Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- ECB not expected to rock the boat, but comms on policy ahead could be key

- Treasuries gear for advance GDP data and 7yr auction

- Oil prices remain firm, touching YTD highs in the process

US TSYS: Modestly Richer Ahead Of Important Session

- Cash Tsys trade 0.5-2.5bp richer, bull flattening but only modestly pare yesterday’s two-step sell-off with strength in flash US PMIs before a poorly received 5Y auction.

- TYH4 at 111-02 has held narrow ranges with solid but not particularly elevated volumes of 300k. The bear cycle remains in play, earlier overnight touching a low of 110-27+, close to support at 110-26 (Jan 19 low) before 110-16 (Dec 13 low).

- A heavy docket today, with the ECB decision before a data deluge including the US Q4 advance for real GDP/core PCE inflation (the latter providing a clue to tomorrow’s December core PCE print), jobless claims, durable goods and 7Y supply. Yellen also speaks

- Fed Funds cumulative cuts: 11bp for March (near recent lows), 31bp for May, 55bp for June and 133bp for Dec.

- Data: US GDP/Core PCE Q4 advance (0830ET), Weekly jobless claims (0830ET), Durable goods Dec prelim (0830ET), Goods trade balance Dec (0830ET), Retail/wholesale inventories Dec/Dec prelim (0830ET), New home sales Dec (1000ET), Kansas City Fed mfg index Jan (1100ET).

- Note/bond issuance: US Tsy $41B 7Y Note auction (91282CJX0) – 1300ET

- Bills issuance: US Tsy $90B 4W, $90B 8W bill auctions – 1130ET

- Tsy Sec Yellen speaks on the economic outlook, Chicago Economic Club (1235ET).

OI Suggests Rounds Of Short Setting & Long Cover Essentially Offset On Wednesday

The combination of yesterday's weakness in Tsy futures and preliminary OI data point to the following positioning swings across the curve on Wednesday:

- Net short setting: TU, TY and WN futures

- Net long cover: FV, UXY and US futures.

- Net curve OI was little changed on the day, with the above positioning swings essentially offsetting.

- A quick reminder that firmer-than expected S&P Global PMI data and a poorly-received round of 5-Year Tsy supply factored into yesterday's Tsy sell off.

| 24-Jan-24 | 23-Jan-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 3,953,177 | 3,940,883 | +12,294 | +462,547 |

| FV | 5,964,953 | 5,996,015 | -31,062 | -1,326,967 |

| TY | 4,663,660 | 4,638,039 | +25,621 | +1,634,336 |

| UXY | 2,125,894 | 2,130,261 | -4,367 | -396,350 |

| US | 1,429,467 | 1,440,685 | -11,218 | -1,495,504 |

| WN | 1,668,678 | 1,661,303 | +7,375 | +1,530,028 |

| Total | -1,357 | +408,090 |

OI Points To Mix Of Short Setting & Long Cover In SOFR Futures On Wednesday

The combination of yesterday's move lower across the SOFR strip and preliminary OI data point to the following positioning swings on Wednesday:

- Whites: Apparent net long cover in SFRH4 comfortably dominated form a net pack perspective, even with all other contracts in the pack seemingly subjected to net short setting.

- Reds: Only what seemed to be apparent net short setting in SFRZ4 broke the wider theme of net long cover in the pack, with the latter dominating in net pack terms.

- Greens: Only what seemed to be apparent (modest) net short setting in SFRU6 broke the wider theme of net long cover in the pack, with the latter dominating in net pack terms.

- Blues: A mix of apparent net short setting (SFRZ6 & M7) and long cover (SFRH7 & U7), with the former dominating in net pack terms.

| 24-Jan-24 | 23-Jan-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRZ3 | 1,204,888 | 1,200,276 | +4,612 | Whites | -45,897 |

| SFRH4 | 1,180,616 | 1,237,646 | -57,030 | Reds | -12,208 |

| SFRM4 | 1,113,606 | 1,109,423 | +4,183 | Greens | -11,051 |

| SFRU4 | 981,182 | 978,844 | +2,338 | Blues | +6,757 |

| SFRZ4 | 1,033,743 | 1,031,487 | +2,256 | ||

| SFRH5 | 539,919 | 547,830 | -7,911 | ||

| SFRM5 | 643,148 | 645,359 | -2,211 | ||

| SFRU5 | 572,443 | 576,785 | -4,342 | ||

| SFRZ5 | 628,089 | 632,317 | -4,228 | ||

| SFRH6 | 418,120 | 422,397 | -4,277 | ||

| SFRM6 | 417,109 | 420,338 | -3,229 | ||

| SFRU6 | 304,316 | 303,633 | +683 | ||

| SFRZ6 | 266,885 | 258,205 | +8,680 | ||

| SFRH7 | 134,443 | 136,279 | -1,836 | ||

| SFRM7 | 147,907 | 146,536 | +1,371 | ||

| SFRU7 | 148,799 | 150,257 | -1,458 |

BoC Review, Jan'24: A Partial Pivot With Inflation Still A Concern

We have published and e-mailed to subscribers the MNI BoC Review. Please find the full report including MNI analysis and views from 13 analysts here: https://roar-assets-auto.rbl.ms/files/59661/BOCReviewJan2024.pdf

CROSS ASSET: New ’24 Highs For Oil Not Necessarily Being Felt In Wider FI Markets

WTI & Brent crude oil futures have moved to fresh YtD highs today, with the well-documented uptick in already heightened geopolitical worry surrounding the Middle East being felt.

- The move comes despite the EIA recently telling MNI that it "expects oil production to be relatively unfazed by (these) tensions," although the Agency does still see prices "rising later this year before receding modestly in 2025."

- European gas futures were initially a little higher but have edged away from best levels to last trade -2.8%.

- On face value, the move higher in crude oil futures should be a headwind for bonds (all else equal), but a demand-side inflationary shock isn’t an indication of healthy economic activity, particularly as the global economy continues to adjust to the post-COVID interest rate environment.

- EUR & USD 5y5y inflation-linked swaps are essentially unchanged on the day (with a very mild bias lower), while EUR 2-Year ZCS show a similar picture.

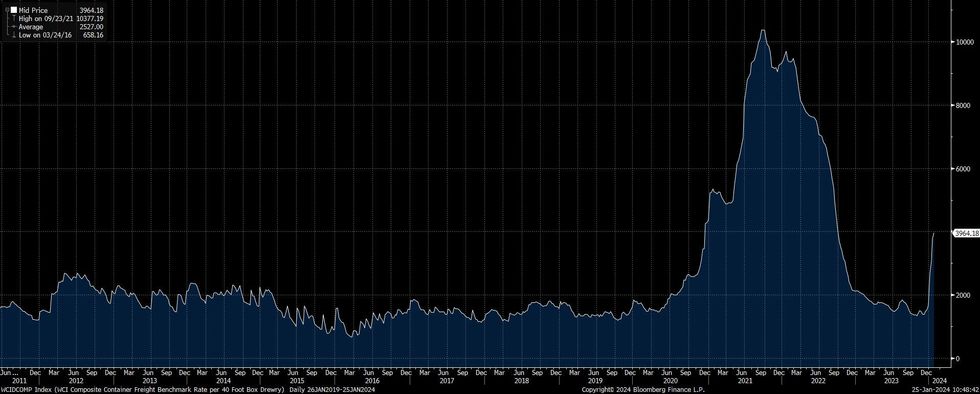

- The Middle East tension-driven move higher in benchmark freight rates remains much shallower than that seen during the COVID-19 pandemic and comes after a moderation back to pre-pandemic norms (as outlined in the below image).

- On this front, HSBC have noted that “even if disruption persists for longer than initially anticipated, is that the world is in a much better position than during the COVID-19 pandemic re: weathering shipping snarls and the same issues with landside logistics (e.g. labour movement restrictions at ports) are not present this time around.”

- When it comes to feedthrough for central banks HSBC notes that "higher shipping costs tend to quickly filter through to producer prices, but the impact on consumer prices can take time to bear out: peaking after around 12 months, according to the IMF.”

- This would suggest that feedthrough into the pricing of the path of policy rates across the major global central banks has been limited thus far (pricing for end of '24 policy rate levels has already pared back aggressively from late '24 dovish extremes).

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

FX OPTIONS: While EUR Vols Have Crept Higher, ECB Impact Seen More Muted Relative to US CPI, NFP

- Despite broad consensus for no change at today’s ECB decision, EUR overnight vols have crept higher, with EUR/GBP implied nearing the best levels of 2024 having printed just over 8 points. This equates to markets pricing a ~25 pip swing in the cross over the course of the decision – a move which would bring yesterday’s lows of 0.8536 into contention in the event of EUR weakness. A weaker EUR into the Thursday NY cut would put the E300mln expiry at 0.8500 into play.

- In relative terms, the vol premium being priced into EUR/USD, however, is shy of levels seen ahead of both the Nonfarm payrolls and US CPI releases this January – suggesting markets anticipate more muted market fallout to Lagarde’s press conference today.

- The pricing out of ECB rate cuts in Q1 (an April 25bps cut is now roughly 50/50 having been fully priced as recently as early last week) has worked in favour of EUR option dynamics, with the 3m EUR/GBP risk reversal improving off mid-Jan lows and potentially concluding the downtrend off the Jun’23 high.

RRR Cut Facilitates Bid, H-Share Discount To Mainland Equivalents Narrows From 15-Year Wides

MNI (London) - The earlier- and larger-than-expected RRR cut from the PBoC boosted Chinese equity sentiment on Thursday, although questions continued to do the rounds re: the efficacy of the latest liquidity injection given worry surrounding the demand side of the economic equation. That kept discussions surrounding the next stage of stimulatory measures front and centre.

- The CSI 300 finished 2.0% better off, with the Hang Seng adding a similar amount. The latter has retaken the 16,000 mark, recovering from Monday’s showing below 15,000.

- The Hang Seng has seen a more notable rally in the wake of this week’s delivered policy easing and speculation surrounding policymaker and regulator support for the equity market. This has allowed the discount of H-shares vs. respective A-shares to move away from ~15-Year extremes.

- Credit access for property developers remains a focal point for regulators and policymakers, with broader support on that front helping to facilitate a bid for related equity names on Thursday.

- Looking a little deeper, SOEs benefitted from a particular focus on injecting higher quality assets into the space.

- Earnings-/guidance-related positives were seen in several names.

- Coal names benefited from policymaker focus on the quickening of the development of Shanxi-based coal projects.

- The HK-China Stock Connect links generated ~CNY6.3bn of net mainland inflows via the northbound channels, representing the largest round of daily net purchases via those links since the turn of the year.

EUROPE ISSUANCE UPDATE:

Italy Auction Results:- E2.5bln of the 3.60% Sep-25 BTP Short Term. Avg yield 3.21% (bid-to-cover 1.45x)

- E1bln of the 1.50% May-29 BTPei. Avg yield 1.61% (bid-to-cover 1.58x)

- E1.5bln of the 2.40% May-39 BTPei. Avg yield 2.32% (bid-to-cover 1.47x)

FOREX: Markets Anticipate Muted Response to Thursday ECB

- Currency markets are largely holding their late Wednesday session moves, with USD/JPY comfortably off yesterday's lows and holding above Y147.50. EUR/USD and GBP/USD are similarly creeping off lows, but the mid-week highs remain out of reach for now.

- The Norges Bank made no change to either rates or guidance at this morning's decision, with the bank pledging to keep rates at current levels for an extended period. The policy statement acknowledged that the currency is stronger than expected, however there was little change to the economy since December's projections. NOK firm modestly once the rate decision had concluded, with firmer oil prices likely having a bigger impact than policy this morning. EUR/NOK has printed lower lows for a fourth session, with the trend outlook remaining bearish for now.

- The ECB rate decision takes focus going forward. Despite broad consensus for no change at today’s ECB decision, EUR overnight vols have crept higher, with EUR/GBP implied nearing the best levels of 2024 having printed just over 8 points. This equates to markets pricing a ~25 pip swing in the cross over the course of the decision – a move which would bring yesterday’s lows of 0.8536 into contention in the event of EUR weakness. A weaker EUR into the Thursday NY cut would put the E300mln expiry at 0.8500 into play.

- US data picks up into the Thursday session, with advanced Q4 GDP on the docket as well as weekly jobless claims and the prelim December durable goods orders read. Fedspeak is expected to remain muted, with the FOMC inside their pre-decision media blackout period.

FX OPTIONS: Expiries for Jan25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0825(E871mln), $1.0850(E767mln), $1.0885-00(E765mln), $1.0945-50(E1.0bln), $1.0975-80(E1.2bln), $1.1000-10(E1.4bln)

- USD/JPY: Y146.50-60($570mln), Y147.55-65($617mln)

- EUR/JPY: Y161.30(E770mln)

- GBP/USD: $1.2815(Gbp554mln)

- USD/CNY: Cny7.1900($1.5bln)

GILTS: Bulk of Early Weakness Holds, Key Technical Levels Untouched

Gilts have recovered from session lows, with the Dec 11 extremes in both futures and 10-Year yields remaining untested.

- Futures last print -37 at 97.75, 18 ticks off the base of the early 54-tick range.

- Cash yields are 2.0-3.5bp higher on the day, with a light steepening bias seen on the curve.

- When it comes to the recent cross-market widening of gilts vs. peers (spreads are off widest levels of the day across the curve) we point to the combination of heightened expectations surrounding pre-election UK fiscal stimulus and data releases, in addition to the related feedthrough from both into BoE-dated OIS pricing, as the meaningful drivers.

- Note that BoE-dated OIS now shows ~91bp of cuts through ’24, a little over 60bp off the late December dovish extremes.

- The moderation in the BoE cuts priced through the end of ’24 has comfortably outstripped the comparative move in ECB pricing since the start of last week (by ~22bp).

- SONIA futures are +0.5 to -5.0 through the blues. The reds are under the most pressure.

- Looking ahead, only lower tier local data is due today, which will likely leave focus on wider market matters and headline flow (the latest ECB decision and U.S. data provide the scheduled risk events of note).

| BoE Meeting | SONIA BoE-Dated OIS (%) | Difference Vs. Current Effective SONIA Rate (bp) |

| Feb-24 | 5.200 | +1.3 |

| Mar-24 | 5.183 | -0.5 |

| May-24 | 5.092 | -9.6 |

| Jun-24 | 4.969 | -21.8 |

| Aug-24 | 4.783 | -40.4 |

| Sep-24 | 4.618 | -56.9 |

| Nov-24 | 4.417 | -77.0 |

| Dec-24 | 4.277 | -91.0 |

EQUITIES: Sustained Move Higher in E-Mini S&P Reinforces Uptrend

- Eurostoxx 50 futures have recovered from last week’s low of 4402.00 on Jan 17 and the contract traded sharply higher Wednesday. 4402.00 represents a key short-term support. A break of it would resume recent bearish pressure and open 4370.00, the Nov 28 low. On the upside, key resistance is at 4634.00, the Dec 14 high. Clearance of this level would confirm a resumption of the medium-term uptrend. Initial support lies at 4498.90, the 20-day EMA.

- The uptrend in S&P E-Minis remains intact and this week’s move higher reinforces current conditions. Resistance at 4841.50, the Dec 28 high has recently been cleared, confirming an extension of the price sequence of higher highs and higher lows. Moving average studies remain in a bull-mode condition, highlighting positive market sentiment. Sights are on 4952.45 next, a Fibonacci projection. Key support lies at 4721.08, the 50-day EMA.

COMMODITIES: Break of 50-Day EMA Strengthens Bearish Threat in Gold

- Trend signals in WTI futures remain bearish and the latest recovery still appears to be a correction - for now. The contract has traded through the 50-day EMA at $74.28. This opens $76.31, the Dec 26 high and a near-term bull trigger. A break of this hurdle would undermine the bearish theme. Moving average studies continue to highlight a downtrend. The trigger for a resumption of the downtrend is $68.28, Dec 13 low.

- Gold remains above the Jan 17 low of $2001.9 - for now. The recent print below the 50-day EMA and the break of support at $2013.4, the Jan 11 low, has strengthened a bearish threat and a resumption of weakness would open a key level at $1973.2, the Dec 13 low. For bulls, clearance of 2062.3, the Jan 12 high, is required to signal a reversal. This would expose $2088.5, the Dec 28 high.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 25/01/2024 | 1100/0600 | *** |  | TR | Turkey Benchmark Rate |

| 25/01/2024 | 1100/1100 | ** |  | UK | CBI Distributive Trades |

| 25/01/2024 | 1315/1415 | *** |  | EU | ECB Deposit Rate |

| 25/01/2024 | 1315/1415 | *** | | EU | ECB Main Refi Rate |

| 25/01/2024 | 1315/1415 | *** | | EU | ECB Marginal Lending Rate |

| 25/01/2024 | 1330/0830 | *** |  | US | Jobless Claims |

| 25/01/2024 | 1330/0830 | ** | | US | WASDE Weekly Import/Export |

| 25/01/2024 | 1330/0830 | *** | | US | GDP |

| 25/01/2024 | 1330/0830 | ** | | US | Durable Goods New Orders |

| 25/01/2024 | 1330/0830 | ** | | US | Advance Trade, Advance Business Inventories |

| 25/01/2024 | 1345/1445 | | EU | ECB Monetary Policy Press Conference | |

| 25/01/2024 | 1400/1500 | ** |  | BE | BNB Business Sentiment |

| 25/01/2024 | 1500/1000 | * |  | CA | Payroll employment |

| 25/01/2024 | 1500/1000 | *** | | US | New Home Sales |

| 25/01/2024 | 1515/1615 | | EU | ECB's Lagarde ECB Podcast - latest monetary policy decisions | |

| 25/01/2024 | 1530/1030 | ** | | US | Natural Gas Stocks |

| 25/01/2024 | 1600/1100 | ** | | US | Kansas City Fed Manufacturing Index |

| 25/01/2024 | 1630/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 25/01/2024 | 1630/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 25/01/2024 | 1800/1300 | ** | | US | US Treasury Auction Result for 7 Year Note |

| 26/01/2024 | 2330/0830 | ** |  | JP | Tokyo CPI |

| 26/01/2024 | 0001/0001 | ** | | UK | Gfk Monthly Consumer Confidence |

| 26/01/2024 | 0700/0800 | * |  | DE | GFK Consumer Climate |

| 26/01/2024 | 0700/0800 | ** |  | SE | Unemployment |

| 26/01/2024 | 0745/0845 | ** |  | FR | Consumer Sentiment |

| 26/01/2024 | 0900/1000 | ** | | EU | M3 |

| 26/01/2024 | 1330/0830 | ** | | US | Personal Income and Consumption |

| 26/01/2024 | 1500/1000 | ** | | US | NAR Pending Home Sales |

| 26/01/2024 | 1600/1100 | | CA | Finance Dept monthly Fiscal Monitor (expected) | |

| 26/01/2024 | 1800/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.