Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL MARKET/OPINION

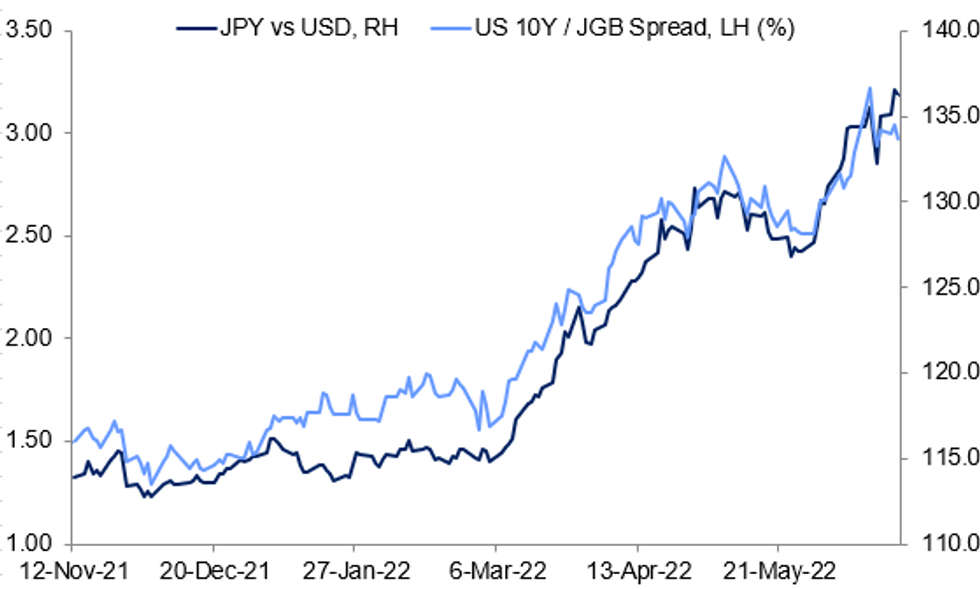

Per our Insight piece out earlier today: the Bank of Japan could adjust its easy monetary policy around the autumn if the yen stabilises at a lower level around 140 to the dollar, sending inflation to temporary peaks near 3% and driving wage hikes into 2023, MNI understands. That could involve adjusting yield curve control (currently the defended yield ceiling on 10Y JGBs is 0.25%).

- While our reporting points to a BOJ policy move further down the line (as our Insight headline suggests, only in autumn) and not immediately, we've had client questions about implications of potential hawkish BOJ policy shifts.

- In the case of unexpected intervention, or adjusting YCC, expect a big knee jerk move lower in the USD vs the yen (first key support comes in at 132.70/131.50 currently, vs 136.22 spot).

- Japanese stocks would sell off strongly, with global equities moving lower on the follow.

- Despite a risk-off move, global long-end yields would rise, with potential for bear steepening in tandem with JGBs. Even if the JGB employs just FX intervention and not YCC adjustment, there would be increasing speculation that the latter would be approaching.

- Likewise oil/industrial metal commodities would weaken as a negative growth impact would be anticipated (though a softer USD could mitigate some of the downside).

- Emerging Market assets would sell off sharply, in part because of the above global impact, and also because the yen is seen as a carry trade funder.

- The overall impact of an FX intervention would be sizeable for a short period of time but might not last, as unilateral interventions in the yen historically haven't worked for long. Abandoning YCC would have more lasting impact.

Source: BBG, MNI

Source: BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok