Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

Highlights:

- NZD seen as most sensitive over CPI

- Markets see Y/Y core and headline inflation pressures moderating

- Litany of Fedspeak to digest, with Barkin, Logan, Harker and Williams due

US TSYS: Modest Bull Steepening Ahead of CPI, Fedspeak

- Ahead of US CPI, cash Tsys have continued a move richer than started late in yesterday’s session for the front-end and earlier on in the day for the long-end after the 10YY twice failed to sustain a nudge above 3.75%. Today’s modest bull steepening after yesterday’s twist flattening keeps 2s10s relatively rangebound at -80bps.

- 2YY -2.5bp at 4.495%, 5YY -2.3bp at 3.888%, 10YY -1.3bp at 3.688% and 30YY -0.8bp at 3.765%.

- TYH3 trades 7 ticks higher at 113-00, just off an earlier high of 113-01+ on unsurprisingly below average volumes ahead of CPI. The push higher has seen the contract move away from trendline support at 112-14+ (drawn from Oct 21 low) whilst resistance remains at the 50-day EMA of 114-00+.

- Data: CPI Jan (0830ET), Real av earnings Jan (0830ET)

- Fedspeak: Barkin (0930ET), Logan (1100ET, text), Harker (1130ET, text) and Williams (1405ET, text).

- Bill issuance: US Tsy $25B 12 Day CMB auction (1130ET)

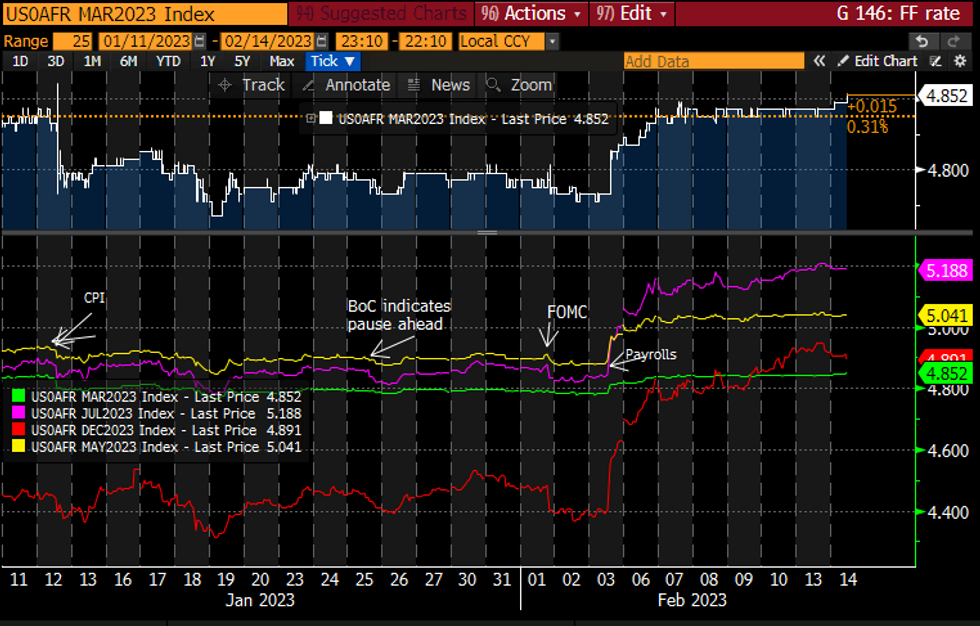

STIR FUTURES: Fed Terminal Nudges Lower Pre-CPI

- Fed Funds implied hikes have edged higher for Mar (27.5bp, +1bp) but sit softer thereafter in a continuation of a steady move lower in the second half of yesterday’s session.

- It’s a small move after post-payrolls surges though, with a cumulative 46bp for May (unch), 61bp to a terminal 5.19% Jul (-1bp) and 29bp of cuts to 4.90% Dec (-2bp).

- Four FOMC members lined up post-CPI, including three current voters with text - Logan & Harker (’23 voters), Williams (voter) – but first with Barkin (’24) in a BBG interview.

FOMC-dated Fed Funds futures implied ratesSource: Bloomberg

FOMC-dated Fed Funds futures implied ratesSource: Bloomberg

FOREX: Markets See ZAR, NZD and SEK as Most Sensitive Over CPI

- Front-end vols are well bid across all USD pairs in anticipation of the US CPI release later today, and the potential impacts for Fed policy going forward. Using implied vol gains as a gauge, markets see NZD, SEK and AUD amoang the most market sensitive over the release in DM, while ZAR is among the most exposed in emerging markets space.

- The two-day gain in overnight vol for NZD/USD amounts to near 19 points, meaning an ATM straddle are priced for a 72 pip swing in the pair - around three times the size of the overnight swing priced in at the tail-end of last week.

- Markets continue to hold a small net long NZD position, as per the most recent CFTC data, although the position has moderated in recent weeks to represent 6.6% of open interest. This contrasts with AUD, with the current short position amounting to just over 25% of OI.

FOREX: USD Fades as Equities Look Constructive Pre-CPI

- The EUR trades well, with the single currency firmer against most others. EUR/USD has traded an intraday high at 1.0767, although prices remain shy of the 1.0791 Thursday high for now. Equity futures are modestly firmer, with the e-mini S&P building on the late Monday gains and helping drive a modest USD downtick into NY hours.

