Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

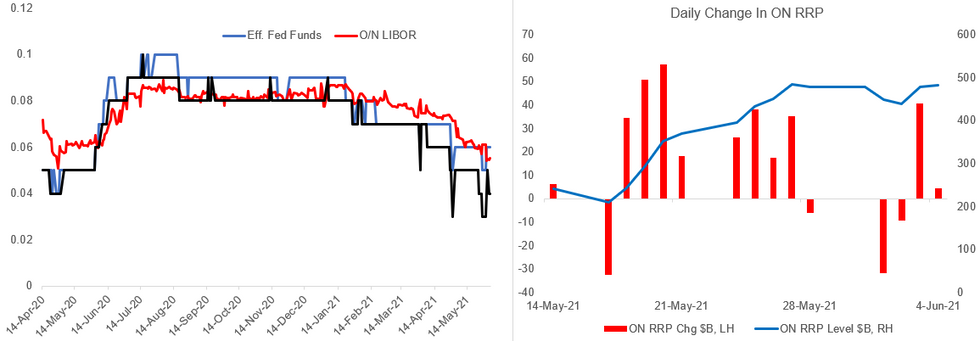

Overnight Reverse Repo takeup was only slightly higher in the week to Jun 2, with some 'cooling off' in usage of the facility following the Memorial Day holiday. Even so, the level of reserves fell slightly (-$3.4B), with the Treasury's account at the fed contracting by $29.2B for a 4-week net drop of $170.5B.

- But daily data shows ON RRP usage rising $40B on Thursday alone, the biggest jump since May 20, so the theme of continued growth amid burgeoning system reserves appears to remain intact.

- In a note Friday, Goldman wrote they expect RRP usage peaking around $1T (w reserves to $4.2T by year-end), but this amount is more conservative than the ~$1.2-1.3T one would assume if the almost one-to-one relationship between TGA drawdown/Fed assets and RRP growth continues. If net Tsy bill supply fails to ramp up, for instance, ON RRP may be end up more heavily used than Goldman has pencilled in.

Source: Federal Reserve, MNI

Source: Federal Reserve, MNI

- Despite continued evidence of reserves putting downward pressure on overnight rates, most analysts see a Fed adjustment of administered rates as a close call. Prevailing opinion on whether the Fed will act at next week's meeting appears to be shifting toward an expectation of inaction, as the funds rate remains at 0.06% (despite a brief dip to 0.05%). MNI will have more out in our Fed Preview next Monday.

| Liabilities | Reserves | US Treasury General Account | Reverse Repo | Currency In Circulation | Other |

| Last Week's Net Change (USDbn) | -3.4 | -29.2 | 2.5 | 6.8 | 55.5 |

| 4-Week Net Change (USD bn) | -52.5 | -170.5 | 284.6 | 12.0 | 51.6 |

| Total Holdings (USD bn) | 3848.3 | 783.2 | 672.9 | 2176.9 | 454.4 |

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok