Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSY SUMMARY: Leaning Towards No-Deal Today

Markets buffeted by deal/no-deal stimulus headlines during second half. White House Speaker Pelosi remained optimistic, Sen Shelby expressed no optimism of a deal, while Sen Mitt Romney flat-out opposing $1.8T deal (or more) adding to late sales in equities. Stanza: Sen majority leader McConnell said would hold vote for stimulus if deal reached, vote does not mean pass.

- Astrazeneca vaccine trial to resume in a few days likely contributed to the midday bid in equities. Other salient headlines:

- GOOGLE ACCUSED BY U.S. OF ABUSING MARKET POWER IN LANDMARK CASE, Bbg

- BREXIT - UK PM JOHNSON TELLS GREEK PM: EU HAVE EFFECTIVELY ENDED NEGS, Rtrs

- Little to no react to multiple Fed speakers, Chicago Fed Pres Evans said stepping up asset purchases would have limited effect on already-low borrowing costs now, but the Fed could consider offering further accommodation later in the recovery.

- Trade volumes were about average, TYZ>1.1M after the bell, two-way flow from fast$, prop and bank portfolios in short end.

- The 2-Yr yield is down 0.2bps at 0.1431%, 5-Yr is up 0.2bps at 0.3361%, 10-Yr is up 2.2bps at 0.7907%, and 30-Yr is up 3.8bps at 1.5976%.

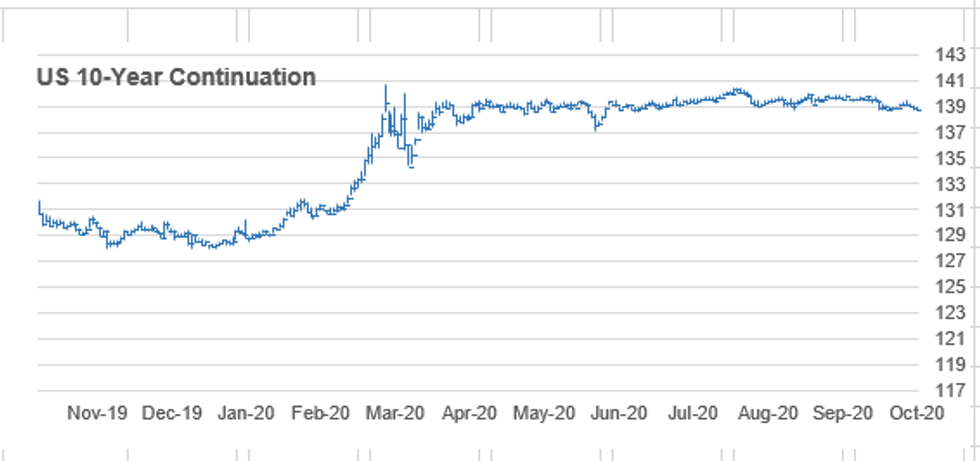

TECHNICALS, US 10Y Continuation

US 10YR FUTURE TECHS: (Z0) Attention Turns To Support

- RES 4: 139-25 High Oct 2

- RES 3: 139-17 76.4% retracement of Sep 29 to Oct 7 sell-off

- RES 2: 139-14 High Oct 15

- RES 1: 139-01+? High Oct 20

- PRICE: 138-26 @ 16:12 BST Oct 20

- SUP 1: 138-20+ Low Oct 7 and bull trigger

- SUP 2: 138-18+ Low Aug 28 and the bear trigger

- SUP 3: 138-16+ Low Jun 23 (cont)

- SUP 4: 138-12 61.8% retracement of the Jun - Aug rally (cont)

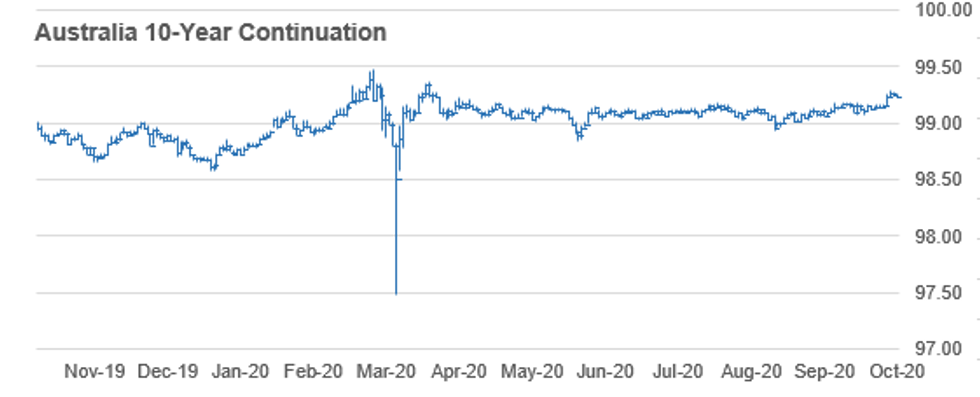

AUSSIE 3Y TECHS

AUSSIE 3-YR TECHS: (Z0) Looking To Clear Resistance

- RES 3: 100.00 - Psychological round number

- RES 2: 99.886 - 3.0% Upper Bollinger Band

- RES 1: 99.845 - All time High Oct 20, 15 and the bull trigger

- PRICE: 99.830 @ 16:15 BST Oct 20

- SUP 1: 99.760 - Low Oct 1 and 2

- SUP 2: 99.705 - Low Sep 18, 21 and 22

- SUP 3: 99.675 - Low Sep 7 and key support

AUSSIE 10Y TECHS

AUSSIE 10-YR TECHS: (Z0) Uptrend Remains Intact

- RES 3: 99.480 - High Mar 10 and the all-time high

- RES 2: 99.360 - High Apr 2 (cont)

- RES 1: 99.290 - High Oct 16

- PRICE: 99.235 @ 16:29 BST Oct 20

- SUP 1: 99.075 - Low Oct and the key support

- SUP 2: 99.055 - Low Sep 18 and 21

- SUP 3: 98.970 - Low Sep 8

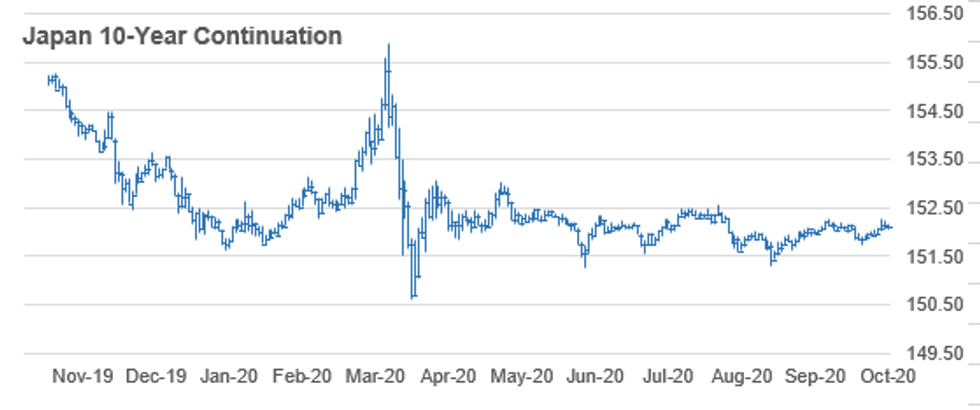

JGB TECHS

JGB TECHS: (Z0) Bullish Focus

- RES 3: 152.55 - High Aug 5 (cont)

- RES 2: 152.36- 3.0% Upper Bollinger Band

- RES 1: 152.29 - High Sep 24 and the bull trigger

- PRICE: 152.16 @ 16:35 BST Oct 20

- SUP 1: 151.75 - Low Oct 08 and trend support

- SUP 2: 151.54 - Low Sep 7

- SUP 3: 151.43 - Low Sep 1

US TSY FUTURES CLOSE: Deal/No-Deal Chop

Broadly weaker by the bell, just off late session lows on choppy trade. Markets buffeted by deal/no-deal stimulus headlines during second half. While House Sp Pelosi remains optimistic, Sen Shelby expressed no optimism of a deal, while Sen Mitt Romney flat-out opposing $1.8T deal (or more) adding to late sales in equities. Yld curves steeper, near highs, update:

- 3M10Y +1.58, 69.096 (L: 65.327 / H: 69.851)

- 2Y10Y +2.741, 64.723 (L: 61.316 / H: 65.19)

- 2Y30Y +4.269, 145.455 (L: 140.173 / H: 145.936)

- 5Y30Y +3.748, 126.104 (L: 121.595 / H: 126.398)

- Current futures levels:

- Dec 2Y up 0.12/32 at 110-13.75 (L: 110-13.25 / H: 110-13.8)

- Dec 5Y down 0.75/32 at 125-23.5 (L: 125-21.7 / H: 125-24.7)

- Dec 10Y down 6/32 at 138-23.5 (L: 138-21 / H: 138-28.5)

- Dec 30Y down 30/32 at 173-18 (L: 173-12 / H: 174-14)

- Dec Ultra 30Y down 2-9/32 at 215-31 (L: 215-21 / H: 218-03)

US EURODLR FUTURES CLOSE: Whites Hold Steady

Steady in the short end, Reds through Golds weaker -- moderate session lows. Lead quarterly back to steady after dipping briefly after 3M LIBOR rebounded +0.00712 from Mon's all-time low to 0.21575% (-0.00263/wk).

