Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Stocks start week on a positive note, but still well shy of Friday highs

- NOK, CAD outperform as oil extends bounce off Friday low

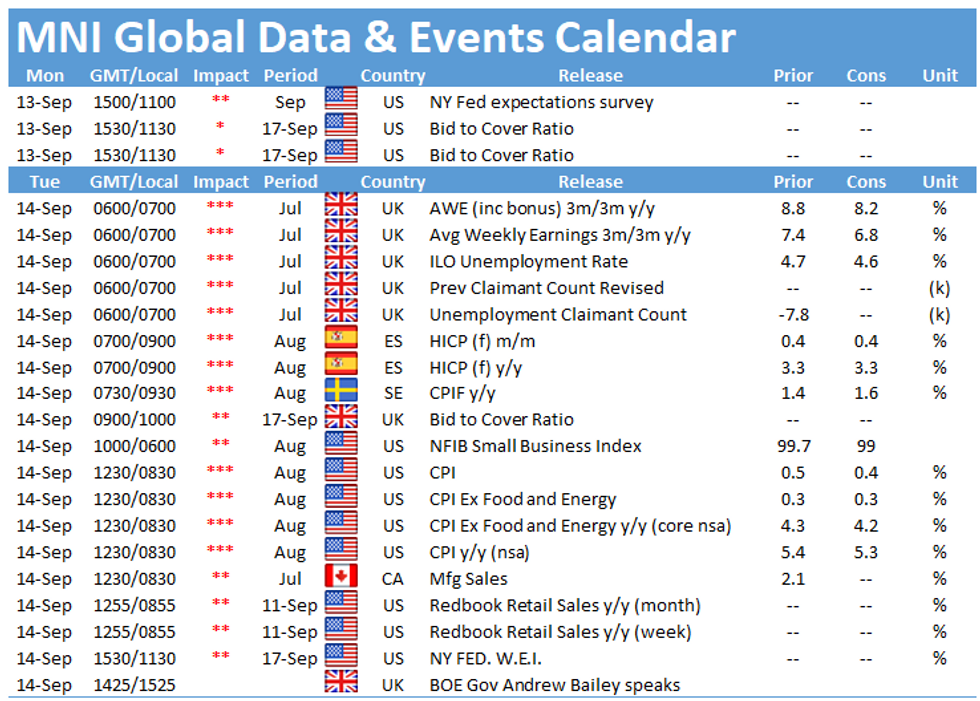

- Data, speaker slate light Monday, with just an appearance from ECB's Lagarde on the docket

US TSYS: Curve A Little Flatter In Run-Up To CPI

Treasuries are trading fairly flat Monday - within Friday's ranges for the most part, and on limited volumes. Attention is already on Tuesday's CPI release, with Monday's schedule looking very light.

- Curve a little flatter, with 30s outperforming: 2-Yr yield is up 0.6bps at 0.2189%, 5-Yr is up 0.2bps at 0.8176%, 10-Yr is down 0.9bps at 1.3326%, and 30-Yr is down 1.4bps at 1.9194%.

- Dec 10-Yr futures (TY) up 0.5/32 at 133-5.5 (L: 133-02.5 / H: 133-08)

- The only data is the monthly budget statement at 1400ET, and there are no Fed speakers as we have entered the pre-FOMC blackout period.

- In an interview published Sunday, Philly Fed's Harker said he saw tapering "sooner rather than later" but still saw a rate hike in late 2022/early 2023. No discernable market reaction, as Harker already seen leaning hawkish, and not a 2021-22 FOMC voter.

- In the absence of obvious macro drivers, there could be some attention on Capitol Hill, with headlines over the weekend focused on Democratic tax hikes and intra-party disagreements over the size and scope of the $3.5T reconciliation package.

- Supply is limited to bills: $93B combined of 13-/26-week bill sale at 1130ET.

- NY Fed makes its last operational purchase purchase (22.5-30Y Tsys for approx $2.025B) until its next schedule is published Tuesday.

EGB/GILT SUMMARY: Schnabel Echoes Lagarde's Inflation Risk Comments

European sovereign bonds trade mixed this morning and have not materially departed from Friday's closing levels.

- Gilts firmed early in the session, but subsequently trade back towards the Friday close.

- The bund curve trades close to flat on the day.

- It is a similar story for OATs, which have so far lacked clear direction.

- The ECB's Isabel Schanbel stated that long-term bottlenecks could lead to higher inflation and that this was being monitored diligently. Schnabel's comments echo President Lagarde, who last week acknowledged the risk of higher inflation.

- President Lagarde will participate in a discussion with the Financial Times' Martin Wolf at 1430GMT today.

- Supply this morning came from Germany (Bubills, EUR3.867bn). Later today France will offer EUR5.6-6.8bn) of BTFs.

- The European data slate was light this morning with not tier one releases.

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXV1 172.50p, sold at 95/94/92 in ~9k

RXV1 173.5/174.5cs, bought for 3.5 in 1k

RXV1 170p, bought for 9 in 2k

RXV1 171.50/171.00ps 1x1.5, bought for 4.5 in 1k

FOREX: Extension of Oil Bounce Works in Favour of NOK, CAD

- A more solid session for equity markets Monday is dictating price action across currencies, with a solid start across core Europe weighing on haven currencies. As a result, CHF and JPY are among the weakest performers across G10, with oil-tied CAD and NOK at the top of the pile.

- The move in CAD and NOK reflects the $2.50/bbl climb off the Friday lows for WTI crude futures, aiding USD/NOK's slip back toward last week's lows. A slip below 8.6073 opens declines toward the 100-/200-dmas at 8.5886/8.5569.

- The USD index is in modest positive territory, with last week's highs already under pressure. A solid clearance back above 92.877 opens gains toward 93.0483 (61.8% Fib for the late August down-move) as well as 93.181, the Aug 27 high.

- Data releases are few and far between Monday, keeping focus on central bank speak. ECB's Lagarde is due to be speaking from the Aspen International Conference at 1430BST/0930ET on the topic of women in finance.

FX OPTIONS: Expiries for Sep13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1975-85(E1.1bln)

- AUD/USD: $0.7350-60(A$629mln)

- NZD/USD: $0.6990-10(N$697mln), $0.7088(N$705mln)

- USD/CNY: Cny6.4500($580mln)

Price Signal Summary - USD Continues To Find Support

- In the equity space, S&P E-minis traded lower Friday and in the process cleared the 20-day EMA. This signals potential for a deeper pullback towards the key 50-day EMA at 4405.55. Key resistance is at 4539.50, the Sep 3 high. EUROSTOXX 50 futures remain above 4132.50, Sep 9 low. A clear break of this level would expose 4078.00, Aug 19 low. The bull trigger is unchanged at 4252.00, Sep 6 high.

- In FX, EURUSD has started the week on a soft note and traded through last week's low of 1.1802, Sep 8 low. The break signals scope for a deeper pullback and has opened 1.1758. Recent activity in GBPUSD has defined short-term directional parameters at; 1.3892 as resistance, Sep 3 high and support at 1.3727, Sep 8 low. A break of either level would provide a clearer directional signal.

- On the commodity front, Gold has pulled back from recent highs and is consolidating just ahead of recent lows. The near-term outlook remains bullish but a break of $1834.1, Jul 15 high is required to confirm a resumption of gains. Support to watch is $1774.5, Aug 19 low. A break would threaten a bull theme. WTI futures remain in a bull mode. The focus is on $70.74, 76.4.% retracement of the Jul 30 - Aug 23 sell-off and $71.44, the bear channel top drawn from the Jul 6 high.

- In FI, Bund futures remain vulnerable following last week's move lower. The focus is on 171.30, 2.382 projection of the Aug 5 - 11 - 17 price swing. Resistance to watch is 172.76, Sep 2 and 3 high. Gilt futures remain in a bear mode following last week's breach of support at 128.03, the Jul 6 low (cont). This opens 127.65, 61.8% of the Jun 3 - Aug rally (cont).

EQUITIES: Stocks Start Week Positively, But Well Shy of Last Week's Highs

- Equity markets have started the week on the front foot, with cash European indices higher by 0.5-0.8%. The recovery is further reflected in US futures, with the e-mini S&P higher by over 20 points at pixel time.

- Across Europe, the energy sector is leading the bounce - helped higher by the $2.50/bbl recovery in oil prices. Utilities and financials also trade more favourably.

- Despite the positive across Europe, US futures remain well below Friday's best levels, keeping a more solid bounce in check for now. Markets need to top 4509.20 to improve the near-term outlook, which looks far more fragile after last week's price action. On the weekly chart, last week marked the first week in 14 in which the e-mini S&P failed to print a new alltime high.

COMMODITIES: Oil Bounce Extends, Eyes Bear Channel Top

- US energy markets trade well, with WTI crude futures extending the bounce off Friday's lows to $2.50/bbl. Strength across crude oil markets continues to play catch-up with NatGas, which holds close to $5.00/MMBtu.

- The oil squeeze persists as markets continue to eye the particularly sluggish return of production from the Gulf following the lingering aftermath of Hurricane Ida.

- Prices also remain supported by persistent coverage of an expected supply squeeze across Winter, with Bank of America this morning flagging the risk of $100/bbl oil prices should winter be colder than usual - with oil demand lurching higher by 1-2mln bpd.

- Precious metals markets are more muted with gold broadly unchanged, although silver modestly underperforms.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok