Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

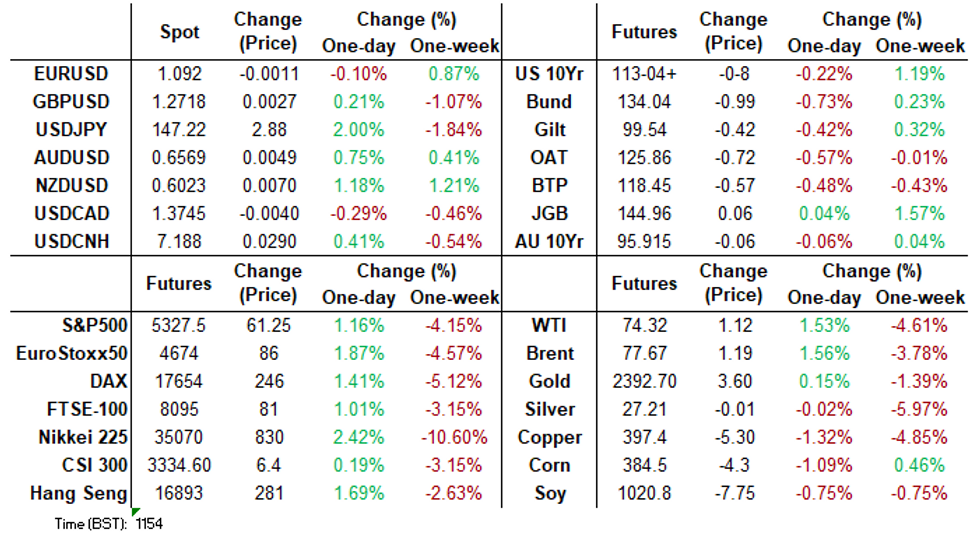

- European equities extend bounce from Monday's lows, JPY pressured.

- Bonds lower as a result.

- Limited calendar leaves focus on broader sentiment.

US TSYS: New Post-Payrolls Lows, 10Y Auction To Headline Thin Docket

Treasuries have recently set fresh post-payrolls lows in a continued pushback on prior recessionary fears seen in the aftermath of a dovish report but one that had some notable caveats.

- Cash yields are 3.7-5.1bp higher on the day, led by 2s.

- 2Y yields have met some resistance between 4.02-4.03% (a latest high of 4.030%) as they remain below the ~4.12% seen pre-payrolls.

- 10Y yields of 3.93% meanwhile are back at pre-payrolls levels courtesy of real yields now sitting ~6bp higher.

- TYU4 has seen a session low of 113-01+ having also essentially closed the post-payrolls gap via 115-03+. It’s the latest step closer to support 112-21 (Aug 2 low). Volumes of 460k are still elevated but less so than overnight sessions for the prior two days.

- Headlines and sentiment should drive today’s session until the 10Y auction. It comes after yesterday’s relatively well-received 3Y and is followed by the 30Y tomorrow.

- Data: Weekly MBA mortgage data (1200ET)

- Fedspeak: Collins to Rhode Island (1200ET – no remarks expected)

- Note/bond issuance: US Tsy $42B 10Y Note auction - 91282CLF6 (1300ET)

- Bill issuance: US Tsy $60B 17W bill auction (1130ET)

US TSY FUTURES: OI Points To Net Long Cover In Most Contracts On Tuesday

The combination of yesterday’s sell off in Tsy futures and OI data points to net long cover in most contracts, as part of the broader (partial) unwind of the recent risk-off price action.

- The only exception to the rule came via modest net short setting in TU futures.

| 06-Aug-24 | 05-Aug-24 | Daily OI Change | OI DV01 Equivalent Change ($) | |

| TU | 4,407,072 | 4,385,454 | +21,618 | +804,314 |

| FV | 6,587,063 | 6,644,734 | -57,671 | -2,451,154 |

| TY | 4,854,475 | 4,870,017 | -15,542 | -1,024,460 |

| UXY | 2,121,660 | 2,140,469 | -18,809 | -1,729,484 |

| US | 1,750,794 | 1,753,480 | -2,686 | -367,700 |

| WN | 1,671,501 | 1,678,247 | -6,746 | -1,444,179 |

| Total | -79,836 | -6,212,663 |

STIR: Modest Further Trimming Of Fed Cuts

- Fed Funds futures have further trimmed rate cut expectations overnight amidst a lack of new headlines that can support those looking for US recessionary signs.

- They have also mostly faded dovish BoJ commentary overnight re Dep Gov Uchida not wanting to hike amidst volatile markets.

- Cumulative cuts from 5.33% effective: 44bp Sep, 75bp Nov, 106bp Dec and 126bp Jan.

- As such the path very roughly considers a first 50bp cut before three 25bp cuts as we await a next trigger.

- Today sees broader sentiment likely in the driving seat, with a light data docket and no Fedspeak scheduled (Boston Fed’s Collins ’25 voter is listed but not expected to give remarks).

- It leaves tomorrow’s weekly jobless claims as the remaining macro focal point of the week with attention on PPI/CPI on Tue/Wed next week.

STIR: OI Points To Mix Of Short Setting & Long Cover In SOFR Futures On Tuesday

Yesterday’s sell off in SOFR futures and OI data points to a mix of net short setting and long cover as some of the recent risk-off price action was unwound.

- Fed Funds futures now price ~105bp of cuts through the Dec FOMC vs. nearly 150bp at one point on Monday, with odds of intra-meeting Fed action fading.

| 06-Aug-24 | 05-Aug-24 | Daily OI Change | Daily OI Change In Packs | ||

| SFRM4 | 1,126,664 | 1,119,767 | +6,897 | Whites | -20,363 |

| SFRU4 | 1,098,218 | 1,113,766 | -15,548 | Reds | -2,002 |

| SFRZ4 | 1,161,913 | 1,139,551 | +22,362 | Greens | +27,721 |

| SFRH5 | 914,765 | 948,839 | -34,074 | Blues | -12,508 |

| SFRM5 | 799,895 | 806,589 | -6,694 | ||

| SFRU5 | 651,621 | 644,394 | +7,227 | ||

| SFRZ5 | 883,195 | 896,086 | -12,891 | ||

| SFRH6 | 610,973 | 600,617 | +10,356 | ||

| SFRM6 | 553,124 | 543,079 | +10,045 | ||

| SFRU6 | 523,484 | 508,180 | +15,304 | ||

| SFRZ6 | 432,597 | 425,474 | +7,123 | ||

| SFRH7 | 241,379 | 246,130 | -4,751 | ||

| SFRM7 | 253,419 | 259,068 | -5,649 | ||

| SFRU7 | 209,042 | 202,743 | +6,299 | ||

| SFRZ7 | 233,913 | 244,729 | -10,816 | ||

| SFRH8 | 146,949 | 149,291 | -2,342 |

EUROPEAN ISSUANCE UPDATE

15-Year Bund Auction Results

- E500mln (E407mln allotted) of the 1.00% May-38 Bund. Avg yield 2.44% (bid-to-offer 4.13x; bid-to-cover 5.07x).

- E1.5bln (E1.199bln allotted) of the 2.60% May-41 Bund. Avg yield 2.51% (bid-to-offer 1.29x; bid-to-cover 1.61x).

4.125% Jul-29 Gilt Auction Results

The GBP4bn 4.125% Jul-29 gilt auction was quite weak, with a 2.87x bid-to-cover ratio, a 0.9bp tail and a lowest accepted price of 101.167 falling short of the pre-auction mid at 101.195.

- The previous re-opening on July 17 also registered a 0.9bp tail, but saw a stronger bid-to-cover ratio of 3.1x.

- Prior to today’s re-opening, the Jul-29 Gilt had averaged a bid-to-cover of 3.28x, and a yield tail of 0.65bp.

- More broadly, today’s 2.87x bid-to-cover was the lowest among Gilts within the 3-7-year maturity bucket since January this year (2.86x for the 4.50% Jun-28). The December 2023 auction of the 4.50% Jun-28 Gilt also saw a 2.53x cover.

- The reaction in Gilt futures has been fairly contained though, just a few ticks below pre-auction levels.

- GBP4bln of the 4.125% Jul-29 Gilt. Avg yield 3.854% (bid-to-cover 2.87x, tail 0.9bp).

FOREX: Yen Consolidates Weakness Post Dovish BOJ Rhetoric, NZD Outperforms

Dovish remarks from BOJ Deputy Governor Uchida overnight stoked a strong reversal lower for the Japanese Yen, and despite a moderate pullback, USDJPY trades close to the 147 handle, consolidating near 2% gains on the session.

- As a reminder, BOJ’s Uchida stated that rates won't be raised if the market is unstable, and the rate path will shift if market moves affect the economic outlook. This offset earlier comments that rates would continue to rise if projections unfolded as expected.

- The latest USDJPY recovery - a correction - is allowing an oversold condition to unwind and initial resistance is seen at 149.77, the Aug 2 high.

- NZDJPY stands out as the key outperforming cross, rising over 3% on the day. This follows the earlier Q2 employment data beat, which prompted RBNZ easing expectations for next week's meeting considerably diminish.

- NZD/USD remains up 1% and is back above 0.6000, while AUDNZD (-0.45%) continues to grind lower, hovering around the 1.0900 mark.

- Higher core yields and the associated pressure on the yen has also filtered through to the Swiss Franc, with both EURCHF and USDCHF rising by 1.25%.

- Other major pairs such as EURUSD and GBPUSD remain in very tight ranges as the action remains on the low yielders that have been most sensitive to carry unwinds in recent sessions.

- Canada Ivey PMI and BOC minutes highlight a relatively quiet economic calendar on Wednesday. Despite remarks not being expected, it is worth noting that Boston Fed President Susan Colllins will travel to Rhode Island to meet with a wide range of participants in the economy.

FX OPTIONS: Expiries for Aug07 NY cut 1000ET (Source DTCC)

- EURUSD: 1.0900 (347mln), 1.0945 (329mln), 1.0950 (347mln)

- USDJPY: 146.00 (500mln), 147.35 (1.32bn)

- EURGBP: 0.8620 (669mln)

- USDCAD: 1.3735 (220mln), 1.3750 (360mln)

- AUDUSD: 0.6530 (349mln), 0.6550 (200mln)

- AUDNZD: 1.0950 (488mln)

MNI Banxico Preview - Aug 2024: Cautious Board Leaning Towards Rate Cut

Executive Summary

- Analysts appear evenly divided over the outcome of this week’s Banxico decision.

- Prior forward guidance suggested greater willingness to consider a rate cut in August, and the recent softening of US data and dovish repricing for the Fed should bolster the case to restart policy easing in Mexico.

- However, a strong rebound in headline inflation and recent pressure on MXN amidst the sell-off in risk assets promotes the need for caution and enhances the likelihood of a split vote and the possibility of a rate hold at this juncture.

- Click to view the full preview:MNI Banxico Preview - Aug 2024.pdf

EQUITIES: EUROSTOXX 50 Bear Threat Remains Present Despite Bounce

S&P E-Minis traded lower late last week and the contract started this week on a bearish note - Monday’s move lower marks an extension of the bear cycle. The move down has resulted in a print below 5185.50, 76.4% of the Apr 19 - Jul 16 bear leg. A clear break of this level would open 5092.00 next, the May 2 low. Monday’s intraday high of 5345.50 marks initial resistance. Gains are considered corrective - for now.

- A bear threat in EUROSTOXX 50 futures remains present and the contract traded lower Monday having started the week on a bearish note. Last week’s sell-off resulted in a break of 4846.00, the Apr 19 low. The breach highlights a stronger reversal and signals scope for an extension towards 4478.81 next, the 2.236 projection of the Jun 6 - 14 - Jul 12 price swing. First resistance is 4720.53, 38.2% of the Jul 12 - Aug 5 bear leg.

OIL: Oil Futures Remain Vulnerable

Recent weakness in Gold appears to be a correction - for now. However, note that the yellow metal has managed to pierce support at the 50-day EMA - at $2375.3. A clear break of this average would signal scope for a deeper retracement towards $2277.4, the May 3 low and a key support. For bulls, a resumption of gains would open $2483.7, the Jul 17 high and a bull trigger. Clearance of this hurdle would resume the uptrend.

- In the oil space, a bear threat in WTI futures remains present and the contract traded lower Monday, extending the current downtrend. Sights are on the next key support at $72.23, the Jun 4 low. It has been pierced, a clear break would reinforce bearish conditions and pave the way for an extension towards $70.73, the Feb 5 low. Key resistance is seen at $78.88, the Aug 1 high. Short-term gains would allow an oversold condition to unwind.

| Date | GMT/Local | Impact | Country | Event |

| 07/08/2024 | 1400/1000 | * |  CA CA | Ivey PMI |

| 07/08/2024 | 1430/1030 | ** |  US US | DOE Weekly Crude Oil Stocks |

| 07/08/2024 | 1700/1300 | ** | US | US Note 10 Year Treasury Auction Result |

| 07/08/2024 | 1730/1330 | CA | BOC Minutes (Summary of Deliberations) | |

| 07/08/2024 | 1900/1500 | * | US | Consumer Credit |

| 08/08/2024 | 2301/0001 | ** |  GB GB | KPMG/REC Jobs Report |

| 08/08/2024 | 0500/1400 |  JP JP | Economy Watchers Survey | |

| 08/08/2024 | 1230/0830 | *** | US | Jobless Claims |

| 08/08/2024 | 1230/0830 | ** | US | WASDE Weekly Import/Export |

| 08/08/2024 | 1400/1000 | ** | US | Wholesale Trade |

| 08/08/2024 | 1430/1030 | ** | US | Natural Gas Stocks |

| 08/08/2024 | 1530/1130 | * | US | US Bill 08 Week Treasury Auction Result |

| 08/08/2024 | 1530/1130 | ** | US | US Bill 04 Week Treasury Auction Result |

| 08/08/2024 | 1700/1300 | *** | US | US Treasury Auction Result for 30 Year Bond |

| 08/08/2024 | 1900/1500 | *** |  MX MX | Mexico Interest Rate |

| 08/08/2024 | 1900/1500 | US | Richmond Fed's Tom Barkin |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.