Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- SWISS NATIONAL BANK REPEATS WILLINGNESS TO INTERVENE IN FX

- NORGES BANK SIGNALS FIRST HIKE IN H1 2022

- FRANCE'S MACRON TESTS POSITIVE FOR COVID; P.M. CASTEX TO SELF-ISOLATE

- U.K.'S GOVE CONFIRMS COMMONS RECALL IF BREXIT DEAL ON THE TABLE

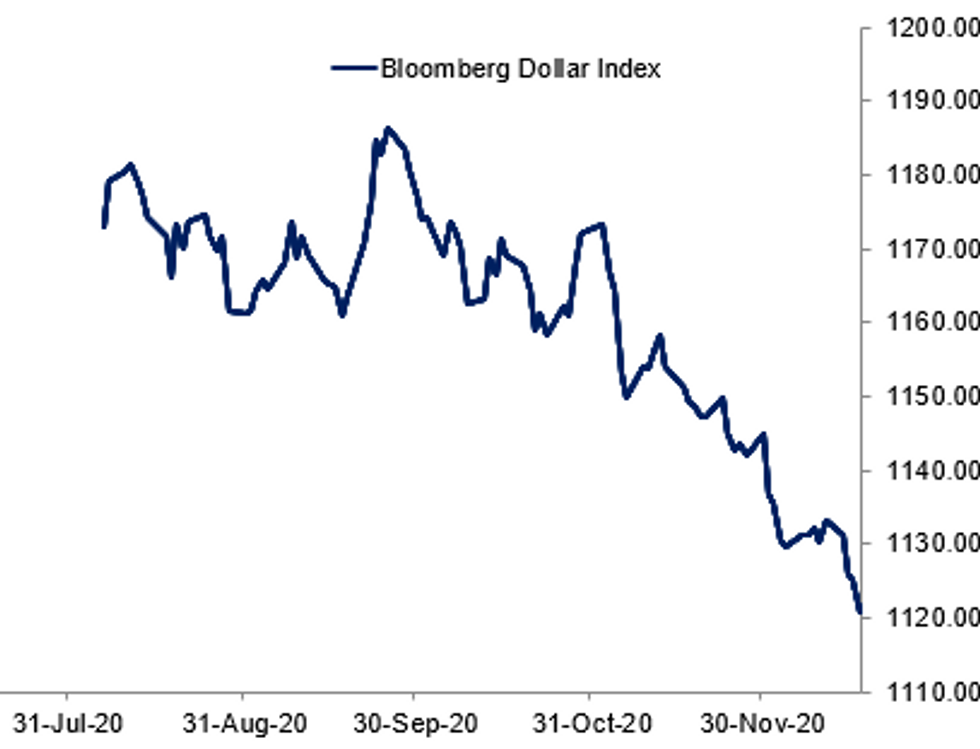

Fig. 1: Dollar Continues To Slide

NORGES BANK (MNI REVIEW): Norges Bank left its policy rate unchanged at zero percent and signalled that it was expecting to hike in the first half of 2022. The board's collective rate path, the key item in its Monetary Policy Report, showed the policy rate rising to 0.3% in 2022 and 0.8% in 2023, compared to 0.2% and 0.3% respectively in the previous MPR. Governor Oysten Olsen restated the guidance that the policy rate would stay on hold until "there are clear signs that economic conditions are normalising." The decision was in line with expectations and the MNI Preview.

FRANCE: President of the Senate Gerald Larcher confirms that Prime Minister Jean Castex will go into a period of self-isolation and will not attend the chamber following the confirmation that President Emmanuel Macron has tested positive for COVID-19. Elysee Palace has confirmed that Macron will continue to work during hisself-isolation period via videolink. Macron was tested after showing mild symptoms of the virus.

FRANCE-E.U.: The schedule of French President Emmanuel Macron shows that he has held in-person meetings with both Spanish Prime Minister Pedro Sanchez and Portuguese Prime Minister Antonio Costa this week.

U.K.-E.U.: Chancellor of the Duchy of Lancaster and Minister for Cabinet Office Michael Gove answering questions in the Commons on Brexit, jumps the gun ahead of statement from Leader of the House, saying that the gov't will recall parliament if a Brexit deal is reached during the recess (which starts at close of business tonight).Gove also stated that he believes any relevant legislation can be passed byyear-end.

U.K.-E.U.: EU chief negotiator Michel Barnier tweets: "In this final stretch of talks, transparency & unity are important as ever: Debriefed @Europarl_EN Conference of Presidents this morning on EU-UK negotiations. Good progress, but last stumbling blocks remain. We will only sign a deal protecting EU interests & principles."

CHINA-AUSTRALIA: Beijing will handle Australia's decision to act against China through the World Trade Organization over anti-dumping and anti-subsidy duties on imported Australian barley through the proper dispute settlement procedures, said Gao Feng, spokesman of the Ministry of Commerce at a briefing on Thursday, adding regret at Canberra's decision to take action.

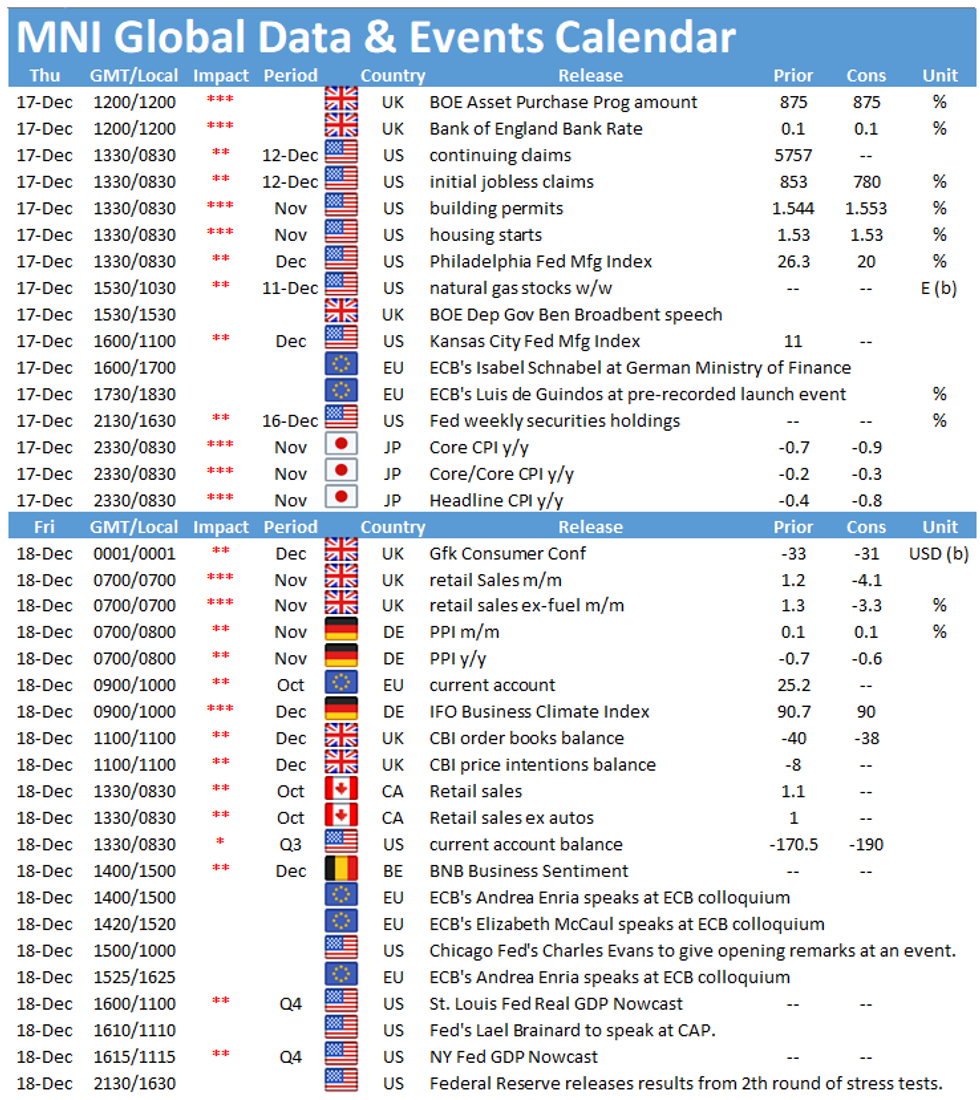

DATA:

FIXED INCOME: Focus on the Bank of England

It's been a day of divergence with Bunds outperforming, gilts a little higher and Treasury futures close to flat on the day. There doesn't seem to be too much behind the moves at present.

- The main highlight for fixed income markets today will be the Bank of England MPC policy decision and Summary. We expect little in terms of new policies with the real focus on aspects of QE. There is an almost unanimous expectation in the market that the Bank will leave the pace of purchases unchanged when it resumes after the Christmas break, but there are question marks over how strongly the Bank will telegraph that the pace could increase in the event of a no deal Brexit. The Bank also confirmed at its last meeting that it was looking at the technicalities of QE and we expect the short bucket to be modified from 3-7 years by reducing the minimum maturity of gilts eligibly for purchase by the Bank.

- Elsewhere, Brexit talks continue while French President Macron has tested positive for Covid-19. Earlier this week he met both the Spanish and Portuguese prime ministers face to face.

- In terms of data today we have US jobless claims data and housing data as well as speeches from the ECB's Schnabel and de Guindos.

- TY1 futures are down -0-0+ today at 137-28 with 10y UST yields up 0.6bp at 0.924% and 2y yields down -0.2bp at 0.116%.

- Bund futures are up 0.20 today at 177.75 with 10y Bund yields down -1.3bp at -0.581% and Schatz yields down -0.3bp at -0.737%.

- Gilt futures are up 0.10 today at 134.63 with 10y yields down -0.1bp at 0.270% and 2y yields down -0.1bp at -0.85%.

FOREX SUMMARY

A busy FX sessio, with plenty of early CB decisions.

- USD inderperforms once again, with better buying interest in Equities.

- Bank Indonesia left their reverse repo rate unchanged as expected at 3.75%

- BSP also left their rate unchanged at 2%, as expected.

- SNB were next on the heavy CB calendar, and have also left their Rate unchanged at -0.75%.

- Norway left their rates unchanged but moved forward the rate hike path.

- As such, NOK continued to extend gains, versus the USD. Highest since 2019Rate path brought forward, and broader USD weakness as well as higher Oil on the decline in US stockpile are all benefiting the NOK.

- USDNOK is 8.5887 at the time of typing

- AUD is the second best performing currency against the Greenback, up 0.75% and tested resistance at 0.7638 38.2% retracement of the 2013-2020 downtrend (printed 0.7640 high)

- GBP stays on the front foot, with market participants positioning for a Brexit deal.

- Talks here continues, with progress progress noted, but same sticking points remains (no change)

- Looking ahead, all eyes on the BoE, and on the data front, USD IJC, and speakers sees ECB Guindos and Schnabel

EQUITIES: Bullish Start

Generally positive risk appetite has equities on the front foot to start Thursday. Tech and Utilities outperforming in Europe, with financials and Energy lagging.

- Asian stocks closed higher, with Japan's NIKKEI up 49.27 pts or +0.18% at 26806.67 and the TOPIX up 5.75 pts or +0.32% at 1792.58. China's SHANGHAI closed up 37.89 pts or +1.13% at 3404.873 and the HANG SENG ended 218.09 pts higher or +0.82% at 26678.38.

- European equities are mostly higher, with the German Dax up 96.61 pts or +0.71% at 13706.31, FTSE 100 down 0.24 pts or 0% at 6589.5, CAC 40 up 18.69 pts or +0.34% at 5572.23 and Euro Stoxx 50 up 17.14 pts or +0.48% at 3568.03.

- U.S. futures are higher, with the Dow Jones mini up 130 pts or +0.43% at 30291, S&P 500 mini up 20.25 pts or +0.55% at 3721, NASDAQ mini up 63 pts or +0.5% at 12728.25.

COMMODITIES: Precious Metals, Oil Higher As Dollar Weakens

- WTI Crude up $0.44 or +0.92% at $48.32

- Natural Gas up $0 or +0.04% at $2.689

- Gold spot up $13.07 or +0.7% at $1880.06

- Copper up $3.45 or +0.97% at $359.95

- Silver up $0.38 or +1.51% at $25.7536

- Platinum up $17.54 or +1.69% at $1052.68

LOOK AHEAD:

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.