EXECUTIVE SUMMARY:

- WHILE JUNE CUT MAY BE APPROPRIATE, JULY NOT WARRANTED - SCHNABEL

- WTO WOULD BE FIRST STEP FOR CHINA IN US TARIFF RESPONSE

- BOJ WANTS STABLE FX MARKET TO CUT JGB BUYING

- PBOC TO PROVIDE $42BLN FUNDS FOR STATE HOUSE PURCHASES

NEWS

ECB (MNI): ECB June Cut 'May Be Appropriate', Not July - Schnabel

Although not pushing back on the likelihood of a June rate cut, ECB executive Board member Isabel Schnabel tells Japan's Nikkei that the prospects of a back-to-back cut in July "does not seem warranted" on current data. Schnabel says she still sees inflation risks tilted to the upside and that a "front-loading of the easing process would come with a risk of easing prematurely".

EUROPE (BBG): Europe’s Economy Needs to Grow More Quickly, Donohoe Says

Europe’s economy needs see faster growth, Eurogroup President Paschal Donohoe said Friday.“As we get inflation down, I want to see the euro-area and Europe grow quicker,” he told Bloomberg Television on Friday. “I believe we can do it but we need to take further steps to make that happen”.

GLOBAL (MNI): WTO First Step For China In US Tariff Response - Advisors

China is likely to file a WTO dispute against the U.S. over its move to hike tariffs on Chinese new energy products instead of tit-for-tat retaliation, policy advisors told MNI. The economic impact of many of the measures announced by U.S. President Joe Biden on May 14, including a 100% tariff on Chinese electric vehicles will be limited in the short term, noted He Weiwen, a former economic and commercial counsellor at the Chinese Consulate General in San Francisco and New York. But, He added, whoever wins the next U.S. presidential election could escalate, potentially imposing import restrictions on new energy products using more than a fixed proportion of Chinese parts.

RUSSIA/UKRAINE (BBG): Ukraine Races to Halt One of Russia’s Biggest War Pushes So Far

Russia’s weeklong offensive in northeastern Ukraine is setting alarm bells ringing in Kyiv as President Volodymyr Zelenskiy and his generals rush to shore up their defenses. Zelenskiy has canceled foreign travel plans for the next few days and on Thursday met with his key commanders in Kharkiv, the border city that’s become the focus of Moscow’s attacks.

JAPAN (MNI): BOJ Wants Stable FX Market To Cut JGB Buying

The Bank of Japan is concerned the market could interpret any reduction to its Japanese government bond buying programme as an attempt to curb yen weakness and a sign of earlier-than-expected rate hikes, and will hold off plans to shrink its purchases until stability returns to the foreign-exchange market, MNI understands.

CHINA (BBG): PBOC to Provide $42 Billion for State Purchases of Unsold Homes

The People’s Bank of China will establish a nationwide program to unleash 300 billion yuan ($41.5 billion) in cheap funding to help state-owned companies buy unsold homes, officials announced. China’s central bank Deputy Governor Tao Ling said the “relending” funds would be extended to 21 providers, including policy banks, state-owned commercial lenders and joint-stock banks, at a rate of 1.75%.

CHINA (MNI): PBOC Abolishes Lower Housing Mortgage Limit

The People’s Bank of China eliminated the nationwide policy floor for the interest rates on commercial mortgage loans for first-time and second-time home buyers, its latest effort to curb the real-estate downturn. Local authorities were given the autonomy to determine whether to set the lower limit of housing mortgages, according to a statement on the PBOC website on Friday.

CHINA (MNI): China To Acquire Housing, Land Stocks From Developers

Local governments can purchase some of the unsold commercial housing at reasonable prices to use as affordable housing, especially in cities with large inventory, said Vice Premier He Lifeng during a video conference on Friday, according to the state run Xinhua News Agency. Local governments should also take over or acquire idle residential lands from real-estate developers to help them overcome financial difficulties, He was cited as saying.

CHINA (MNI): China April Data Shows Insufficient Demand - NBS

China's April data showed domestic demand remains insufficient, while overall economic operations were stable and continuing the upward recovery, Liu Aihua, spokesperson for the National Bureau of Statistics said on Friday. When questioned on the impact of U.S. tariffs, Liu said the national economy's strong resilience was conducive to resolving external shocks.

MNI PBOC WATCH: May LPR To Remain Steady As Market Rates Fall

China’s reference lending rate is likely to remain unchanged in May as the central bank aims to steady the policy environment following the fall in market rates and as it pursues its mission to curb idle funds inside the financial system.

MNI RBNZ WATCH: MPC To Hold, Maintain OCR Path Ahead

The Reserve Bank of New Zealand's Monetary Policy Committee is likely to hold the Official Cash Rate at 5.5% when it meets on May 22, and to maintain its outlook for cuts by the second half of 2025, as domestic and core inflation continue to prove resilient and despite a weakening labour market.

DATA

**CHINA APR RETAIL SALES +2.3% Y/Y VS MEDIAN +3.8% Y/Y - MNI

JAN-APR RETAIL SALES +4.1% Y/Y VS JAN-MAR +4.7% Y/Y

APR INDUSTRIAL OUTPUT +6.7% Y/Y VS MEDIAN +5.4% Y/Y: NBS

JAN-APR INDUSTRIAL OUTPUT +6.3% Y/Y VS JAN-MAR +6.1% Y/Y

YTD PROPERTY INVESTMENT -9.8% Y/Y VS JAN-MAR -9.5% Y/Y

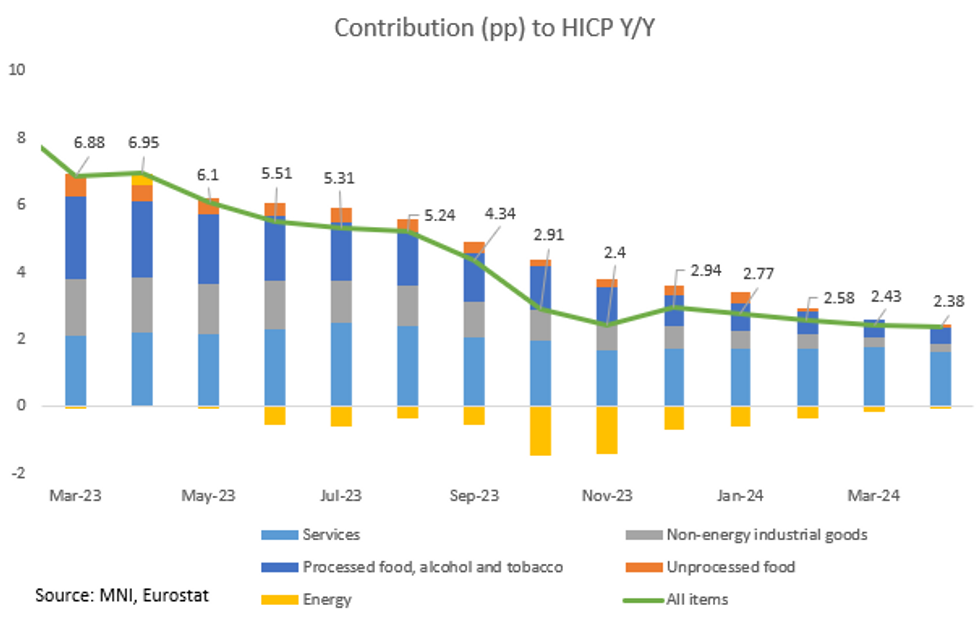

EUROZONE: Final Data Confirms Broad Deceleration Seen In April Flash HICP

Eurozone Final HICP confirmed the April flash prints, at +2.4% Y/Y (vs +2.4% in March) and +0.6% M/M (vs +0.8% in March). Energy continued to see Y/Y deflation for the twelfth consecutive month, whilst Processed food, alcohol & tobacco, non-energy industrial goods (NEIG, or core goods) and Services disinflated Y/Y.

- Core inflation on an annual basis printed in line with with flash at +2.7% Y/Y (vs +2.9% in March), and on a monthly basis it slowed to +0.7% M/M from+1.1% in March.

- At a country level, Estonia saw a revision from flash HICP Y/Y down 0.2pp, Italy and Cyprus saw a -0.1pp revision, whilst Malta saw HICP revised up +0.1pp.

- The final readings show the contribution from services inflation fell to the lowest since August 2022, after stalling for the last few months, contributing +1.64pp, although it remains the largest contributor to HICP overall.

- Meanwhile, the contribution from Processed food, alcohol and tobacco fell for the thirteenth successive month to +0.49pp (vs +0.55pp prior) - the lowest since December 2021. Similarly, NEIG's contribution fell again for the fourteenth consecutive month to +0.23pp (vs +0.3pp prior).

- Energy's negative contribution continues to fade as base effects continue to drop out of the Y/Y comparison, resulting in a contribution of -0.04pp in April (vs -0.16pp in March).

- To note, Unprocessed foods contribution increased slightly to +0.06ppt from -0.02ppt in March maintaining similar levels to February 2024.

- Later today, the ECB releases calculations of key underlying inflation metrics based on the final data, which will form part of the Governing Council's decision-making process as it assesses price pressures going into the June meeting.

FOREX: Greenback Follows Yields Higher as Markets in Bounceback Mode

- The greenback trades firmer against all others in the final trading day of the week, gaining on the back of an extension of the recovery in US Treasury yields. The US 10y yield is now north of yesterday's high, and retracing a large part of the post-CPI move lower.

- As a result, most major pairs are lower, with EUR/USD back below the 1.0850 mark and close to daily lows ahead of the NY crossover. ECB speak has largely stuck to the recent comms strategy, flagging June as the likely first cut, but a less certain outlook beyond the first easing step.

- Eurozone final CPI data confirmed the broad deceleration seen in the April flash release. Chinese industrial production and retail sales data came in mixed, with IP topping expectations, but retail sales coming up short. The challenges facing the Chinese economy remain a focus for policymakers, with PBOC's Tao on the wires this morning to shed more light on four separate housing market policies - but the headlines failed to trigger any broad risk rally. AUD remains among the poorest performers in G10.

- Data releases are few and far between Friday, leaving focus on central bank communications. ECB's Vasle, Holzmann & Kazaks are still set to speak, as well as Fed's Waller, Kashkari and Daly.

EGBS: Under Pressure Following Overnight Schnabel Remarks

Core/semi-core EGBs continue to exhibit weakness, with Bunds now below their pre-US-CPI/retail sales levels from Wednesday.

- Overnight, ECB Executive Board member Schnabel told Nikkei that a July rate cut was unlikely based on current data, which appears to have weighed on the EGB space this morning.

- While this view is consistent with market pricing (OIS price just 6bps of sequential cuts through the July meeting), it is one of the few times in recent weeks where a July cut has been explicitly noted as unlikely by ECB speakers.

- Eurozone final HICP confirmed flash estimates at 2.4% Y/Y, though more interest will lie in the ECB’s underlying inflation metrics, due for release later today.

- Bunds are -52 ticks at 131.06, while the German and French cash curves have bear steepened. 10-year periphery spreads to Bunds are little changed.

- With no other notable data scheduled for today, focus will rest on scheduled ECB (Vasle, Holzmann and Kazaks) and Fed speakers this afternoon.

EQUITIES: S&P Extends Bull Cycle

S&P E-Minis have traded higher this week as the contract extends the bull cycle from Apr 19. Bullish trend conditions remain intact. Recent gains have resulted in a break of key resistance at 5333.50, Apr 1 high. This confirms a resumption of the primary uptrend and signals scope for a climb to 5372.73. Eurostoxx 50 futures maintain a bullish tone despite yesterday’s pullback. This week’s gains resulted in a break of key resistance at 5079.00, the Apr 2 high, to confirm a resumption of the uptrend and maintain the price sequence of higher highs and higher lows.

- Japan's NIKKEI closed lower by 132.88 pts or -0.34% at 38787.38 and the TOPIX ended 8.08 pts higher or +0.3% at 2745.62.

- Elsewhere, in China the SHANGHAI closed higher by 31.625 pts or +1.01% at 3154.026 and the HANG SENG ended 177.08 pts higher or +0.91% at 19553.61.

- Across Europe, Germany's DAX trades lower by 56.99 pts or -0.3% at 18681.94, FTSE 100 lower by 23.92 pts or -0.28% at 8414.73, CAC 40 down 33.82 pts or -0.41% at 8156.64 and Euro Stoxx 50 down 17.35 pts or -0.34% at 5055.75.

- Dow Jones mini down 24 pts or -0.06% at 39988, S&P 500 mini down 1.5 pts or -0.03% at 5318.75, NASDAQ mini down 0 pts or 0% at 18648.

COMMODITIES: Bearish Oil Theme Persists

The medium-term trend structure in Gold is unchanged and remains bullish. This is reinforced by moving average studies that are in a bull-mode position. Near-term, a continued push higher would refocus attention on $2431.50, the Apr 12 high and bull trigger. A bearish theme in WTI futures remains intact and the current consolidation phase appears to be a pause in the trend. Price has recently breached the 50-day EMA, strengthening a short-term bearish set-up that highlights potential for a deeper correction.

- WTI Crude down $0.05 or -0.06% at $79.19

- Natural Gas up $0.02 or +0.8% at $2.514

- Gold spot up $5.13 or +0.22% at $2382.63

- Copper up $5.75 or +1.18% at $493.95

- Silver up $0.07 or +0.25% at $29.6572

- Platinum down $3.57 or -0.34% at $1059.53

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/05/2024 | 1230/0830 | * |  | CA | International Canadian Transaction in Securities |

| 17/05/2024 | 1415/1015 |  | US | Fed Governor Christopher Waller | |

| 17/05/2024 | 1700/1300 | ** | | US | Baker Hughes Rig Count Overview - Weekly |

| 18/05/2024 | 2145/1745 | | US | Fed Governor Adriana Kugler | |

| 19/05/2024 | 1930/1530 | | US | Fed Chair Jerome Powell | |

| 20/05/2024 | 0600/0800 | ** |  | DE | PPI |

| 20/05/2024 | 0900/1000 |  | UK | BOE's Broadbent Monetary Mechanism Workshop | |

| 20/05/2024 | - | | UK | DMO to hold quarterly consultation investors / GEMM consultation | |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 26 Week Bill |

| 20/05/2024 | 1530/1130 | * | | US | US Treasury Auction Result for 13 Week Bill |