Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE

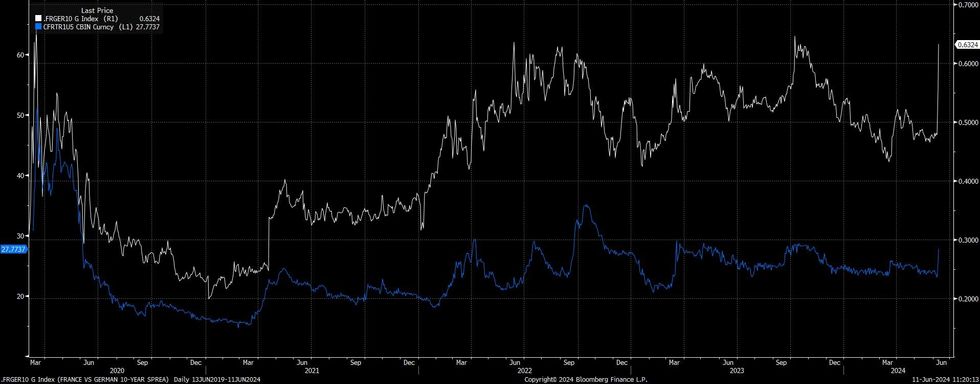

French CDS widening extends as speculation surrounding President Macron’s future picks up and OATs widen further.

- The Élysée has denied suggestions that Macron is considering his future.

- The benchmark French 5-Year CDS contract has moved to levels not seen since November, but still lags the degree of the relative move in OAT/Bund spreads.

- Movement in (the more liquid) 5-Year CDS measures covering the big French banks is more limited, with ’24 ranges comfortably intact. YtD highs are some distance away there.

- Note that the 10-Year PGB/Bund spread is now just ~3bp away from parity. Iberian/OAT spread tighteners have been a favoured sell-side play in recent times, owing to fiscal/ratings divergence.

- French fiscal worry remains evident at this juncture, while political paralysis in the case of an RN election victory and Macron staying on (known as “cohabitation”) could limit the ability to adjust fiscal spending.

- As a result, both Moody’s & Morningstar have issued notes of caution surrounding heightened political uncertainty.

- Furthermore, RN promises in previous election cycles included boosting fiscal spending, this will also be factoring into the move.

Fig. 1: 10-Year OAT/Bund Spread Vs. French 5-Year CDS

source: MNI - Market News/Bloomberg

source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok