Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EXECUTIVE SUMMARY:

- ECB'S SIMKUS SAYS NEW TOOL MAY NEVER BE USED (MNI INTERVIEW)

- SPAIN INFLATION SOARS IN JUNE; STATE DATA POINTS TO SOFT GERMAN READING

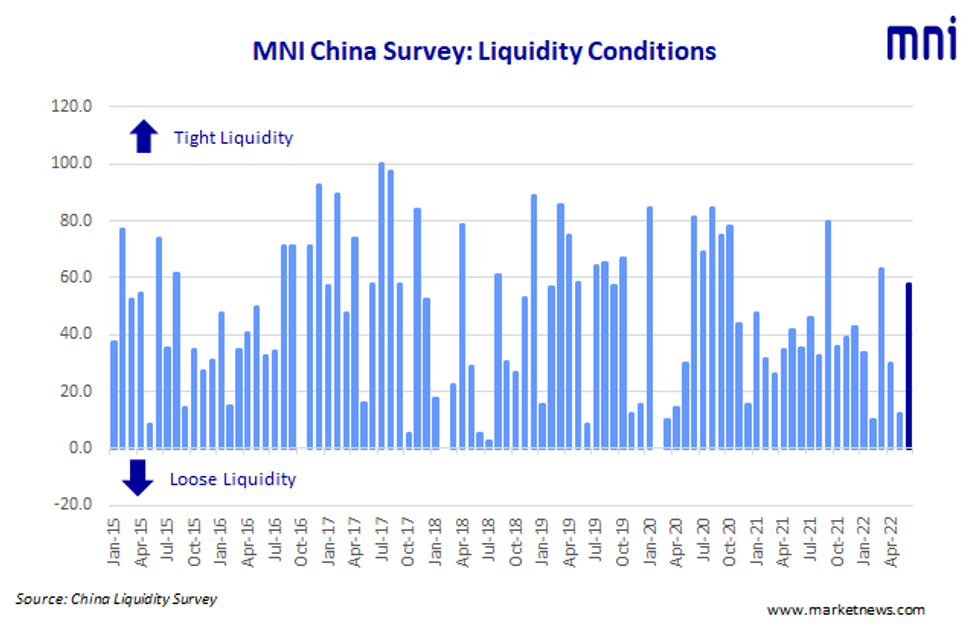

- MNI CHINA LIQUIDITY INDEX: LIQUIDITY TIGHTER; ECONOMY RECOVERS

- FED'S MESTER BACKS 75BP JULY HIKE IF CONDITIONS REMAIN SAME

- "AMPLE ROOM" TO HIKE IN 25BP OR 50BP STEPS AFTER SEPT: ECB HOLZMANN

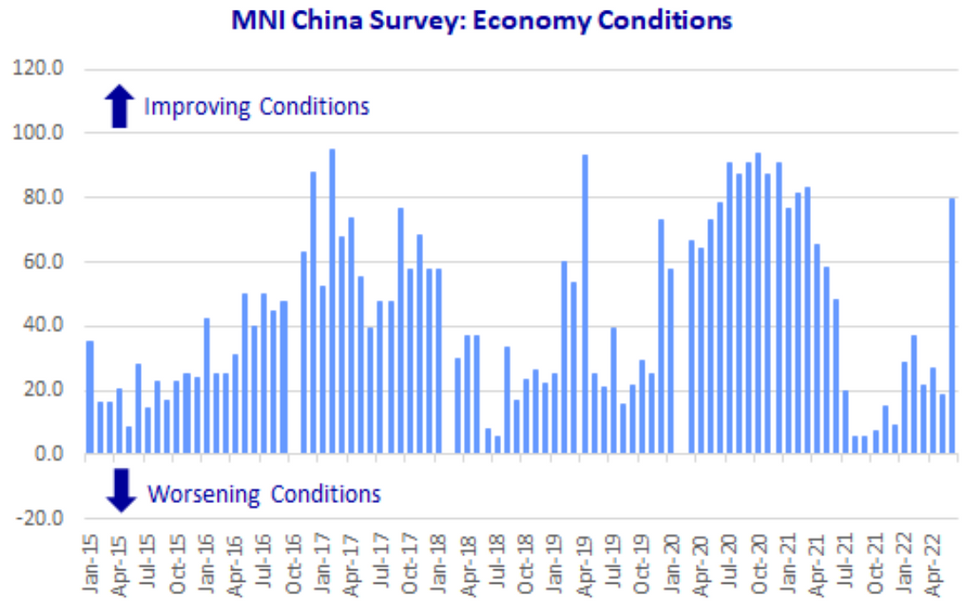

Fig. 1: China Econ Conditions Improving, Per MNI China Liquidity Survey

Source: MNI China Liquidity Survey

Source: MNI China Liquidity Survey

NEWS:

ECB (MNI INTERVIEW): The European Central Bank should raise key interest rates by at least 50 basis points in September and possibly by the same amount in July, Bank of Lithuania Chairman Gediminas Simkus told MNI, adding that he hoped a proposed new tool aimed at capping yield spreads within the eurozone may never be used.

FED (CNBC): Federal Reserve Bank of Cleveland President Loretta Mester said Wednesday that if economic conditions remain the same when the U.S. central bank meets to decide its next monetary policy move in July, she will be advocating for a 75 basis point hike to interest rates. “If conditions were exactly the way they were today going into that meeting — if the meeting were today — I would be advocating for 75 because I haven’t seen the kind of numbers on the inflation side that I need to see in order to think that we can go back to a 50 increase,” she told CNBC’s Annette Weisbach.

ECB (CNBC): A member of the European Central Bank told CNBC Wednesday that there’s plenty of runway to hike interest rates, following the two planned raises for July and September. “We will have to make an assessment where the economic development is going and where inflation stands and afterwards there’s ample room to hike in 0.25 and 0.5 levels to whatever rate we think, we consider reasonable,” Robert Holzmann, who’s also the governor of the Austrian central bank, told CNBC about the period after September.

GERMANY / FISCAL (BBG): Germany will bring its finances back in line with constitutional debt limits after three years of extraordinary spending. Finance Minister Christian Lindner is targeting 17.2 billion euros ($18.1 billion) in additional borrowing in 2023, according to two senior government officials, who asked not to be identified in line with protocol. While that’s more than double an earlier projection of 7.5 billion euros, it marks a massive cut from this year and complies with a rule that caps new debt at 0.35% of gross domestic product for the first time since 2019, the officials said on Wednesday.

CHINA (MNI): China is expected to issue over CNY1 trillion of Special Treasury Bonds (SBTs) in the third quarter to fill a fiscal gap and to help meet economic and employment targets, policy advisors and market analysts said, calling on the central bank increase liquidity to accommodate the massive debt sale.

CHINA/ENERGY (BBG): China will offer subsidies to oil refiners and won’t raise domestic oil product prices if international crude oil price is higher than $130/barrel, the upper limit set by the government, according to a statementon the Ministry of Finance website.

DATA:

MNI China Liquidity Index™– Rises To 57.8 in June

China’s economy is recovering from the recent Covid-triggered downturn, with many survey indicators picking up and liquidity conditions tightened in the half-year end, the latest MNI Liquidity Conditions Index shows.

The Liquidity Condition Index, rose to 57.8 in June from 12.5 previously, the highest reading in three months. One-in-five traders saw conditions “tighter than last month” as the year’s 6-month mark approached.

The higher the index reading, the tighter liquidity appears to survey participants.

- The Economy Condition Index stood at 79.7, surging from May's 18.8, partly on Covid restrictions easing.

- The PBOC Policy Bias Index remained below 50 for a 12th consecutive month.

- The Guidance Clarity Index was little changed, as respondents again claim to understand the signals from the PBOC.

The MNI survey collected the opinions of 32 traders with financial institutions operating in China's interbank market, the country's main platform for trading fixed income and currency instruments, and the main funding source for financial institutions.

Interviews were conducted June 13 – June 20.

Click below for the full press release:

MNI China Liquidity Index -2022-06 presser.pdf

For full database history and full report on the MNI China Liquidity Index™, please contact:sales@marketnews.com

Downside Risks to German CPI Following State Prints

- The German regional CPI readings for June saw 0.2-0.6pp decelerations across the board.

- The state readings published this morning account for 67.3% of the total June rate. Out state-weighted calculation of the German June CPI rate accounts for 67.3% of the total print and sees inflation at +7.6%, which would imply a 0.3pp slowdown from May.

- Our calculation expects substantial downside risks to the consensus forecast of inflation flatlining at +7.9% y/y in Germany's index, and the 0.1pp uptick anticipated for the harmonised print to +8.8% y/y. The release time is 1300 BST.

| June y/y | May y/y | Difference | Destatis Weighting | |

| North Rhine Westphalia | 7.5 | 8.1 | -0.6 | 21.7% |

| Hesse | 8.1 | 8.4 | -0.3 | 7.7% |

| Bavaria | 7.9 | 8.1 | -0.2 | 16.8% |

| Brandenburg | 8 | 8.5 | -0.5 | 2.6% |

| Baden Wuert. | 7.1 | 7.4 | -0.3 | 14.1% |

| Saxony | 7.7 | 8.0 | -0.3 | 4.4% |

| Total: 67.3% | ||||

| Weighted average: | +7.62% y/y | for | 67.3% of total CPI |

SPAIN DATA (BBG): Inflation Soars to 10%

Spanish inflation unexpectedly surged to a record, defying government efforts to rein it in and signaling intensifying price pressure as the European Central Bank gears up to raise interest rates for the first time in more than a decade. The surprise 10% reading for June dashes hopes that inflation in the euro zone’s fourth-biggest economy had peaked and highlights how a squeeze on consumers, once forecast to be transitory, is instead intensifying. The rate is up from 8.5% in May and exceeded all 15 estimates in a Bloomberg survey of economists.

Eurozone Economic Sentiment Softens Modestly in June

EUROZONE JUNE ECONOMIC SENTIMENT 104; MAY 105

- Economic sentiment dipped one point in June to 104, coming in slightly stronger than the two-point weakening expected. This is the lowest reading since March 2021, however, remains above levels seen for the majority of 2020.

- Economic sentiment in the EU saw a larger 1.7-point decrease to 102.5.

- The Netherlands saw the steepest decline (-3.6 points), followed by Germany and Spain (both -1.9 points).

- Confidence weakened across construction, consumer, retail and services sentiment. Industry remained largely stable, largely due to current orders remaining robust despite production expectations slumping to a 19-month low.

- Expected services demand dipped to a 14-month low, on the back of an anticipated drop-off in consumer demand, as households saw their future financial positions at a record low.

- The employment indicator also saw a notable -1.6-point decrease, on the back of deteriorating employment expectations in the upcoming months.

- On the inflation front, selling prices continued to climb to a fresh high in retail, whilst seeing some relief in industry and construction.

FIXED INCOME: Another fast markets start

- A busy start for EGBs and Bund, with futures taking their cue from some of the German regional CPI misses versus last.

- It's another 210 ticks range for the German 10yr, but are well off the sessions high, and actually drifting towards the session low at the time of typing.

- Some of the pullback has been attributed to the Spanish CPI big beat, coming at 10% vs median estimates of 8.7%, and likely some position squaring.

- Peripherals are all tighter, Greece by 4.2bps so far today.

- Gilts underperforms Bund, pushing the Gilt/Bund spread 1.2bp wider, but well within ranges.

- US Treasuries have also lagged Europe, but are nonetheless also in green territory, underpinned by the moves in Europe.

- Looking ahead, German National CPI, and out of the US sees third readings for GDP, so more focus on the US PCE.

- Still plenty of speakers are left, with ECB Schnabel, Lagarde, BoE Bailey, Swati, Fed Powell, Mester and Bullard.

- Sep Bund futures (RX) up 48 ticks at 145.66 (L: 145.27 / H: 147.37)

- Germany: The 2-Yr yield is down 3.5bps at 0.922%, 5-Yr is down 4.6bps at 1.387%, 10-Yr is down 2.5bps at 1.603%, and 30-Yr is down 2.1bps at 1.807%.

- Sep Gilt futures (G) up 10 ticks at 112.25 (L: 112.1 / H: 112.66)

- UK: The 2-Yr yield is down 3.3bps at 2.083%, 5-Yr is down 2bps at 2.122%, 10-Yr is down 1.1bps at 2.454%, and 30-Yr is up 1.2bps at 2.724%.

- Sep BTP futures (IK) up 83 ticks at 121.02 (L: 120.6 / H: 121.83)

- Sep OAT futures (OA) up 39 ticks at 136.29 (L: 135.94 / H: 137.57)

- Italian BTP spread down 4.4bps at 188.8bps

- Spanish bond spread down 1.9bps at 107.8bps

- Portuguese PGB spread down 2bps at 105.6bps

- Greek bond spread down 2.8bps at 223.3bps

- US 2-Yr yield is down 1bps at 3.0994%, 5-Yr is down 2.1bps at 3.2125%, 10-Yr is down 1.1bps at 3.1603%, and 30-Yr is down 0.5bps at 3.2736%.

- The Sep 22 T-Note future is up 11.5/32 at 117-20, having traded in a range of 116-270 to 117-125.

FOREX: EUR Reverses Overnight Dip on Double Digit Spanish CPI

- Spanish inflation prompted some early price action across European assets, with the EU harmonised reading lurching higher to 10.0% from 8.5% and another record high. The release prompted EUR/USD to erase the early losses to trade just above the 1.05 handle once more, but stopping short of the 1.0536 Asia session highs.

- In contrast, German state CPIs suggest a lower-than-expected reading later today, with states representing a majority weight of the national measure putting M/M at around 0.0-0.1%, well below the 0.4% M/M consensus. The earlier release of North Rhine Westphalia data had prompted some downside in the EUR, but the Spanish release reversed the bulk of the move.

- EUR/CHF is narrowing in on both parity and the YTD lows posted in March, with 0.9972 the key support going forward. CHF strength follows the continued baking-in of rate hike expectations at the SNB, with SARON markets indicating expectations of further 50bps rate rises at both the September and December policy meetings. This would put year-end rates at +0.75%.

- AUD/USD is extending the recent streak of underperformance, putting the pair lower for a third consecutive session and within range of key supports at 0.6869 and 0.6851.

- US GDP and PCE data out later today will likely fail to move the needle, with the tertiary reading expected unchanged across the board. Instead, focus will be on the ECB's Sintra policy forum, at which ECB's Lagarde, BoE's Bailey and Fed's Powell are all due to appear. Fed's Bullard and Mester also make separate appearances.

EQUITIES: Cyclical Stocks Leading Europe Lower

- Asian markets closed lower: Japan's NIKKEI closed down 244.87 pts or -0.91% at 26804.6 and the TOPIX ended 13.81 pts lower or -0.72% at 1893.57. China's SHANGHAI closed down 47.692 pts or -1.4% at 3361.518 and the HANG SENG ended 422.08 pts lower or -1.88% at 21996.89.

- European equities are also lower, following on from Tuesday's U.S. stock weakness. Cyclical stocks are dragging on the index, including industrials and tech, with the German Dax down 169.78 pts or -1.28% at 13302.72, FTSE 100 down 33.67 pts or -0.46% at 7359.99, CAC 40 down 41.59 pts or -0.68% at 6139.11 and Euro Stoxx 50 down 27.18 pts or -0.77% at 3567.32.

- U.S. futures are finding their feet, with the Dow Jones mini up 44 pts or +0.14% at 30977, S&P 500 mini up 4.25 pts or +0.11% at 3829.75, NASDAQ mini up 15.5 pts or +0.13% at 11689.75.

COMMODITIES: U.S. NatGas Gains Amid Broader Weakness

- WTI Crude down $0.11 or -0.1% at $111.22

- Natural Gas up $0.22 or +3.36% at $6.561

- Gold spot down $2.74 or -0.15% at $1822.13

- Copper down $1.9 or -0.5% at $377.25

- Silver down $0.01 or -0.03% at $20.9101

- Platinum up $16 or +1.75% at $916.85

LOOK AHEAD:

| Date | GMT/Local | Impact | Flag | Country | Event |

| 29/06/2022 | 1015/1215 |  | EU | ECB Schnabel on Inflation Expectations at ECB Forum | |

| 29/06/2022 | 1030/0630 |  | US | Cleveland Fed's Loretta Mester speaking at ECB forum | |

| 29/06/2022 | 1100/0700 | ** | | US | MBA Weekly Applications Index |

| 29/06/2022 | 1200/1400 | *** |  | DE | HICP (p) |

| 29/06/2022 | 1230/0830 | *** | | US | GDP (3rd) |

| 29/06/2022 | 1300/0900 | | US | Fed Chair Jerome Powell speaking at ECB forum | |

| 29/06/2022 | 1300/1500 | | EU | ECB Lagarde pm Monetary Policy Challenges | |

| 29/06/2022 | 1300/1400 |  | UK | BOE Bailey Panels ECB Forum | |

| 29/06/2022 | 1430/1030 | ** | | US | DOE weekly crude oil stocks |

| 29/06/2022 | 1500/1700 | | EU | ECB Lagarde Closing Remarks at ECB Forum | |

| 29/06/2022 | 1530/1130 | * | | US | US Treasury Auction Result for Cash Management Bill |

| 29/06/2022 | 1705/1305 | | US | St. Louis Fed's James Bullard | |

| 30/06/2022 | 0130/0930 | *** |  | CN | CFLP Manufacturing PMI |

| 30/06/2022 | 0130/0930 | ** | | CN | CFLP Non-Manufacturing PMI |

| 30/06/2022 | 0600/0700 | * | | UK | Quarterly current account balance |

| 30/06/2022 | 0600/0700 | *** | | UK | GDP Second Estimate |

| 30/06/2022 | 0630/0830 | ** |  | CH | retail sales |

| 30/06/2022 | 0645/0845 | *** |  | FR | HICP (p) |

| 30/06/2022 | 0645/0845 | ** | | FR | PPI |

| 30/06/2022 | 0645/0845 | ** | | FR | Consumer Spending |

| 30/06/2022 | 0700/0900 | * | | CH | KOF Economic Barometer |

| 30/06/2022 | 0730/0930 | ** |  | SE | Riksbank Interest Rate |

| 30/06/2022 | 0755/0955 | ** | | DE | Unemployment |

| 30/06/2022 | 0900/1100 | ** | | EU | Unemployment |

| 30/06/2022 | 1230/0830 | *** |  | CA | Gross Domestic Product by Industry |

| 30/06/2022 | 1230/0830 | ** | | US | Jobless Claims |

| 30/06/2022 | 1230/0830 | ** | | US | Personal Income and Consumption |

| 30/06/2022 | 1230/0830 | ** | | US | WASDE Weekly Import/Export |

| 30/06/2022 | 1330/1530 | | EU | ECB Lagarde Speech at Simone Veil Pact | |

| 30/06/2022 | 1345/0945 | ** | | US | MNI Chicago PMI |

| 30/06/2022 | 1430/1030 | ** | | US | Natural Gas Stocks |

| 30/06/2022 | 1530/1130 | * | | US | US Bill 08 Week Treasury Auction Result |

| 30/06/2022 | 1530/1130 | ** | | US | US Bill 04 Week Treasury Auction Result |

| 30/06/2022 | 1600/1200 | *** | | US | USDA Acreage - NASS |

| 30/06/2022 | 1600/1200 | ** | | US | USDA GrainStock - NASS |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.