- NZD is underperforming, slipping against all others in G10 following inflation expectations data overnight. 2y inflation is seen at 3.30% for Q1, down from 3.62% late last year - feeding into the view that inflation may have peaked for now.

- USD/JPY has snapped overnight Asia-Pac weakness to rise back above the Y132 handle at the crossover, narrowing the gap with first resistance at Y132.91.

- The US inflation report is the highlight Tuesday, with markets expecting a pick up in monthly CPI to 0.5%, but a moderation in headline CPI to 6.2% and 5.5% for core metrics. Post-inflation Fedspeak will also be carefully watched, with Barkin, Logan, Harker and Williams all slated to speak.

FX OPTIONS: Expiries for Feb14 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.0600-05(E1.0bln), $1.0700(E2.3bln), $1.0800(E554mln), $1.0845-50(E772mln)

- USD/JPY: Y132.50($551mln), Y133.00($628mln)

EQUITIES: E-Mini S&P Trend Conditions Bullish Following Monday Price Action

- EUROSTOXX 50 futures traded higher Thursday last week to breach 4265.00, the Feb 3 high. Despite the pullback from last week’s best levels, the fresh cycle high confirms a resumption of the uptrend and opens 4303.20, the 2.382 projection of the Sep 29 - Oct 4 rise from the Dec 20 low. Note that the trend is overbought. A pullback would represent a healthy correction. Key support lies at 4097.00, the Jan 19 low. Initial support is at 4167.50, the 20-day EMA.

- The S&P E-Minis trend condition is bullish and the latest pullback is considered corrective. The contract has pierced initial support at 4069.52, the 20-day EMA. Firmer support lies at the 50-day EMA, at 4006.63. A clear break of this average would signal scope for a deeper pullback and potentially highlight a reversal. Key resistance and the bull trigger intersect at 4208.50, the Feb 2 high. A breach would resume the uptrend.

COMMODITIES: WTI Futures Contract Print Fresh Feb High Monday

- WTI futures showed above the Friday high ahead of the Monday close, marking an extension of the recovery from $72.25, the Feb 6 low. The rally has confirmed a break of the 50-day EMA, at $78.34, strengthening the current bull cycle and note that price has pierced $80.22, 76.4% of the Jan 18 - Feb 6 bear leg. A clear break of this level would expose the key resistance at $82.66, the Jan 18 high. On the downside, initial firm support has been defined at $76.52, the Feb 9 low.

- Trend conditions in Gold are bearish for now, and the yellow metal remains in a corrective cycle. This follows the strong sell-off on Feb 2 / 3 and sights are on the 50-day EMA, at $1855.5. The average represents a key support and has been pierced. A clear break would strengthen a bearish case and suggest scope for a deeper pullback - towards $1825.2, the Jan 5 low. On the upside, key resistance and the bull trigger is at $1959.7, the Feb 2 high.

| Date | GMT/Local | Impact | Flag | Country | Event |

| 14/02/2023 | 1000/1000 | ** |  | UK | Gilt Outright Auction Result |

| 14/02/2023 | 1000/1100 | *** |  | EU | GDP (p) |

| 14/02/2023 | 1000/1100 | * | | EU | Employment |

| 14/02/2023 | 1100/0600 | ** |  | US | NFIB Small Business Optimism Index |

| 14/02/2023 | - | | EU | ECB de Guindos at ECOFIN Meeting | |

| 14/02/2023 | 1330/0830 | *** | | US | CPI |

| 14/02/2023 | 1355/0855 | ** | | US | Redbook Retail Sales Index |

| 14/02/2023 | 1600/1100 | | US | Dallas Fed's Lorie Logan | |

| 14/02/2023 | 1630/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 14/02/2023 | 1800/1300 | | US | Philadelphia Fed's Patrick Harker | |

| 14/02/2023 | 1905/1405 | | US | New York Fed's John Williams | |

| 15/02/2023 | 0700/0700 | *** | | UK | Consumer inflation report |

| 15/02/2023 | 0700/0700 | *** | | UK | Producer Prices |

| 15/02/2023 | 0800/0900 | *** |  | ES | HICP (f) |

| 15/02/2023 | 0930/0930 | * | | UK | ONS House Price Index |

| 15/02/2023 | 1000/1100 | ** | | EU | Industrial Production |

| 15/02/2023 | 1000/1100 | * | | EU | Trade Balance |

| 15/02/2023 | 1200/0700 | ** | | US | MBA Weekly Applications Index |

| 15/02/2023 | 1315/0815 | ** |  | CA | CMHC Housing Starts |

| 15/02/2023 | 1330/0830 | *** | | US | Retail Sales |

| 15/02/2023 | 1330/0830 | ** | | US | Empire State Manufacturing Survey |

| 15/02/2023 | 1400/0900 | * | | CA | CREA Existing Home Sales |

| 15/02/2023 | 1400/1500 | | EU | ECB Lagarde at Plenary Debate on ECB Annual Report | |

| 15/02/2023 | 1415/0915 | *** | | US | Industrial Production |

| 15/02/2023 | 1500/1000 | * | | US | Business Inventories |

| 15/02/2023 | 1500/1000 | ** | | US | NAHB Home Builder Index |

| 15/02/2023 | 1530/1030 | ** | | US | DOE Weekly Crude Oil Stocks |

| 15/02/2023 | 1800/1300 | ** | | US | US Treasury Auction Result for 20 Year Bond |

| 15/02/2023 | 2100/1600 | ** | | US | TICS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok