US DATA

Personal income and spending growth was mixed versus expectations in June, though spending especially remained relatively solid overall in 2Q when considering upward revisions to prior months.

- Personal income grew by 0.2% M/M, below the 0.4% expected and with downward revisions to the prior two months (May 0.4% and April 0.2%, each revised down 0.1pp). Disposable personal income (personal income less personal current taxes) growth figures were identical to those.

- Personal spending growth came in line with expectations at 0.3% M/M, though this marked a better-than-foreseen result given an upwardly revised May (0.4% rev from 0.2%) and April (0.2% from 0.1%).

- The combination of these changes and slight upward PCE inflation revisions to prior left real disposable personal income growth at 0.1% in June, vs 0.3% in May (down rev from 0.5%) and -0.1% in April (down rev from 0.0%), and real PCE expenditure growth at 0.2% vs 0.4% M/M in May (rev from 0.3%) and -0.1% in Apr (unrev).

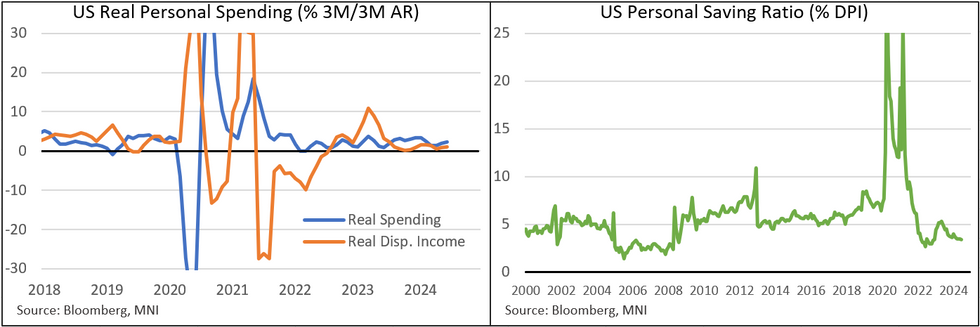

- The 0.2% real personal expenditure growth comprised a 0.2% rise in each of goods and services. This was a 4-month high (unrounded) for services spending, though goods pulled back sharply from +0.9% prior.

- The more-solid-than-expected real consumption figures were presaged by the prior day's release of a 2.3% Q/Q ann. real PCE growth figure in the first reading of Q2 national accounts (2.0% had been expected), which contributed the lion's share of GDP growth. Real consumption has thus improved in Q2 from 1.5% in Q1, though is cooler than the the 3.2% average in 2H23.

- Activity in the report can best be described as "moderate", but we note some slowly building cracks in the consumer story as the soft real income growth above suggests:

- The personal saving rate of 3.4% was down from 3.5% in each of the prior 3 months (May was downwardly revised from what had been a 4-month high 3.9%) and the lowest since December 2022. Total income growth is now running at 4.1% 3M/3M annualized, the slowest since January, with wages and salaries softening.

342 words