Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- EUR/USD uptrend persists, 2021 highs in view

- Stocks narrow gap with alltime highs, Treasury curve flattens

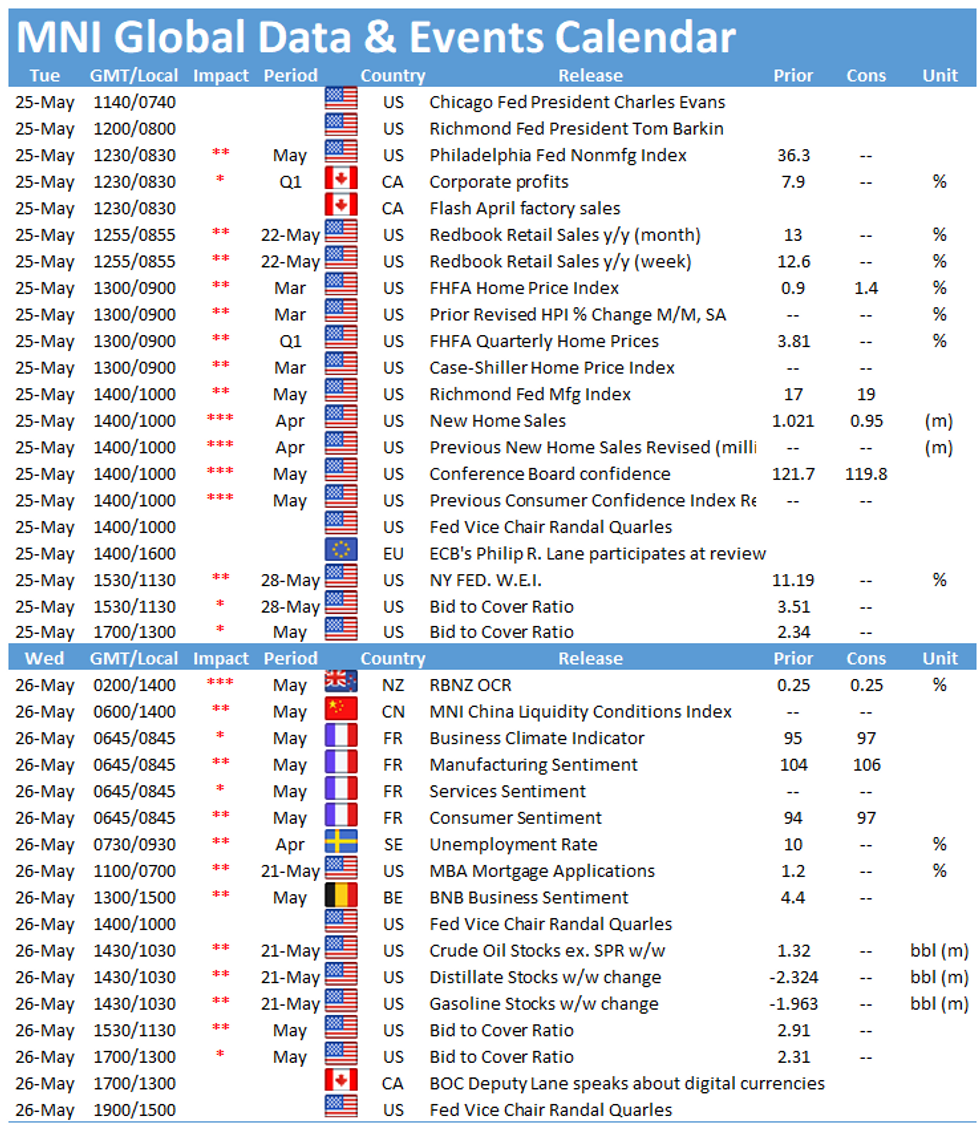

- Fedspeak in focus, Barkin, Evans and Quarles due

US TSYS SUMMARY: 2-Yr Supply And More Fed Speakers

Treasuries have held onto overnight gains which were made largely within the space of 1 hour (0200-0300ET) overnight in early European trade. A decent mix of supply, Fed speakers and data ahead.

- The 2-Yr yield is unchanged at 0.1493%, 5-Yr is down 0.7bps at 0.7969%, 10-Yr is down 1bps at 1.591%, and 30-Yr is down 1.4bps at 2.2853%. Jun 10-Yr futures (TY) up 3/32 at 132-23 (L: 132-19 / H: 132-24.5), volumes elevated (563K) but largely roll related (also 380K TYU1).

- Overnight, KC Fed's George noted she can't dismiss current pricing signals despite likelihood that inflation is likely transitory; suggests flexible Fed approach (comments had little impact on the space though).

- Fed speakers today: Richmond's Barkin (0800ET); Chicago's Evans (0940ET), VC Quarles (1000ET).

- Housing data includes house price purchase index (0900ET) and new home sales (1000ET), while we also get Conference Board confidence and Richmond Fed at 1000ET.

- Republicans set to meet today to mull a new offer to the White House on infra. Overall tone is that it looks like we're not close to getting a deal. Also in D.C., worth noting Senate Finance Committee confirmation hearings for Tsy officials at 0930ET, incl Nellie Liang as undersecretary.

- $40B 42-day bills auction at 1130ET, while $60B in 2-Yr Notes sell at 1300ET. NY Fed buys ~1.425B of 10-22.5Y Tsys.

EGB/GILT SUMMARY - Periphery Outperforming

European government bonds have broadly rallied this morning with the EGB periphery outperforming alongside gains for equities.

- Gilts opened firmer and have traded sideways through the morning. Yields are 1bp lower on the day.

- Bunds have similarly firmed with the curve 1bp flatter.

- OATs have marginally outperformed bunds with belly/long-end yields 2-3bp lower on the day.

- BTPs have outperformed core EGBs with cash yields down 3-5bp.

- Supply this morning came from Germany (Bubill, EUR3.614bn allotted) and the Netherlands (DSL, EUR1.7bn). France will offer EUR5.3-6.5bn of BTFs this afternoon. The UK is today issuing GBP4bn of a 0.125% Mar-39 linker via syndication with books last seen over GBP28.75bn. There is also a hefty EUR20.3bn OAT redemption today.

- The final German Q1 GDP print was a touch weaker than the initial estimate (-1.8% Q/Q vs -1.7% previously).

EUROPE ISSUANCE UPDATE: UK, EU Syndications

UK to sell GBP4.0bln of new 0.125% Mar-39 Gilt linker, fixed spread -0.5 vs 2040.

- Books above GBP 28.75bln

- This is larger than the GBP2.75-3.0bln nominal MNI had pencilled in going into today's syndication.

EU tapping E460mln of 0.25% Apr-36 bond, guidance MS +4 area.

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXN1 170.50/171.50/172.50c fly, sold at 19 in 1.5k (profit taking)

3RM1 100.37/50cs bought for 0.25 in 4k

UK:

3LM1 99.12/25/37c fly, bought for 5 in 3k

L U1 99.87/100.00/100.12c fly 1x3x2, sold at 4 in 7.1k

FOREX: Greenback Weaker as Equities Progress, Yields Slip

- The EUR/USD uptrend persists early Tuesday, with the pair showing above the recent 1.2245 high and hitting multi-month highs in the process. This narrows the gap with 2021's best levels at 1.2349.

- The greenback is weaker across the board, slipping alongside Treasury yields ahead of the NY open, with the curve modestly flatter through the European morning.

- Similarly, with the JPY is softer, underperforming alongside the USD, as markets watch the persistent equity strength boosting US futures further. EUR/JPY is nearing the cycle highs posted May 19th at 133.44.

- Vols are steady, with the front-end of the curve across DMFX holding much of the early May strength.

- Central bank speak remains the focus, with another busy slate Tuesday. Fed's Barkin, Evans and Quarles are due to speak as well as the ECB chief economist Lane and BoE's Tenreyro.

- US new home sales and consumer confidence numbers are the data highlight.

FX OPTIONS: Expiries for May25 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2095-1.2105(E1.3bln-E1.2bln of EUR puts), $1.2150-60(E518mln), $1.2215-25(E629mln-EUR puts), $1.2260-75(E1.2bln-EUR puts), $1.2325-45(E679mln-EUR puts)

- USD/JPY: Y107.50-60($1.1bln), Y107.85-108.05($1.5bln), Y108.85-109.00($657mln)

- USD/NOK: Nok8.40($410mln-USD puts)

Price Signal Summary - EUR Uptrend Persists And Equities Stay Firm

- In the equity space, S&P E-minis continue to trade constructively and have cleared resistance at $4185.00, May 21 high. This opens 4238.25, May 10 high. Key trend support lies at 4029.25, May 13 low. EUROSTOXX 50 futures have traded higher too, breaching 4036.00, May 10 high. The move higher confirms a resumption of the uptrend and opens 4099.00,1.00 projection of the Mar - Jul - Oct 2020 price swing.

- In the FX space, EURUSD strength persists to keep the uptrend in tact. The pair has cleared 1.2245 with sights set on 1.2285 next, Jan 8 high. GBPUSD is trading closer to recent highs and remains bullish. The focus is on 1.4237, Feb 24 high and this year's high print. USDJPY support is unchanged at 108.34, May 7 low. A bullish theme dominates while this support holds and attention is on 109.79, May 13 high. A break of 108.34 however would highlight a trendline break drawn off the Jan 6 low and risk a deeper pullback.

- On the commodity front, Gold is consolidating but remains bullish. The focus is on $1892.7, 76.4% retracement of the Jan 6 - Mar 8 sell-off. Oil contracts have recovered from recent lows. Brent (N1) key resistance is at $70.24, May 18 high and the bull trigger. WTI (N1) bulls are eyeing$67.02, May 18 high.

- In the FI space, Bunds (M1) is firmer as the short-term correction extends. The next resistance is 169.62, the 20-day EMA. The bear trigger is 168.29, May 19 low. Directional risk in Gilts (M1) is still skewed to the downside despite recent strength. The key support and bear trigger is 126.79, Mar 18 low. Key resistance is 128.80 High May 7.

EQUITIES: Indices Make Further Progress, Germany Leads

- Global equity markets are in the green early Tuesday, with US futures indicating a positive open on Wall Street later today. The index has now narrowed the gap with the early May alltime highs to around 30 points.

- On the continent, European markets are generally higher with German names leading. The DAX trades higher by over 0.8% thanks to strength in Deutsche Wohnen and Delivery Hero shares. UK's FTSE-100 lags slightly, as commodity and oil stocks drag on the headline index.

COMMODITIES: Brent, WTI Roll Off Highs, Silver Consolidates

- After the sharp Friday/Monday rally, both WTI and Brent crude futures are in negative territory ahead of the Tuesday open, as prices roll off recent highs. The key macro drivers remain the same, with focus turning to the resumption of the Iranian nuclear deal talks due to kick off again in Vienna later today.

- Directional parameters for WTI remain unchanged at $67.02 to the upside, and the $61.56 first support.

- Gold and silver are mixed, with gold slightly higher while silver consolidates. Today's USD weakness has failed to support prices, with silver now circling the first support at the Friday low of 27.202.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok