Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Mixed equity outlook with Europe more stable, while US still at risk of correction

- USD/CAD circling key support

- US CPI, Fedspeak eyed as market remains sensitive to inflation risks

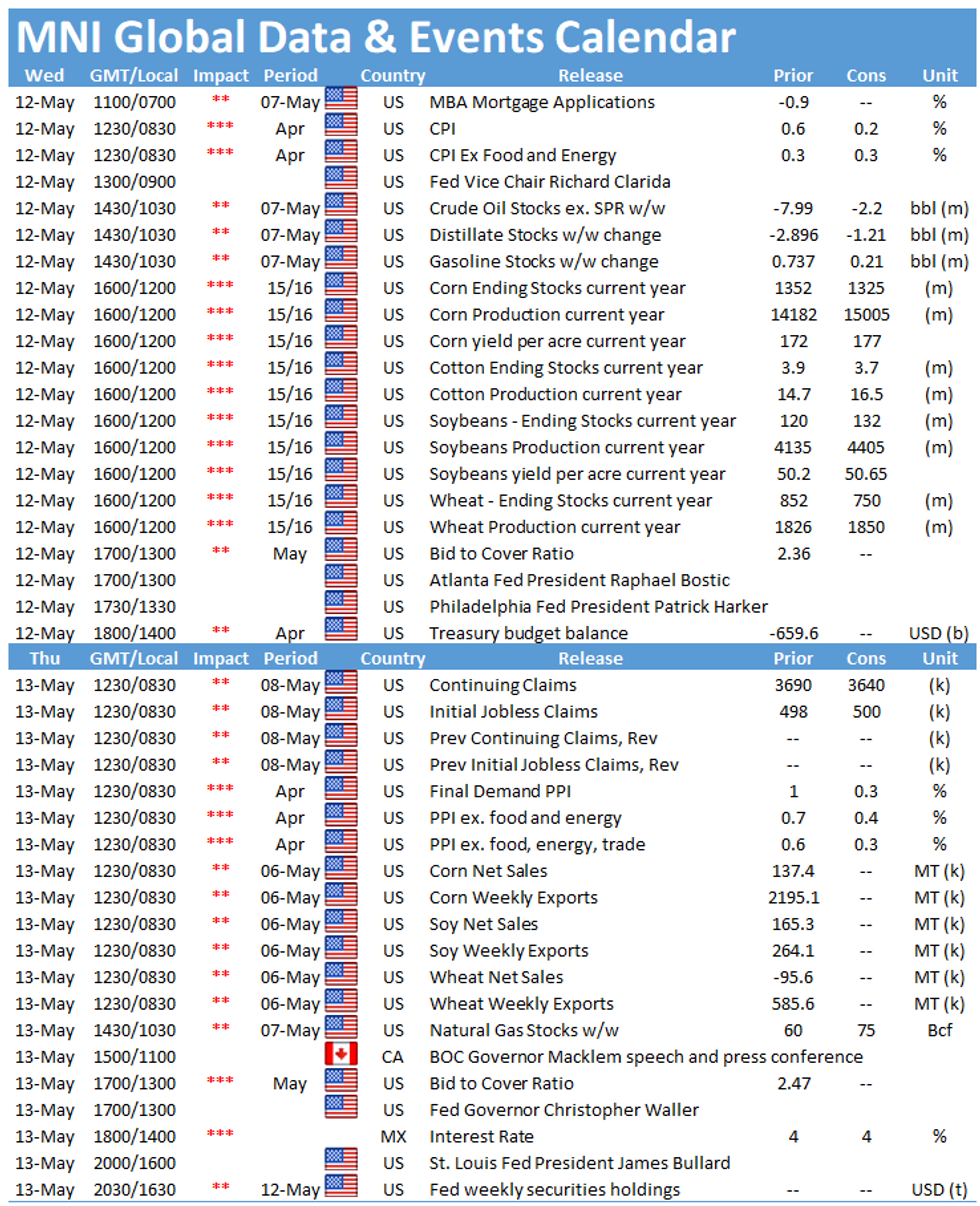

US TSYS SUMMARY: Edging Higher Ahead Of Apr Inflation Report, 10-Year Supply

Treasuries have edged higher from overnight lows with a bit of bull flattening early Wednesday, in anticipation of key inflation data and 10-Yr supply.

- The 2-Yr yield is down 0.4bps at 0.1549%, 5-Yr is down 0.8bps at 0.7918%, 10-Yr is down 1.1bps at 1.6112%, and 30-Yr is down 1.7bps at 2.328%. Jun 10-Yr futures (TY) up 2.5/32 at 132-17 (L: 132-12.5 / H: 132-17.5)

- The main event of the day/week is the April CPI report at 0830ET - headline expected to slow to 0.2% M/M from +0.6% prior; but core seen keeping up the pressure at +0.3% from +0.3% prior. Both seen spiking Y/Y on base effects.

- It's the highest consensus for M/M core since the 1990s, so arguably a low bar is in place for a downside miss (more on this shortly, incl some sell-side previews).

- The other key event on the schedule is the $41B 10-Yr note auction at 1300ET (also $35B in 119-day bill supply at 1130ET). NY Fed buys ~$1.75B of 20-30Y Tsys.

- Fed speakers keep coming, but not all are econ/mon-pol focused subjects: 0900ET is prob the most important, w VC Clarida on the economic outlook (text and Q&A), 0905ET Boston's Rosengren on crypto; 1300ET Atlanta's Bostic in a webinar w CFR; 1330ET Philly's Harker on Higher Education.

EGB/GILT SUMMARY: Brief Respite

European sovereign bonds have traded firmer this morning, partially recovering some of yesterday's sell off. Equities have similarly stabilized after a bout of selling on the back of reemerging inflation concerns.

- The gilt curve has bull flattened with the 2s30s spread 2bp narrower.

- Bund yields have edged down 1bp.

- OAT yields are similarly 1-bp lower on the day.

- The BTP curve has flattened with the 2s30s spread trading down 1bp

- Supply this morning came from Italy (BOTs, EUR7.5bn), and Portugal (OTs, EUR1.25bn).

- Headline UK GDP data for the first quarter came in slightly better than expected in Q/Q terms (-1.5% Q/Q vs -1.6% survey) with government spending doing much of the heavy lifting. The latest monthly GDP print for March surprised higher (2.1% M/M vs 1.5% consensus).

EUROPE ISSUANCE UPDATE: Portuguese Auction

Portugal sells 10/15y OTs:

E0.551bln 0.30% Oct-31 OT, Avg yield 0.51% (Prev 0.34%), Bid-to-cover 2.47x

E0.699bln 0.90% Oct-35 OT, Avg yield 0.84% (Prev 0.32%), Bid-to-cover 1.68x (Prev 2.55x)

EUROPE OPTION FLOW SUMMARY

Eurozone:

RXM1 168/167ps, bought for 6 in 4.5k

RXM1 169/168ps, bought for 20 in 3k

RXN1 171/169ps 1x2, bought for 28.5/29 in 1.5k

FOREX: USD/CAD Continues to Test Key Support

- CAD is the strongest currency in G10 ahead of Wednesday's NY open, with USD/CAD keeping key support at 1.2062 under pressure. A break through here would be a sizeable break of support for the pair, leaving USD/CAD at the lowest levels since 2015. Better WTI and Brent crude markets are supporting the price here, with a firm crude futures curve underpinning CAD strength.

- At the other end of the table, AUD and NZD trade poorly, with continued weakness in US index futures draining risk sentiment. Immediate support for NZD/USD undercuts at $0.7205, with long covering in AUD/USD also adding pressure.

- Plenty of focus will be paid to today's US CPI release, with markets expecting Y/Y CPI to tick higher to 3.6%, the highest since 2011. Inflationary concerns have been the primary driver of markets this week, so the market response to today's release could be outsized.

FX OPTIONS: Expiries for May12 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.2000(E542mln)

- USD/JPY: Y108.25-35($769mln), Y109.95-00($783mln)

- AUD/USD: $0.7900(A$619mln)

- USD/CAD: C$1.2800($610mln)

Price Signal Summary - S&P E-minis Breach Support

- In the equity space, S&P E-minis remain vulnerable following this week's pullback. The bull channel support drawn off the Mar 4 low has been cleared and 4110.50, Apr 20 low has been probed. An extension lower would open 4061.48, 50-day EMA.

- In FX, EURUSD maintains a firmer tone following the recent climb from 1.1986, May 5 low and the break of 1.2150, Apr 29 high. The focus is on 1.2184, Feb 26 high and 1.2243, Feb 25 high. GBPUSD is firm following Monday's strong rally and attention is on 1.4237, Feb 24 high and this year's high. USDJPY support has been defined at 108.34, May 7 low. A bullish theme remains intact while it holds and attention is on 109.70, May 3 high. A break of support would highlight a trendline break drawn off the Jan 6 low and risk a deeper pullback.

- On the commodity front, Gold is holding onto gains and the outlook remains bullish. Last week's climb has opened $1851.5, 61.8% retracement of the Jan 6 - Mar 8 sell-off. Oil is off recent highs but the uptrend remains intact. The Brent (N1) focus is on the psychological $70.00 level and $71.75, Jan 8 2020 high (cont). Watch key support at $66.10, May 3 low. WTI bulls are eyeing the key resistance at $67.29, Mar 8 high. Support at $62.91, May 3 low is key.

- In the FI space, Bunds (M1) remain vulnerable and attention is on the major support at 169.24, Feb 25 low and the bear trigger. Near-term risk in Gilts is still skewed to the downside. The next support and intraday bear trigger is at 127.32, Apr 1 low.

EQUITIES: Continental Stocks Stabilise, But Still Signs of US Weakness

- After a volatile Monday/Tuesday session, European equity markets have stabilised ahead of the Wednesday open, with UK's FTSE-100 leading the bounce to trade higher by 0.6%. The EuroStoxx50 is the laggard, off around 0.1%.

- Despite better performance in Europe, US markets are more fragile, with tech again a cause for concern as the NASDAQ futures points to a lower open of around 0.5% or so.

- Across Europe, tech is the weakest sector, with financials also trading soft. Utilities and staples are the firmest so far, confirming the cautious tone despite higher headline indices.

COMMODITIES: Supply Scramble Persists, As Colonial Pipeline Plans Eyed

- A supply crunch in the Southern US states and sporadic reports of panic buying continues to support gasoline prices, with RBOB gasoline prices support above $2.10/gallon. Focus turns to the plans expected to be outlined by the Colonial Pipeline CEO later today, at which the company are expected to confirm plans to return pipelines back to full capacity.

- Elevated gas prices have bled through into WTI and Brent crude futures, which are both headed higher into Wednesday's NYMEX open.

- Precious metals are in minor negative territory, with gold off around 0.2% and inline with Tuesday's open. Markets remain a little firmer off the Tuesday low at $1,818.13, which undercuts as first support. Silver sees similar weakness, keeping the gold/silver ratio unchanged.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.