Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

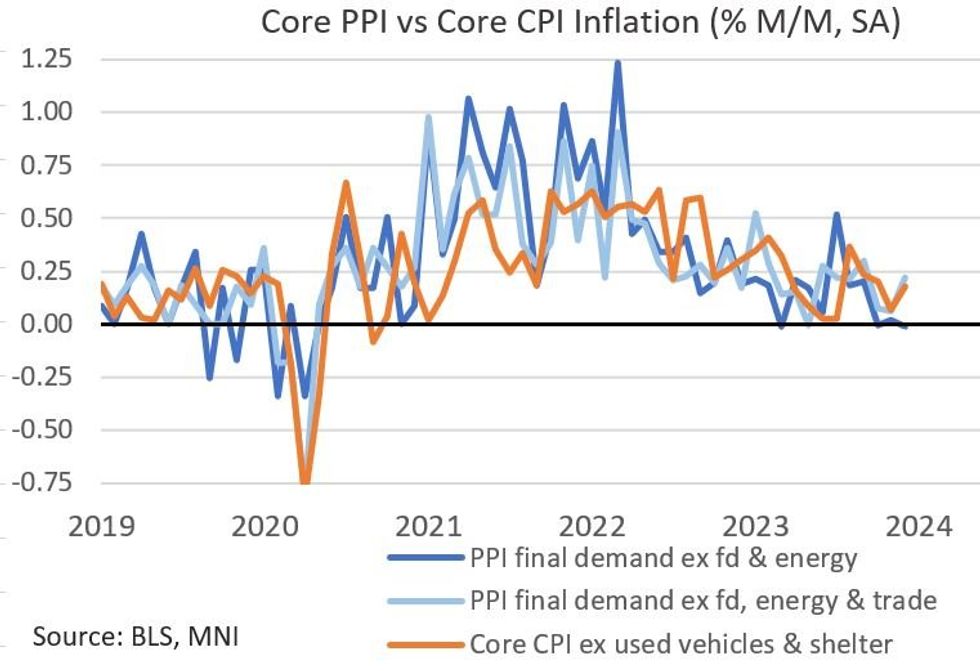

December's PPI report produced a downside surprise in terms of headline (-0.1% M/M vs +0.1% expected, and vs a -0.1% Nov figure that includes a downward 0.1pp revision), with ex-food/energy also soft (0.0% vs 0.2% expected, 0.0% prior).

- The ex-food/energy/trade metric was in line though, accelerating to a 3-month high 0.2% from 0.1% prior as expected.

- The most scrutinized areas though will be those that feed into the Fed's preferred measure of inflation: PCE.

- On this front there is no reason from this report to expect any upside revisions to those expectations than had been imputed by analysts after yesterday's CPI, and perhaps some bias toward downward revisions if anything - especially based on what was reported for the key healthcare services categories.

- Recall that sell-side analyst expectations for core PCE ranged from 0.12-0.15% M/M (BofA) to as high as 0.28 (Citi)-0.3% (unrounded, Wrightson ICAP) post-CPI yesterday.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok