Highlights:

- Political risk remains the highlight, as French election campaign kicks off

- CAD rivals JPY, CHF as FX market's largest net short

- Empire manufacturing, ECB & Fedspeak take focus

- Treasuries are running weaker but scaling off overnight lows at the moment, mirroring similar moves on narrow ranges in EGBs as last week's French political cools slightly.

- Moderate Treasury futures volumes (TYU4<340k), with the Sep'24 10Y contract currently trading -3.5 at 110-23.5 vs. 110-18.5 low. Despite the decline, a bull cycle remains in play after the contract traded higher Friday, clearing resistance at 110-21, the Jun 7 high. Focus on 111-01 initial resistance - last Friday's high, followed by 111-09, April 1 high. Key support well below at 109-00+, the Jun 10 low.

- Cash yields are running mildly higher: 5s +.0069 at 4.2452%, 10s +.0135 at 4.2363%, 30s +.0273 at 4.3761%, while curves look steeper: 2s10s +1.572 at -46.993, 5s30s +1.872 at 12.774.

- This morning's data release is limited to US Empire State Manufacturing Survey General Business Conditions at 0830ET.

- Meanwhile, scheduled speakers include NY Fed Williams, Economic Club of NY moderated discussion at noon, Philly Fed Harker economic outlook at 1300ET, Fed Gov Cook acceptance remarks Marshall Forum later this evening at 2100ET.

- US Treasury supply kicks off the week with $70B each 13- and 26W Bill auctions at 1130ET, $60B 42D Bill CMB auction at 1300ET.

US TSY FUTURES: OI Points To Mix Of Short Cover & Long Setting During Friday's Rally

The combination of Friday’s rally in Tsy futures and preliminary OI data points to a mix of net short cover and long setting ahead of the weekend, with the former dominating in net OI DV01 equivalent curve terms.

- The apparent net long setting seen in TU and UXY futures was easily outweighed by the apparent net short cover seen elsewhere.

- A reminder that CFTC CoT positioning metrics continue to point to net short positioning in Tsy futures across the curve (as of Tuesday June 11), albeit skewed by basis trade positions.

- In terms of the drivers, the spill over from French political uncertainty dominated on Friday, underpinning Tsys. A very soft headline round of UoM sentiment readings also factored in.

| 14-Jun-24 | 13-Jun-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,086,359 | 4,007,980 | +78,379 | +3,021,673 |

| FV | 6,246,910 | 6,320,898 | -73,988 | -3,164,399 |

| TY | 4,385,060 | 4,423,335 | -38,275 | -2,499,569 |

| UXY | 2,058,595 | 2,053,967 | +4,628 | +418,794 |

| US | 1,654,928 | 1,660,974 | -6,046 | -809,320 |

| WN | 1,679,967 | 1,686,129 | -6,162 | -1,280,501 |

| Total | -41,464 | -4,313,323 |

STIR: OI Points To Mix Of Long Setting & Short Cover Across Much Of SOFR Futures Strip On Friday

The combination of Friday’s rally in most SOFR futures and preliminary OI data points to a mix of long setting and short cover across much of the strip.

- The only exceptions seemed to come via long cover in SFRH4 & M4, as those contracts settled incrementally lower on the day.

- Net short cover was seen in the remaining white contracts.

- Net long setting then provided the slightly more meaningful force in the reds.

- The greens seemed to see net short cover in all contracts.

- Net short cover seemed to provide the most meaningful net input for the blues, even though 3 out of the 4 contracts seemed to see net long setting on the day.

- French political uncertainty drove the rally in wider core global FI markets into the weekend, with a particularly soft round of UoM sentiment readings also noted.

- That left ~46bp of ’24 cuts priced into FOMC-dated OIS late last week, vs. ~36bp the week prior.

- The impact of last week's inflation data and French political uncertainty more than countered hawkish moves seen in the wake of the NFP report and FOMC decision.

| 14-Jun-24 | 13-Jun-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRH4 | 903,972 | 905,905 | -1,933 | Whites | -85,873 |

| SFRM4 | 1,297,643 | 1,344,062 | -46,419 | Reds | +5,807 |

| SFRU4 | 1,118,970 | 1,140,760 | -21,790 | Greens | -39,379 |

| SFRZ4 | 1,039,074 | 1,054,805 | -15,731 | Blues | -3,598 |

| SFRH5 | 818,698 | 826,477 | -7,779 | ||

| SFRM5 | 787,184 | 756,152 | +31,032 | ||

| SFRU5 | 632,106 | 652,641 | -20,535 | ||

| SFRZ5 | 807,930 | 804,841 | +3,089 | ||

| SFRH6 | 567,261 | 581,777 | -14,516 | ||

| SFRM6 | 483,209 | 502,092 | -18,883 | ||

| SFRU6 | 407,463 | 407,859 | -396 | ||

| SFRZ6 | 355,453 | 361,037 | -5,584 | ||

| SFRH7 | 255,660 | 255,086 | +574 | ||

| SFRM7 | 190,636 | 199,523 | -8,887 | ||

| SFRU7 | 165,636 | 164,888 | +748 | ||

| SFRZ7 | 163,042 | 159,075 | +3,967 |

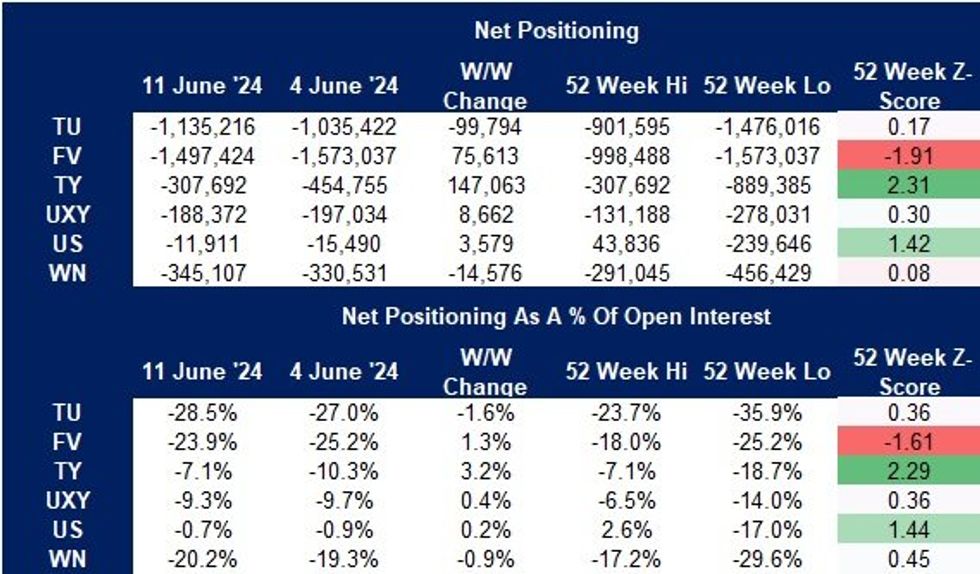

US TSY FUTURES: CFTC CoT Shows Asset Managers Adding To Duration & SOFR Longs Into FOMC & CPI

Last week’s CFTC CoT report (reference period cut off Tuesday 11 June) noted that non-commercial net positioning remains short across all Tsy futures contracts (this will be skewed by basis trade positions).

- In terms of the weekly movement, net shorts in the wings (TU & WN futures) were added to ahead of last week’s FOMC decision and CPI data, while net shorts were trimmed elsewhere (FV, TY, UXY & US futures).

- Asset managers added to their net long duration position across much of the curve, although trimmed net longs in both TY & UXY futures.

- Further forwards, that investor group flipped to net long positioning in SOFR futures for the first time since July ’23.

- Meanwhile, hedge funds extended their net shorts in SOFR futures (to the deepest level seen since April ’23) and trimmed net shorts in TY futures.

- A reminder that we suggested hedge fund short cover may have played into the move higher in SOFR futures during the second half of last week, as softer-than-expected inflation data and French political uncertainty provided dovish inputs for the market-implied Fed policy rate path.

Source: MNI - Market News/CFTC/Bloomberg

Source: MNI - Market News/CFTC/Bloomberg

CFTC: CAD Net Position Deteriorates in Wake of BoC Cut

- The largest net shifts in positioning last week see the NZD and GBP net longs improve, while, the EUR and MXN net longs trimmed and the AUD and CAD net shorts extend.

- Meanwhile, the CAD net position slips to a new series low, with the net short now amounting to 42.1% of open interest - a fresh 52w low. This presses the Z-score to the lowest among all currencies surveyed at -1.76. Positioning shift captures the response to the Bank of Canada's rate cut on June 5th, as well as the shift higher in USD/CAD spot from just below 1.3700, to just below 1.3800.

- The NZD net long, while still short of the 12m high in open interest terms, still represents a notable turnaround in fortunes. The outright net position now being north of 10k contracts is the largest since February 2021, while the pace of the switch from net short pushes the Z-score to the highest among all currencies surveyed - now at +1.81.

Full CFTC data here:

FOREX: EUR/JPY Firmer Off Support, But Downside Risks Pervade

- Consolidation has been the theme of the Monday session so far, with the USD Index holding the vast majority of the late gains posted last week, and keeping pressure on nearby resistance. For the USD Index, 105.805 is the level to watch and clearance here would mark the best levels since early May.

- EUR/JPY sits firmer ahead of the NY crossover, undoing a small part of the losses borne into the Friday close - we note that the cross pierced a key support at 167.92 Friday, a key trendline drawn from the Dec 7 ‘23 low, which broadly coincides with the 50-dma at 167.66. Price has found support at these levels to trade on a more stable footing today - but these will again be a focus on any near-term weakness.

- Political risk likely to be the near-term driver as markets watch opinion polls out of France - official campaigning begins this week - latest fieldwork (dated 15th June) from Ifop sees right-wing RN with 35%, left-wing alliance 26%, Macron's alliance at 19%.

- Focus for the duration of the Monday session turns to the Empire Manufacturing release for June and Canadian existing home sales. Central bank speakers are set to include ECB's de Guindos & Makhlouf, Fed's Williams & Harker.

EURJPY: Key Supports in Focus as French Campaigning Gets Underway

- EUR/JPY firmer early Monday, undoing a small part of the losses borne into the Friday close - we note that the cross pierced a key support at 167.92 Friday, a key trendline drawn from the Dec 7 ‘23 low, which broadly coincides with the 50-dma at 167.66.

- Price has found support at these levels to trade on a more stable footing today - but these will again be a focus on any near-term weakness.

- Political risk likely to be the near-term driver as markets watch opinion polls out of France - official campaigning begins this week - latest fieldwork (dated 15th June) from Ifop sees right-wing RN with 35%, left-wing alliance 26%, Macron's alliance at 19%.

- Front-end of the EURJPY vol curve well elevated as it captures French elections - 1 month contract now nearing 10 points for first time since early May.

OPTIONS: Expiries for Jun17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0670-85(E1.4bln), $1.0800-20(E2.1bln)

- USD/JPY: Y157.50($771mln), Y158.00($534mln)

- EUR/GBP: Gbp0.8445-50(E730mln)

- AUD/USD: $0.6600-15(A$1.5bln)

- USD/CAD: C$1.3765($630mln), C$1.3780($565mln)

WTI Futures Trading Near Resistance at 50-Day EMA

- WTI futures traded higher last week. For now, short-term gains are considered corrective and the trend direction remains bearish. However, resistance at $78.38, the 50-day EMA, has been pierced. A clear break of this average would expose the key short-term resistance at $80.62, the May 1 high, where a break is required to cancel a bear theme. On the downside, a resumption of weakness would open $71.33, the Feb 5 low.

- Gold is trading closer to its recent lows. A sharp sell-off on Jun 7 reinforces a short-term bearish theme. The yellow metal has traded below the 50-day EMA, at 2313.7. The break confirms a resumption of the reversal that started May 20 and signals scope for a deeper correction. This has opened $2277.4, the May 3 low. Clearance of this price point would strengthen a bearish theme. Initial firm resistance to watch is $2387.8, the Jun 7 high.

E-Mini S&P Remains Above 5400.00 Handle

- The trend condition in Eurostoxx 50 futures remains bullish, however, a corrective cycle has resulted in a pullback from the May high, and this bear cycle accelerated Friday. Last week’s move lower has resulted in a break of 4943.00, the Jun 11 low, highlighting potential for a deeper retracement. Scope is seen for a move towards 4762.00, the Apr 19 low and a key support. Firm resistance is at 5046.00, Jun 12 high.

- The uptrend in S&P E-Minis remains intact and the contract traded higher Wednesday last week. Price has recently cleared 5368.25, the May 23 high and bull trigger. The move confirmed a resumption of the uptrend. The continuation higher has resulted in a break of the 5400.00 handle. This opens 5462.77 next, a Fibonacci projection. Key short-term support has been defined at 5205.50, the May 31 low. Initial support lies at 5333.75, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 17/06/2024 | 1130/1330 | ECB's De Guindos remarks at APIE Seminar | ||

| 17/06/2024 | 1200/1400 | ECB's Cipollone chairing financial markets supervision session | ||

| 17/06/2024 | 1215/0815 | ** | CMHC Housing Starts | |

| 17/06/2024 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2024 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 17/06/2024 | 1300/0900 | * | CREA Existing Home Sales | |

| 17/06/2024 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/06/2024 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/06/2024 | 1700/1300 | Philadelphia Fed's Patrick Harker | ||

| 17/06/2024 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 17/06/2024 | 0100/2100 | Fed Governor Lisa Cook | ||

| 18/06/2024 | 0430/1430 | *** | RBA Rate Decision | |

| 18/06/2024 | 0900/1100 | *** | ZEW Current Conditions Index | |

| 18/06/2024 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 18/06/2024 | 0900/1100 | *** | HICP (f) | |

| 18/06/2024 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 18/06/2024 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 18/06/2024 | 1200/1400 | ECB's Cipollone chairing session on market supervision | ||

| 18/06/2024 | 1230/0830 | *** | Retail Sales | |

| 18/06/2024 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 18/06/2024 | 1315/0915 | *** | Industrial Production | |

| 18/06/2024 | 1330/1530 | ECB's De Guindos at EC and ECB joint conference | ||

| 18/06/2024 | 1400/1000 | * | Business Inventories | |

| 18/06/2024 | 1400/1000 | MNI Webcast with Richmond Fed's Tom Barkin | ||

| 18/06/2024 | 1540/1140 | Boston Fed's Susan Collins | ||

| 18/06/2024 | 1700/1300 | Fed Governor Adriana Kugler | ||

| 18/06/2024 | 1700/1300 | Dallas Fed's Lorie Logan | ||

| 18/06/2024 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/06/2024 | 1720/1320 | St. Louis Fed's Alberto Musalem | ||

| 18/06/2024 | 1800/1400 | Chicago Fed's Austan Goolsbee | ||

| 18/06/2024 | 2000/1600 | ** | TICS | |

| 19/06/2024 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 19/06/2024 | 2350/0850 | ** | Trade | |

| 19/06/2024 | 0600/0700 | *** | Consumer inflation report | |

| 19/06/2024 | 0600/0700 | *** | Producer Prices | |

| 19/06/2024 | 0600/0800 | ** | Unemployment | |

| 19/06/2024 | 0800/1000 | ** | Current Account | |

| 19/06/2024 | 0900/1100 | ** | Construction Production | |

| 19/06/2024 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 19/06/2024 | 1400/1000 | ** | NAHB Home Builder Index | |

| 19/06/2024 | 1730/1330 | BOC Minutes (Summary of Deliberations) | ||

| 20/06/2024 | 2245/1045 | *** | GDP |