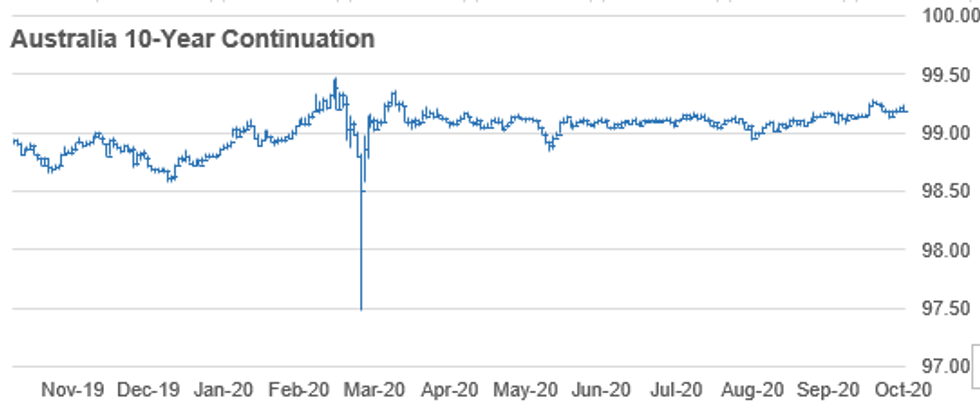

AUSSIE 10-YR TECHS: (Z0) Uptrend Remains Intact

- RES 3: 99.480 - High Mar 10 and the all-time high

- RES 2: 99.360 - High Apr 2 (cont)

- RES 1: 99.290 - High Oct 16

- PRICE: 99.190 @ 16:26 BST Oct 29

- SUP 1: 99.116 - 50-dma

- SUP 2: 99.055 - Low Sep 18 and 21

- SUP 3: 98.970 - Low Sep 8

Aussie 10y futures remain bullish despite this week's modest pullback. The break above 99.180, an area of congestion reflecting highs in Sep and early October confirmed a resumption of the uptrend that started on Aug 28. Attention turns to 99.300 and 99.360. The latter is the Apr 2 high (cont). The near-term bull trigger is 99.290, Oct 16 high. On the downside, firm trend support is at 99.075, Oct 5 low.

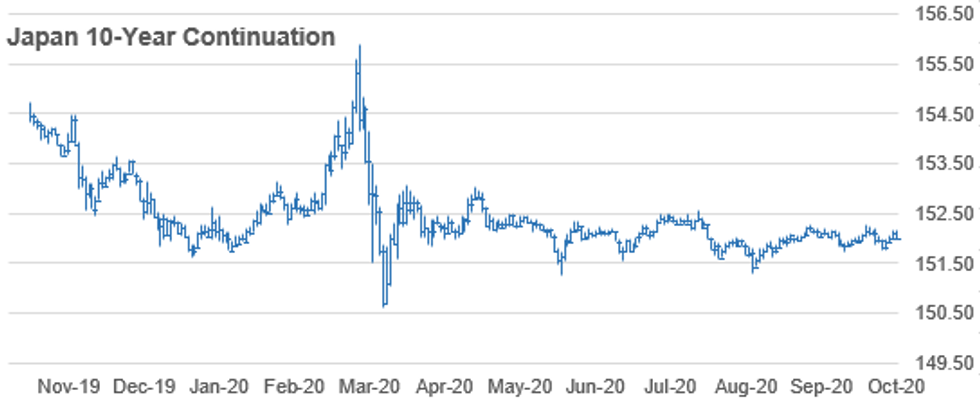

JGB TECHS

JGB TECHS: (Z0) Either Side of 152.00

- RES 3: 152.55 - High Aug 5 (cont)

- RES 2: 152.36- 3.0% Upper Bollinger Band

- RES 1: 152.29 - High Sep 24 and the bull trigger

- PRICE: 152.02 @ 16:28 BST Oct 29

- SUP 1: 151.75 - Low Oct 08 and trend support

- SUP 2: 151.54 - Low Sep 7

- SUP 3: 151.43 - Low Sep 1

Having topped 152.00 earlier in the week, reestablishing the recent positive outlook, JGBs faded slightly to trade either side of 152. Attention remains on 152.29, Sep 4 high, a key resistance and the bull trigger. A break of this level would confirm a resumption of the uptrend and open 152.36, a Bollinger band objective and 152.55, Aug 5 high (cont). On the downside, key trend support has been defined at 151.75, Oct 8 low.

TSY FUTURES CLOSE: Back Near Early Monday Levels

After a higher start to the session, futures trading broadly weaker after the bell on heavier volumes (TYZ over 1.8M) as equities stage a strong rebound after Wed's rout. Yld curves sharply steeper, especially in the short end. Update:

- 3M10Y +7.226, 74.155 (L: 66.17 / H: 74.829)

- 2Y10Y +6.013, 68.06 (L: 62.11 / H: 68.565)

- 2Y30Y +6.333, 146.653 (L: 140.371 / H: 147.891)

- 5Y30Y +2.376, 124.416 (L: 120.986 / H: 125.722)

- Current futures levels:

- Dec 2Y down 0.5/32 at 110-13.25 (L: 110-13.25 / H: 110-14)

- Dec 5Y down 4.25/32 at 125-20.25 (L: 125-19.75 / H: 125-26)

- Dec 10Y down 12.5/32 at 138-13 (L: 138-11.5 / H: 138-28.5)

- Dec 30Y down 1-5/32 at 172-28 (L: 172-20 / H: 174-13)

- Dec Ultra 30Y down 1-29/32 at 215-22 (L: 215-02 / H: 218-18)

US EURODLR FUTURES CLOSE: Long End Of Strip Weaker

Steady to mildly higher in the short end, broadly weaker out the strip; lead quarterly EDZ0 unchanged since 3M LIBOR set' steady at 0.21438% (-0.00212/wk).

- Dec 20 steady at 99.755

- Mar 21 +0.005 at 99.795

- Jun 21 steady at 99.80

- Sep 21 +0.005 at 99.805

- Red Pack (Dec 21-Sep 22) -0.01 to +0.005

- Green Pack (Dec 22-Sep 23) -0.025 to -0.015

- Blue Pack (Dec 23-Sep 24) -0.04 to -0.03

- Gold Pack (Dec 24-Sep 25) -0.06 to -0.05

US DOLLAR LIBOR: Latest settles

- O/N +0.00075 at 0.08100% (-0.00038/wk)

- 1 Month +0.00138 to 0.14913% (-0.00712/wk)

- 3 Month +0.00000 to 0.21438% (-0.00212/wk)

- 6 Month -0.00125 to 0.24288% (-0.00650/wk)

- 1 Year +0.00337 to 0.33100% (-0.00563/wk)

US TSYS: Short Term Rates

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $59B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $172B

- Secured Overnight Financing Rate (SOFR): 0.08%, $910B

- Broad General Collateral Rate (BGCR): 0.06%, $333B

- Tri-Party General Collateral Rate (TGCR): 0.06%, $309B

- (rate, volume levels reflect prior session)

- Tsy 20Y-30Y, $1.734B accepted vs. $3.942B submission

- Next scheduled purchase:

- Fri 10/30 1100-1120ET: TIPS 7.5Y-30Y, appr $1.225B

OUTLOOK: Look Ahead To Friday

- US Data/Speaker Calendar (prior, estimate)

- 30-Oct 0830 Sep total PCE price index (0.3%, 0.2%) 1.5% Y/Y

- 30-Oct 0830 Sep core PCE price index (0.3%, 0.2%) 1.7% Y/Y

- 30-Oct 0830 Sep current dollar PCE

- 30-Oct 0830 Sep personal income (-2.7%, 0.4%)

- 30-Oct 0830 Q3 ECI (0.5%, 0.5%)

- 30-Oct 0945 Oct MNI Chicago PMI (62.4, 58.0)

- 30-Oct 1000 Oct Michigan sentiment index (f) (81.2, 81.2)

- 30-Oct 1100 Q4 St. Louis Fed Real GDP Nowcast

- 30-Oct 1115 Q4 NY Fed GDP Nowcast

PIPELINE: Boeing Launched

Boeing Launched -- leads session but well off late Apr's massive $25B jumbo:

- Date $MM Issuer (Priced *, Launch #)

- 10/29 $4.9B #Boeing 4pt: $1B +3Y +180, $1.4B +5Y +240, $1.1B +7Y +265, $1.4B +10Y +280a (issued $25B via 7pt jumbo on April 30: $3B 3Y +425, +450: $3.5B 5Y, $2B 7Y, $4.5B 10Y and $5.5B 30Y, $3B 20Y +440, $3.5B 40Y +462.5)

- 10/29 $1.5B #Philip Morris $750M +5Y +58, $750M 10Y +103 (issued $2.25B on Apr 29: $750M each 3Y +100, 5Y +125 and 10Y +155)

- 10/29 $750M #Stanley Black & Decker 30Y +112.5

- 10/29 $650M #Baxter Int WNG 10Y +90

- 10/29 $500M *Swedish Export Credit Corporation (SEK) 2Y +5

- 10/29 $500M IFFIm 3Y Red S vaccine bond +18a

- 10/29 $Benchmark State Development & Inv 5Y +160a

EURODOLLAR/TREASURY OPTIONS

Eurodollar Options:

- +5,000 Blue Mar 90/93 3x2 put spds, 15.5

- +25,000 Blue Mar 92/93 put spds, 4.0

- +3,000 Blue Mar 90 puts, 2.0

- Overnight trade

- 2,000 Dec 96/97 2x1 put spds

- 2,000 Blue Jun 93/95 call spds

- 2,000 Dec 100 calls, cab

- 12,000 TYZ 134.5/135.5 put spds, 1

- 3,500 TYZ 136/138 put spds, 25/64

- +2,000 TYZ 137.5 puts, 15/64

- 2,000 USF 178/181 1x2 call spds, 6-7 earlier

- over 5,000 more TYZ 137.75/138.75 2x1 put spds, 4/64 add to recent +25k at 3/64

- +25,000 TYZ 137.75/138.75 2x1 put spds, 3/64 vs. 138-21/0.05%

- 7,500 TYZ 140 calls up to 11/64 on day

- -2,000 TYZ 136.75 puts, 7/64

- +5,500 TYZ 140 calls, 11/64

- Overnight trade

- 5,600 TYF 139.5/140.5 call spds, 15/64

- 7,100 TYZ 137 puts, 10-11

- +2,500 USZ 178/180 call spds, 22/64

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.