- Dec 20 steady at 99.765

- Mar 21 steady at 99.795

- Jun 21 steady at 99.805

- Sep 21 steady at 99.805

- Red Pack (Dec 21-Sep 22) -0.005 to steady

- Green Pack (Dec 22-Sep 23) -0.010 to -0.015

- Blue Pack (Dec 23-Sep 24) -0.015 to -0.035

- Gold Pack (Dec 24-Sep 25) -0.035 to -0.050

US DOLLAR LIBOR: Latest settles

- O/N -0.00050 at 0.08038% (-0.00075/wk)

- 1 Month +0.00237 to 0.14575% (-0.00563/wk)

- 3 Month +0.00712 to 0.21575% (-0.00263/wk)

- 6 Month -0.00237 to 0.25188% (-0.00562/wk)

- 1 Year -0.00262 to 0.33713% (+0.00213/wk)

US TSYS/SHORT END RATES

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 0.09% volume: $54B

- Daily Overnight Bank Funding Rate: 0.08%, volume: $155B

- Secured Overnight Financing Rate (SOFR): 0.09%, $903B

- Broad General Collateral Rate (BGCR): 0.06%, $344B

- Tri-Party General Collateral Rate (TGCR): 0.06%, $324B

- (rate, volume levels reflect prior session)

- Tsy 4.5Y-7Y, $6.001B accepted vs. $18.032B submission

- Next scheduled purchase:

- Wed 10/21 1010-1030ET: TIPS 7.5Y-30Y, appr $1.225B

OUTLOOK: Look Ahead To Wednesday

- US Data/Speaker Calendar (prior, estimate)

- 21-Oct 0700 16-Oct MBA Mortgage Applications (-0.7%, --)

- 21-Oct 1000 Clev Fed Pres Mester, mon-pol discussion

- 21-Oct 1030 16-Oct Distillate stocks w/w change

- 21-Oct 1030 16-Oct Gasoline stocks w/w change

- 21-Oct 1030 16-Oct crude oil stocks ex. SPR w/w

- 21-Oct 1130 TBA 105D Bill CMB 20-Oct

- 21-Oct 1130 TBA 154D Bill CMB 20-Oct

- 21-Oct 1200 Mn Fed Pres Kashkari, const amend for students

- 21-Oct 1200 Dallas Fed Pres Kaplan, Hispanic CoC

- 21-Oct 1300 US Tsy $22B 20Y-bond/R/O auction (912810SQ2)

- 21-Oct 1330 NY Fed VP Singh on Fed's copr credit facility

- 21-Oct 1400 Federal Reserve releases Beige Book

- 21-Oct 1645 StL Fed Pres Bullard, mon-pol, eco-outlook, Q&A

PIPELINE: Kingdom of Denmark Priced

- Date $MM Issuer (Priced *, Launch #)

- 10/20 $2B *Denmark 2Y +1

- 10/20 $3B United Airlines 4.1Y EETC deal (enhanced equipment trust certificates, corporate debt securities)

- Expected Wednesday

- 10/21 $Benchmark World Bank (IRBD) 5Y +11a

EURODOLLAR/TREASURY OPTIONS

Eurodollar Options:- +2,500 Blue Mar 91/93 put spds vs short Mar 96/97 put spds, 2.5 net db for conditional bear curve steepener

- +2,500 Blue Mar 91/93 put spds, 6.25 legged

- -5,000 Green Dec 92/93/95/96 put condors, 1.5

- +2,000 Red Mar'22 2x1 put spds, 1.75 legged

- -6,000 Green Nov 97 calls, 1.5 vs. 99.69/0.22%

- +2,000 Blue Mar 90/92 put spds, 4.25

- Overnight trade

- 1,000 Blue Nov 92/93/95/96 put condors

- 1,000 Blue Jan 93/96 comb or strangle

- +6,700 TYZ 137 puts, 11/64

- +8,000 FVZ 124 puts, 1.5

- >+65k TYZ 137.5/138/139 put trees, +50k at 3, trades up to 6/64

- over 1,000 USZ 175/177 1x2 cal spds, 5/64

- +6,000 TYX 138.5 puts, 6/64 vs. 138-25/0.25%

- Overnight trade

- -10,000 TYZ 140 calls, 15/64

- 2,500 TYX 139/139.25 call spds

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.