Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

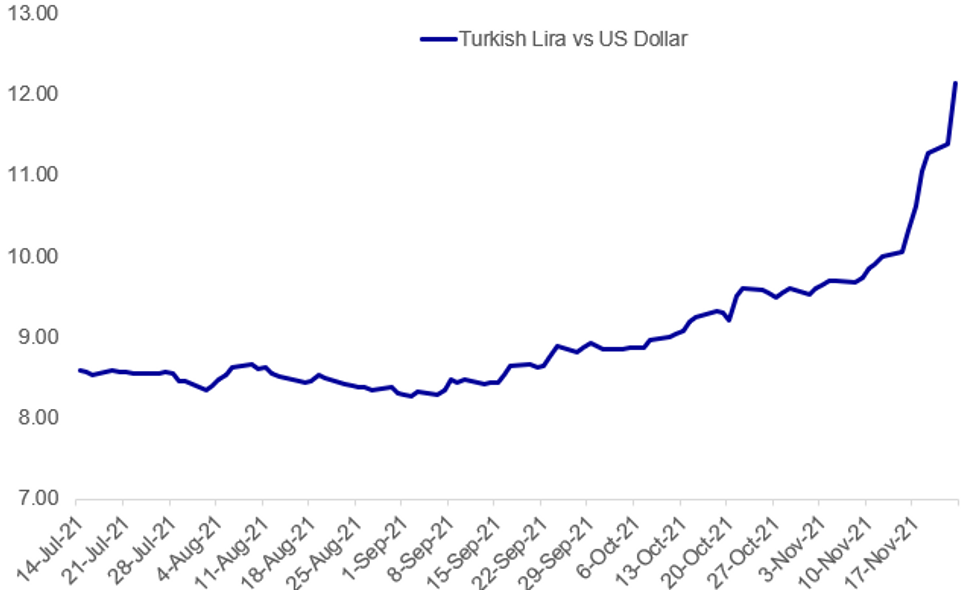

- TURKISH LIRA DROPS ANOTHER 8+% VS USD AS ERDOGAN SUPPORTS LOW RATES

- STRONG EUROZONE PMIS, BUT DETAILS MIXED

- UK PMI BEATS, DETAILS SOLID

- ECB'S SCHNABEL: UPSIDE INFLATION RISK, PEPP REINVESTMENTS GO ON

Fig. 1: Turkish Lira Drops To New Record Low Vs USD

Source: BBG, MNI

Source: BBG, MNI

NEWS:

TURKEY: Turkey President Erdogan defended lower interest rates this morning, sending TRY to a new low vs the USD. Erdogan said Turkey has abandoned old policies based on high borrowing costs and a strong currency in the name of slowing inflation, and instead shifted to a new set-up that prioritizes greater investments, exports and strong job creation. Also said there is a game being played by those using interest rates, the lira and inflation and that Turkey will crack down on "unfair, inexplicable price increases" by those using a weak lira as an excuse. "We know quite well what we're doing with the current policy, why we're doing it, and the kind of risks it entails and what we'll achieve at the end"

ECB: Net purchases under the ECB's PEPP programme should end in March next year, Executive Board member Isabel Schnabel said in an interview Tuesday, but PEPP itself will not, with flexible reinvestments possibly mitigating the need to transfer PEPP flexibility to APP. Short-run growth is likely to slow as a result of continued supply-side disruptions and the resurgence of the coronavirus, Schabel said, but the medium-term growth outlook continues to look strong. December's Eurosystem staff inflation projections are expected to be revised upwards, but, overall, inflation will decline over the forecast horizon.

ECB (BBG): European Central Bank Governing Council member Klaas Knot said new restrictions in parts of the euro area to battle record Covid-19 infections are unlikely to change the planned wind-down of monetary stimulus. While the measures "will surely have a moderating impact on economic activity, the impact on inflation will actually be more ambiguous, because it might also reinforce some of the concerns we have around supply bottlenecks," Knot said Tuesday in a Bloomberg TV interview with Francine Lacqua."I don't think myself that it will have an impact on our intention to wind down the pandemic emergency purchase program," Knot said. "After all, its dual objectives have already been accomplished."

FRANCE / COVID (BBG): French Prime Minister Jean Castex tested positive for Covid-19 as a new wave of coronavirus cases spreads across Europe. Castex will be isolating for 10 days, his office said in a statement. Although France has not put new restrictions in place like Austria and Germany, the latest wave is hitting the country "at a blazing speed," government spokesman Gabriel Attal said on Sunday. President Emmanuel Macron's government is reinforcing health-pass checks in enclosed areas and this week will discuss opening up its booster-shot campaign to more adults, he said.

ITALY (BBG): Italy needs to use any possible room for maneuver to accelerate the debt reduction process, Bank of Italy's head of the structural economic analysis directorate Fabrizio Balassone told lawmakers on Tuesday."Italy should identify intervention areas for a credible reduction of debt/GDP ratio, even beyond the three-year planning": Balassone.

DATA:

FRANCE DATA: Strong PMI data driven by services

Positive print for the French PMIs with services at 58.2 (55.5 exp, 56.6 prev), manufacturing at 54.6 (53.1 exp, 53.6 prev) and composite at 56.3 (53.9 exp, 54.7 prev). Strong output for services and employment in general and further cost pressures. Only a small market reaction as we expected to an upside print. Highlights from the Markit press release:

- "The fastest increase in services activity for almost four years"

- "In order to meet existing and expected demands on their businesses, private sector employment across France continued to increase in November. In line with the trend seen in recent months, jobs growth remained well above its historical average and was primarily led by service providers."

- "Elsewhere, steep rates of both output price and input cost inflation were once again recorded in November. Price pressures were particularly acute at manufacturers"

- "Selling charges were increased at the strongest rate since May 2011 during November as both manufacturers and service providers marked up their prices to stronger extents to protect their profit margins."

GERMAN DATA: Weaker details underpin strong PMI prints

Above-consensus prints for the German PMIs too, with services at 57.6 (56.9 exp, 57.8 prev), manufacturing at 53.4 (51.5 exp, 52.4 prev) and composite at 52.8 (51.0 exp, 52.0 prev). However, other than employment, the details were much more subdued in terms of output and new orders but price pressures continued. Highlights from the press release:

- "Data pointed to unprecedented inflationary pressures, with firms linking the latest rises with ongoing supply issues and shortages."

- "The latest uplift in new work was the slowest for nine months as gains to demand were hindered by supply bottlenecks, input shortages and an associated decline in demand from the automotive sector"

- "November's flash data pointed to a stalling of new business at German service providers"

- "The rate of expansion in manufacturing new orders remained among the weakest since the recovery began in 2020, despite quickening since October to a solid rate"

- "The rate of [price] increase hit a survey record for the second month running as firms sought to maintain margins by passing greater costs through to clients where possible."

- "German companies continued to take on additional staff in November, extending the current sequence of higher employment which began in January. According to anecdotal evidence, firms were taking on staff to alleviate capacity pressures and in preparation for a strong rebound in the coming months."

EUROZONE DATA: PMI details mixed (1/2)

Higher than expected Eurozone PMI print, too, but again the details mixed with employment higher than expected, price pressures elevated but output expectations at their weakest since January.

- Note that data were collected 10-19 November (and responses are normally front-loaded). So these output expectations were before the worst of the lockdown news and before the Austrian lockdown was announced.

- However, this is still enough for EURUSD to be on the front foot today with the Euribor strip and Bunds under pressure.

- From the press release:

- Employment: "Although the rate of job creation rose to the second-highest in over 21 years as firms sought to meet rising demand, optimism about the outlook sank to a ten-month low on renewed COVID-19 worries and lingering supply constraints."

EUROZONE DATA: PMI details mixed (2/2)

- Output:

- Services saw "the strongest growth of activity for three months. Growth also picked up in manufacturing, though remained the second-weakest seen over the past 17 months"

- "The rest of the region as a whole meanwhile enjoyed faster growth of both manufacturing and services than seen in France and Germany."

- "Future output expectations deteriorated to the lowest since January. Ongoing concerns over supply chain issues were exacerbated by growing worries about the impact of further COVID-19 waves, which darkened the outlook for services in particular."

- Prices:

- "Shortages were meanwhile once again seen as a principal driver of higher prices for many goods and services, alongside higher shipping costs, rising energy prices and increases in staff costs. November consequently saw a survey record increase in firms' input costs for a second successive month."

- "Selling price inflation likewise accelerated in both manufacturing and services to the fastest in almost two decades of comparable survey history as firms sought to pass higher costs on to customers, most notably in Germany."

UK DATA: Strong PMI details as output and consumer demand remain solid

PMI data a little better than expected for services and composite and almost a point better than expected for manufacturing. Looking through the report there are strong details in here with output and consumer demand looking good.

- Market reaction rather subdued given only a small upward surprise to the data.

- Highlights from the press release:

- Input prices at highest pace of increase since January 1998 "driven by higher wages and a spike in prices paid for fuel, energy and raw materials"

- "Exceptionally strong cost pressures meant that prices charged by manufacturers increased at the steepest rate since the index began 20 years ago. However, service providers indicated a slight slowdown in output charge inflation to its lowest for three months, with some citing greater resistance to higher selling prices among clients."

- "Customer demand continued to rise sharply in November, despite the pass through of higher costs to clients, with the overall rate of new order growth accelerating to a five-month high."

- "Service providers reported a faster recovery in new work than goods producers. Subdued momentum in the manufacturing sector again reflected constraints on growth due to the global supply chain crisis. "

- "Strong customer demand and increased backlogs of work contributed to another marked rise in private sector employment during November. Staffing numbers have now picked up in each of the past nine months, although the latest increase was the slowest since April. Survey respondents widely noted that recruitment difficulties and unexpected staff departures for higher wages or lifestyle changes had constrained employment growth."

FIXED INCOME: PMIs the driver this morning with big moves in Bunds

There have been some big moves in Bunds this morning following the stronger-than-expected German, French and Eurozone PMI prints. However, we would caution that some of the moves look a little excessive - there are clear inflationary pressures, but the underlying details outside of prices and employment look rather weak. The UK PMI in contrast saw less of a headline surprise but was more positive in the underlying details.

- The bear steepening of the Bund curve has seen 2s5s steepen 2.4bp and 2s10s steepen 3.4bp on the day. The gilt curve has seen more of a parallel 1.6bp shift with yieldds higher while the UST curve has steepened most in the 2s7s area (1.5bp steeper on the day).

- TY1 futures are down -0-3+ today at 129-28+ with 10y UST yields up 0.8bp at 1.633% and 2y yields down -0.6bp at 0.627%.

- Bund futures are down -0.63 today at 171.14 with 10y Bund yields up 4.3bp at -0.260% and Schatz yields up 0.3bp at -0.834%.

- Gilt futures are down -0.17 today at 126.12 with 10y yields up 1.5bp at 0.947% and 2y yields up 1.4bp at 0.535%.

FOREX: EUR Off the Mat as PMIs Improve

- The single currency is among the session's best performers so far Tuesday, with the EUR improving on the back of a set of better-than-expected PMI numbers across the continent. Prelim data showed growth was higher than expected across both manufacturing and services sector in France and Germany.

- This puts EUR/USD back above 1.1250 ahead of the NY crossover and thereby off the new YTD lows printed in early Asia-Pac hours at 1.1226. There's little evidence of a sustained bounce at present levels, with markets needing to top 1.1307 before indicating any further recovery.

- Elsewhere, markets are more mixed, with CAD, NZD and NOK among the session's worst performers as commodity markets trade more subdued. WTI and Brent crude futures are off over 1.5% on the day, possibly in anticipation of a coordinated release of oil reserves from some of the world's largest consumers at some point today.

- US prelim PMI takes focus going forward, with both the manufacturing and services sector seen improving from the October read. Both sectors are seen growing at a decent clip, with the data seen holding just below 60.0. The speaker slate picks up, with BoE's Bailey, Cunliffe and Haskel all due as well as BoC's Beaudry and ECB's de Guindos.

- Lastly, President Biden speaks directly on the US economy and inflation at 1400ET / 1900GMT.

EQUITIES: Tech Leads Overnight Weakness

- Asian stocks closed mixed (Japan is closed for holidays), with China's SHANGHAI closed up 7.009 pts or +0.2% at 3589.089 and the HANG SENG ended 299.76 pts lower or -1.2% at 24651.58.

- European equities are sharply lower, with the German Dax down 169.32 pts or -1.05% at 15936.54, FTSE 100 down 28.22 pts or -0.39% at 7229.53, CAC 40 down 62.32 pts or -0.88% at 7049.04 and Euro Stoxx 50 down 42.84 pts or -0.99% at 4291.75.

- U.S. futures are a little weaker overnight, with the Dow Jones mini down 3 pts or -0.01% at 35568, S&P 500 mini down 3.5 pts or -0.07% at 4676.25, NASDAQ mini down 46.25 pts or -0.28% at 16336.

COMMODITIES: Gas Jumps, Oil Drops, Precious Metals Weaken

- WTI Crude down $1.12 or -1.46% at $75.67

- Natural Gas up $0.21 or +4.32% at $4.984

- Gold spot down $6.81 or -0.38% at $1797.43

- Copper up $2.75 or +0.63% at $442.3

- Silver down $0.25 or -1.02% at $23.9146

- Platinum down $6.42 or -0.63% at $1007.11

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.