Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

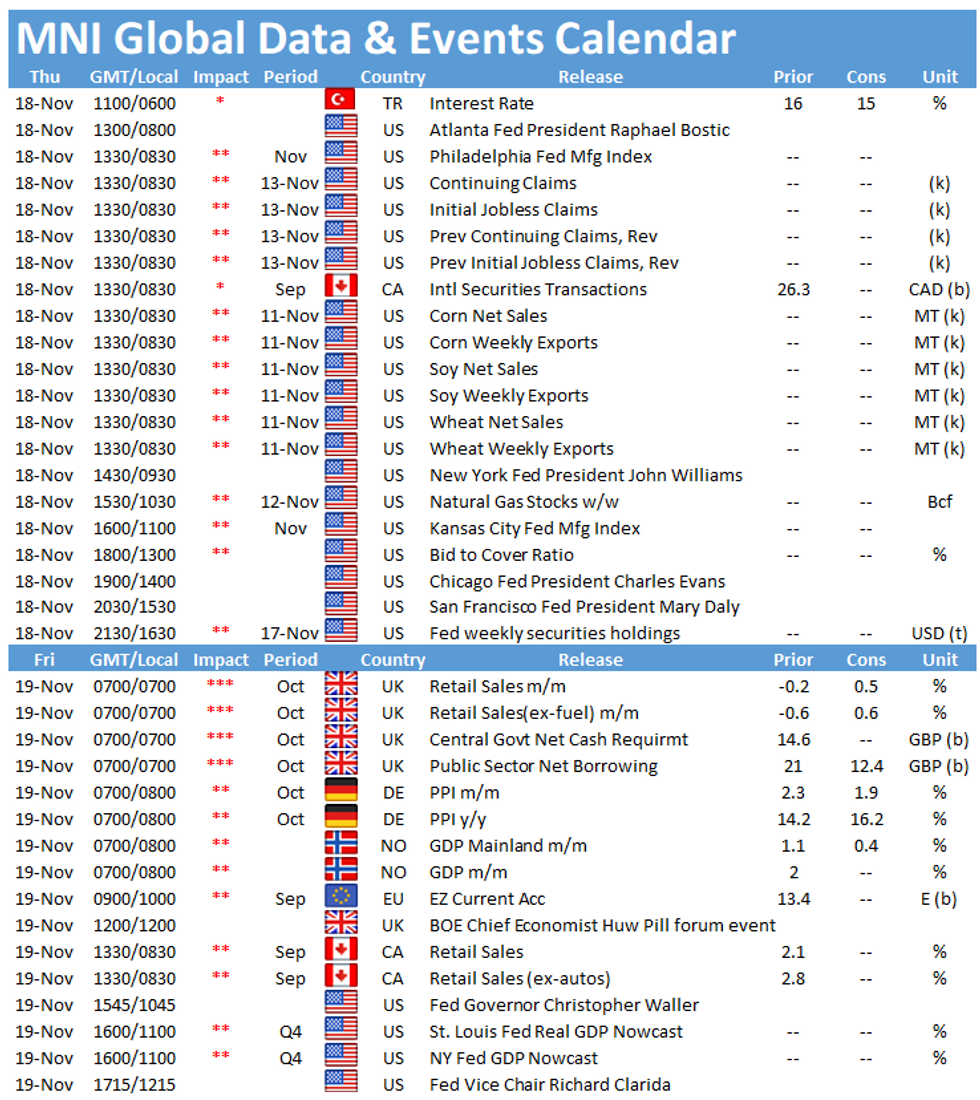

- Markets testing the resolve of the SNB

- Equities recover off lows following Wednesday losses

- Focus turns to Fedspeak & weekly jobless claims

US TSYS SUMMARY: Quiet Morning After Yesterday's Bull Flattening

- TYZ1 currently at low end of today's narrow range (130-15+) on low volumes, consolidating yesterday's 11 tick rally.

- Slight bear steepening in cash Tsys with 2Y unchg at 0.498%, 10Y up +1bps at 1.599% and 30Y up +1.4bps at 1.990%, after 30Y in particular rallied 4bps yesterday.

- Fedspeak from Bostic (0800ET), Williams (0930ET), Evans (1400ET) and Daly (1530ET). Evans, normally on dovish end of the spectrum, said yesterday that inflation strength has persisted longer than he expected.

- Data on light side with jobless claims and Philly Fed for Nov, potential upside in latter as seen unchg despite strength in Monday's Empire survey.

- 10Y TIPS auction 1300ET and end of month supply announcement from the Treasury.

- Next scheduled NY Fed purchase today 1010-1030ET for Tsy 22.5-30Y (appr. $1.600B).

- Markets also digest a busier corporate pipeline, with over $53B in deals set to launch this week (as of Tue close but with only three names seen so far and likely to pick up today). Highlights include $6.7B from Canadian Pacific Railway as well as $4B from Barclays.

EGB/GILT SUMMARY: Gaining Ground

European sovereign bonds have rallied this morning with gilts leading the charge.

- Gilts yields uniformly 3bp lower on the day. Short sterling futures are 4.0-5.5 ticks lower in reds and greens.

- The ECBs Centeno earlier repeated the official line that inflation remains a 'temporary phenomenon'.

- Bunds have firmed and the curve has marginally bull flattened with the 2s30s spread narrowing by 1bp.

- There has been a sharper flattening of the OAT curve on the back of the short-end trading weaker and the longer end rallying. The 2s30s spread is 4bp narrower on the day.

- BTP cash yields are 1-3bp lower.

- Supply this morning came from France (OATs, EUR7.494bn & Linkers, EUR1.746bn), Spain (Bono/Oblis, EUR4.115bn) and Ireland (IRTBs, EUR750mn).

- The European data slate was slight. Focus today will be on US jobless claims and the Philly Fed update.

EUROPE ISSUANCE UPDATE

France sells:- E3.047bln 0% Feb-24 OAT, Avg yield -0.69% (Prev. -0.63%), Bid-to-cover 2.86x (Prev. 2.31x)

- E2.598bln 0% Feb-27 OAT, Avg yield -0.37% (Prev. -0.42%), Bid-to-cover 2.56x (Prev. 2.51x)

- E1.849bln 2.75% Oct-27 OAT, Avg yield -0.37% (Prev. -0.42%), Bid-to-cover 2.92x (Prev. 2.39x)

- E565mln 0.10% Mar-26 OATei, Avg yield -2.38% (Prev. -2.29%), Bid-to-cover 3.41x (Prev. 3.37x)

- E573mln 0.10% Mar-28 OATi, Avg yield -1.79% (Prev. -1.71%), Bid-to-cover 2.48x (Prev. 3.30x)

- E608mln 0.70% Jul-30 OATei, Avg yield -1.99% (Prev. -1.41%), Bid-to-cover 2.28x (Prev. 2.79x)

- E1.489bln 0% Jan-27 Bono, Avg yield -0.1140% (Prev. -0.0890%), Bid-to-cover 1.62x (Prev. 1.35x)

- E865mln 0.60% Oct-29 Obli, Avg yield 0.1780% (Prev. 0.2720%), Bid-to-cover 2.32x (Prev. 2.69x)

- E1.761bln 0.50% Oct-31 Obli, Avg yield 0.4650% (Prev. 0.4830%), Bid-to-cover 1.40x (Prev. 1.32x)

EUROPE OPTION FLOW SUMMARY

Eurozone:

OEZ1 135/134.5ps, sold at 7 in 3k

DUZ1 134.75/134.25ps, bought for 4 in 1.5k

DUG2 112.00p, bought for 9 in 2k

US:

TYZ1 129.50/129ps, bought for 2 in 15k

FOREX: Markets Testing SNB Tolerance

- JPY is the poorest performer on the day, but the pullback pales in comparison to the strength seen into the Wednesday close. USD/JPY looks to the 114.00 handle as a near-term anchor, with markets needing to retake 114.97 to reignite the upside argument, while a break below 113.76 would prove bearish.

- EUR/CHF remains a focus, with markets watching the cross testing the key support seen ahead of the 1.05 handle. 1.0503 remains the low print so far, with traders looking to gauge the SNB's implied tolerance level for the cross.

- NZD is the strongest currency in G10, with the currency taking the lead from 2yr inflation expectation data released overnight, which surged to 2.96% from 2.27% previously - the highest rate since 2011. NZD/USD rallied to narrow the gap with the 50-dma of 0.7056. A break above here would see the short-term outlook improve toward 0.71 and the 200-dma.

- Data in focus later today includes weekly US jobless claims, with markets expecting a modest improvement in claims, seen dropping to 260k. Fed speakers remain plentiful, with Fed's Williams likely the focus - he speaks on transatlantic responses to the pandemic. Others include Evans, Bostic and Daly, but don't appear policy-oriented.

FX OPTIONS: Expiries for Nov18 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1290(E552mln), $1.1330-50(E646mln), $1.1450-60(E941mln)

- USD/JPY: Y113.90-05($1.4bln), Y114.20-25($1.3bln), Y114.50-55($521mln), Y115.00($510mln)

- GBP/USD: $1.3400(Gbp896mln)

- EUR/GBP: Gbp0.8400(E1.1bln), Gbp0.8450-60(E1.1bln)

- USD/CAD: C$1.2330($1.3bln), C$1.2380($770mln), C$1.2500($1.0bln)

- USD/CNY: Cny6.3830($1bln)

Price Signal Summary - Equity Space Still Bullish

- In the equity space, S&P E-minis are holding onto this week's gains. Attention is on 4717.00 next, 1.50 projection of the Jul 19 - Aug 16 - Aug 19 price swing. Initial support to watch is 4622.04, the 20-day EMA. EUROSTOXX 50 futures uptrend remains intact and the contract continues to register a fresh trend high. The focus is on 4420.80, 1.382 projection of the Jul 19 - Sep 6 - Oct 6 price swing.

- In FX, EURUSD traded lower yesterday and breached key support at 1.1300, the base of a bear channel drawn from the Jun 1 high. A clear break and continued bearish follow through would open 1.1222, 1.618 projection of the Jan 6 - Mar 31 - May 25 price swing. The recent break in GBPUSD of 1.3412, Sep 29 low, opens 1.3334 next, 1.00 projection of the Sep 14 - 29 - Oct 20 price swing. For now though, the pair continues to correct higher. Watch resistance at 1.3547, the 20-day EMA. EURGBP remains heavy following this week's sharp sell-off and breach of 0.8403, Oct 26 low. This has opened 0.8356, Feb 26 low. USDJPY has breached resistance at 114.70, the Oct 20 high. The break higher confirms a resumption of the underlying uptrend and opens 115.51 next, the Mar 10, 2017 high. A concern for bulls is yesterday's bearish engulfing candle. A deeper pullback would expose key support at 112.73, Sep 9 low. EURCHF is challenging1.0505, the May 14, 2020 low. A break would (potentially) expose the cross to a deeper sell-off below 1.0500.

- On the commodity front, Gold is consolidating but remains bullish. Attention is on $1877.7, Jun 14 high and $1903.8, Jun 8 high. WTI has traded through key short-term support at $78.25, Nov 4 low. The break suggests scope for a deeper corrective pullback towards $76.13, 38.2% retracement of the Aug 23 - Oct 25 rally .

- In the FI space, Bund futures maintain a bullish short-term tone and the contract remains above support at 170.06, Nov 5 low. The focus is on 171.95, 61.8% of the Aug - Nov sell-off. Gilts also maintain a firmer tone and the recent pullback is considered corrective. A resumption of strength would suggest potential for a climb towards 127.69 next, Sep 21 high. Initial support has been defined at 125.40, Nov 17 low.

EQUITIES: Stocks on Front Foot, Recovering Off Negative Wednesday Close

- US equity futures sit in positive territory, rebounded modestly off the negative cash close on Wall Street Wednesday. The e-mini S&P trades higher by just over 15 points, but remains shy of the week's best levels printed up at 4643 on Tuesday.

- European markets are more mixed, with upside across EuroStoxx50, German and French markets countered by slippage across UK, Spanish and Italian names.

- The S&P E-minis outlook remains bullish and futures remain above recent lows. Another all-time high print on Nov 5 confirmed a resumption of the uptrend and the focus is on 4717.00 next, a Fibonacci projection.

COMMODITIES: Oil Offered as Biden/Xi Threat Continues to Weigh on Prices

- WTI and Brent crude futures have extended weakness initially triggered on Tuesday as markets eyed speculation that Xi and Biden could coordinate to act against high energy prices globally. This was compounded by the weekly DoE inventories data, which showed a sizeable draw from the SPR of just over 3mln bbls.

- WTI has slipped through the Wednesday lows, printing down at $77.08 for the Dec-21 contract. This puts prices at the lowest levels since early October as the previously bullish condition unwinds. $76.13 marks the first key support, the 38.2% retracement of the Aug 23-Oct 25 rally.

- Gold remains bullish. Prices rallied sharply higher last week resulting in a clear break of resistance at $1834.0, Sep 3 high. The breach of this hurdle reinforces current bullish conditions and paves the way for further strength near-term. Note too that gold has also breached $1863.3, 76.4% of the Jun - Aug sell-off.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok