Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

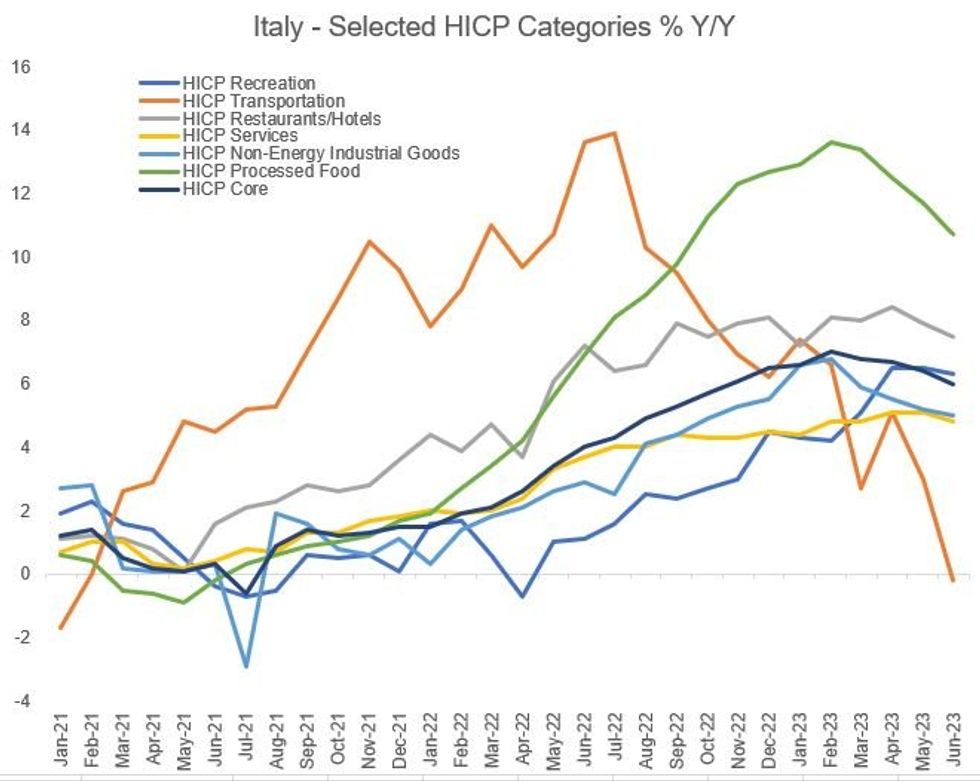

With the exception of communication (+0.5% after 0.4% in May), all of the major core categories were either steady or decelerated on a Y/Y basis.

- Recreation services (+6.3% vs 6.5% in each of the two months prior) and restaurants (+7.5% after 7.9%) also decelerated. They make up 22% of core inflation and that helped overall services HICP (47% of core) edge lower for the 2nd consecutive month at 4.8% vs 5.1% prior.

- Albeit there is still some stickiness here as Y/Y services remain well above 2022 levels which were <4%. And one would have to go back to 2012 to see readings consistently at 2% or above which is where services have printed 17 of the past 18 months.

- Transport, which is 15% of the total HICP basket, fell by 0.2% Y/Y vs 3.0% in May, marking the first negative Y/Y figure since January 2021. On a services basis alone in the CPI series, we saw a deceleration in transport to +3.8% from 5.6% prior.

- Non-energy industrial goods (35% of core) also decelerated but only modestly (to 5.0% from 5.2%).

- And while the broad grocery and unprocessed food category in CPI continued decelerating (10.7% Y/Y vs 11.2% prior), this belies an upward contribution from unprocessed foods (+9.8% in HICP vs 8.8% prior).

- On the latter, we note that some analysts had expected the recent flooding in Italy to impact on unprocessed food prices and that may have indeed been the case in June. Weather issues elsewhere including drought in Spain could come into play in this month's reading. That being said, while unprocessed food affects headline HICP, it is excluded from core.

Source: IStat, MNI

Source: IStat, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok