Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

HIGHLIGHTS:

- Sharp drop in yields across Asia-Pac gives way to large rebound in Europe

- Crude little changed as Iranian President-elect reaffirms desire to remove Iranian sanctions

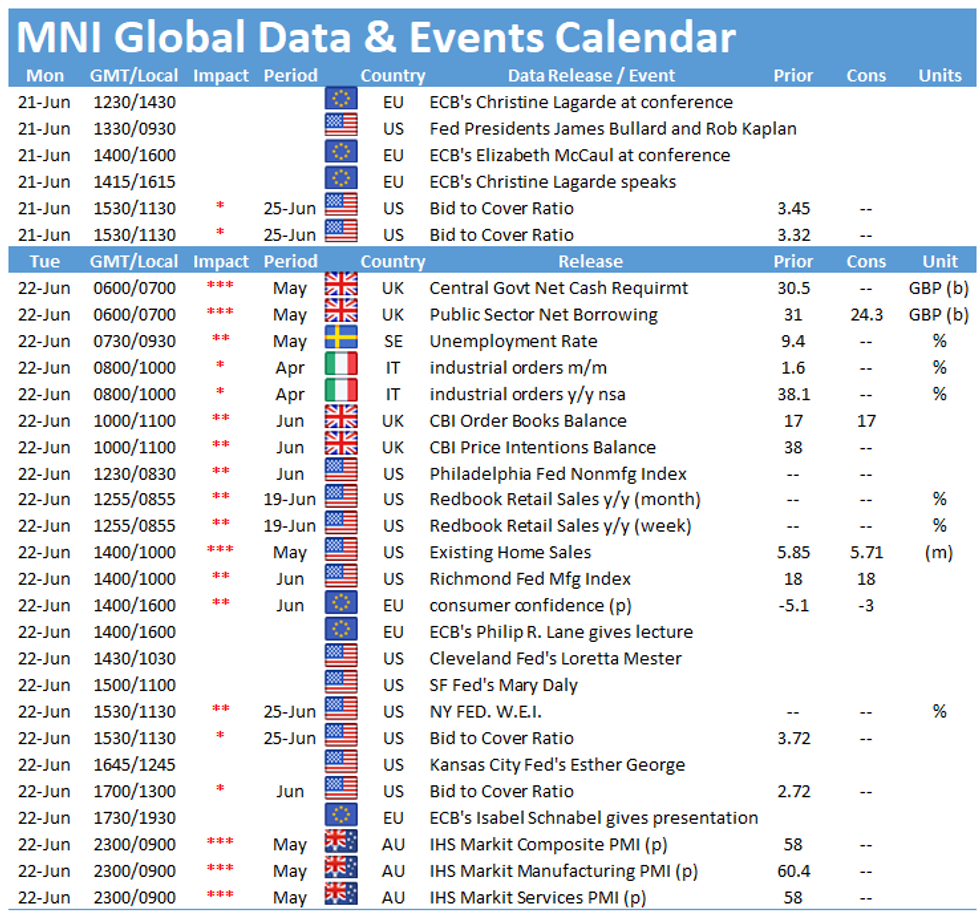

- Fedspeak in focus, with Bullard, Kaplan and Williams due

US TSYS SUMMARY: Sharp Reversal Overnight, With Fed Speakers Eyed

The week has kicked off with a sharp drop in yields in Asia-Pac followed by a large rebound in Europe, as markets continue to digest last week's hawkish Fed turn. A fairly quiet schedule ahead but FOMC speakers will continue to be closely watched following last week's unexpectedly hawkish shift.

- The 2-Yr yield is up 0.4bps at 0.2583%, 5-Yr is up 0.5bps at 0.8795%, 10-Yr is down 0.4bps at 1.4346%, and 30-Yr is up 1.7bps at 2.03%.

- But those relatively modest moves understate wide ranges: 10Y yields touched a fresh post-Feb low of 1.3526% (as Asian equities tumbled) before rebounding. 30-Yr yields higher on the session after dipping well below 2% (1.9259% low).

- Sep 10-Yr futures (TY) up 3.5/32 at 132-13.5 (L: 132-11 / H: 132-30), with an impressive ~660k volume.

- Scheduled Fed speakers include St Louis' Bullard and Kaplan (0945ET) in an event discussing the economic outlook (with Q&A); they're two of the 7 2022 hikes in the FOMC dot plot (Bullard said as much yesterday, and Kaplan surely kept his 2022 hike from the March meeting).

- Then NY Fed's Williams at 1500ET (incl Q&A) who may provide a better gauge of the current thinking of the FOMC "core", ahead of Chair Powell's Congressional appearance Tuesday.

- May Chicago Fed Nat'l Activity Index at 0830ET is the only data release.

- In supply, 3-M / 6-M bills (total $111B) auction at 1130ET. NY Fed buys ~$1.425B of 10Y-22.5Y Tsy.

EGB/GILT SUMMARY: Adjusting To The FOMC

It has been a mixed session so far for European government bonds following an initially strong start. The broader narrative is still anchored to the post-FOMC reassessment of inflation.

- OATs have outperformed this morning with yields 1-2bp lower. A poor showing in regional elections for President Macron and his far-right rival Marine Le Pen has given markets pause for thought ahead of the 2022 presidential election, which could be more fractured than people initially thought.

- Bunds initially traded firm but soon return to the Friday close.

- Gilts similarly trade close to flat on the day having initially opened higher.

- The Daily Telegraph reports that UK Treasury officials are looking into potential reforms to pension taxation as a possible tool for restoring the public finances in the aftermath of the pandemic. Such reforms, if pursued, would be a difficult sell for the Tory party, which was last week left unnerved by the loss of its Amersham and Chesham seat to the Lib Dems.

- Supply this morning came from Germany (Bubills, EUR5.274bn allotted), Netherlands (T-Bills, EUR2.92bn) and Slovakia (SlovGBs, EUR561mn).

- There are no Tier 1 European data releases today.

EUROPE ISSUANCE UPDATE

Slovakia sells 3/7/11/25-year SlovGBs:

- E124mln 0% Jun-24, Avg yield -0.56% (Prev. -0.57%), Bid-to-cover 1.17x (Prev. 2.55x)

- E78mln 1.00% Jun-28, Avg yield -0.26% (Prev. -0.26%), Bid-to-cover 1.73x (Prev. 1.64x)

- E215mln 1.00% May-32, Avg yield 0.17% (Prev. 0.25%), Bid-to-cover 1.07x (Prev. 1.66x)

- E144mln 2.00% Oct-47, Avg yield 0.87% (Prev. 1.00%), Bid-to-cover 1.21x (Prev. 1.35x)

EUROPE OPTIONS FLOW SUMMARY

Eurozone:

RXQ1 171.50/170.50ps 1x1.5, bought for 9.5 in 2k

RXQ1 170.5/170.0/169.5/168.5p condor, bought for 1 in 1.5k

FOREX: Extended Fed Reaction Continues to Roil Markets

- The extended reaction to last week's Fed rate decision continues to roil markets, with further US curve flattening keeping asset markets on their toes. The US dollar is edging off its recent highs, allowing the likes of EUR/USD and GBP/USD to recover off the lows printed late last week. The moves this morning, however, look corrective in nature, with the technical outlook still in favour of further greenback gains.

- As a result, the dollar is among the weakest in G10, with last week's hardest hit currencies, namely AUD, NZD and GBP, among Monday's best performers.

- Equity markets started the week poorly, but have undergone a decent reversal, with the e-mini S&P back in positive territory ahead of the Monday bell and indicating a stronger open.

- Tier one data releases are few and far between Monday, with Chicago Fed National Activity Index the sole release of note. Central bank speak may be of more consequence, with ECB's Lagarde on the docket (she speaks after the ECB met to discuss their policy strategy review this weekend) as well as Fed's Bullard, Kaplan and Williams.

Expiries for Jun21 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1900(E565mln), $1.1940(E553mln)

- USD/JPY: Y110.00($1.0bln)

Price Signal Summary - S&P E-Minis Tests The 50-Day EMA

- In the equity space, S&P E-minis traded below the 50-day EMA overnight. Levels below the 50-day EMA have this year resulted in a quick reversal of prior corrections and a resumption of the uptrend. Key short-term support has been defined at 4126.75, the intraday low and represents a potential risk parameter for bulls. Key trend resistance and the bull trigger is at 4258.25, Jun 15 high.

- In FX, EURUSD remains weak following last week's sharp sell-off and gains are considered corrective. Scope is seen for weakness towards 1.1837 next, 76.4% of the Mar 31 - May 25 rally. GBPUSD remains vulnerable following last week's bearish pressure. The pair has probed 1.3800 and this signals scope for 1.3717 next, Apr 16 low. USDJPY traded higher last week and breached 110.33, Jun 4 high. This reinforces a bullish theme with the focus on 110.97, the year high on Mar 31. Support to watch is at 109.72, today's intraday low.

- On the commodity front, Gold traded sharply lower last week and remains vulnerable. The focus is on $1756.2, low Apr 29. Upticks are considered corrective. Oil remains below recent highs and a corrective cycle is in play. Support in Brent (Q1) is seen at $71.56, the 20 day EMA. WTI (N1) support to watch lies at $69.26, the 20-day EMA.

- Within FI, Bund futures key directional triggers have been defined at; 171.80, Jun 17 low and 173.16, the Jun 11 high. The pullback in Gilt futures key support lies at 126.70, Jun 3 low.

EQUITIES: Stocks on the Bounce, But Friday's Highs A Way Off For Now

- Equity markets are modestly firmer early Monday, with the e-mini S&P higher by close to 20 points ahead of the opening bell. Global futures markets started poorly, extending last week's weakness to touch new cycle lows of 4126.75. But, losses were pared as Europe opened, prompting stocks to show above water. Nonetheless, the intraday recovery remains well short of the Friday highs, which mark first resistance at 4220 for the Sep-21 contract.

- Across Europe, cash markets are uniformly higher, but gains are modest at present, with the Eurostoxx50 higher by 0.5% while Spain's IBEX-35 lags slightly, but remains higher by 0.2%.

- Europe's materials and consumer staples sectors are leading the bounce, while healthcare, real estate and financials are the primary laggards.

COMMODITIES: Crude Little Changed as Iranian Election Goes Alongside Expectations

- WTI and Brent crude futures trade largely in line with last week's range, with the weekend's Iranian Presidential election results largely inline with expectations. This leaves diplomats negotiating the nuclear deal looking to a seventh round of discussions with Tehran after the new President-elect Raisi reaffirmed their intention to seek the removal of sanctions.

- This leaves directional parameters for WTI unchanged at last week's cycle high of $72.99/bbl.

- In precious metals space, gold and silver both trade higher, with a modest pullback in the dollar helping relieve some of the downside pressure evident in recent sessions. Gold support undercuts at $1761.1 Jun 18 low, while first resistance crosses at $1825.4.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok