Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

SPAIN DATA

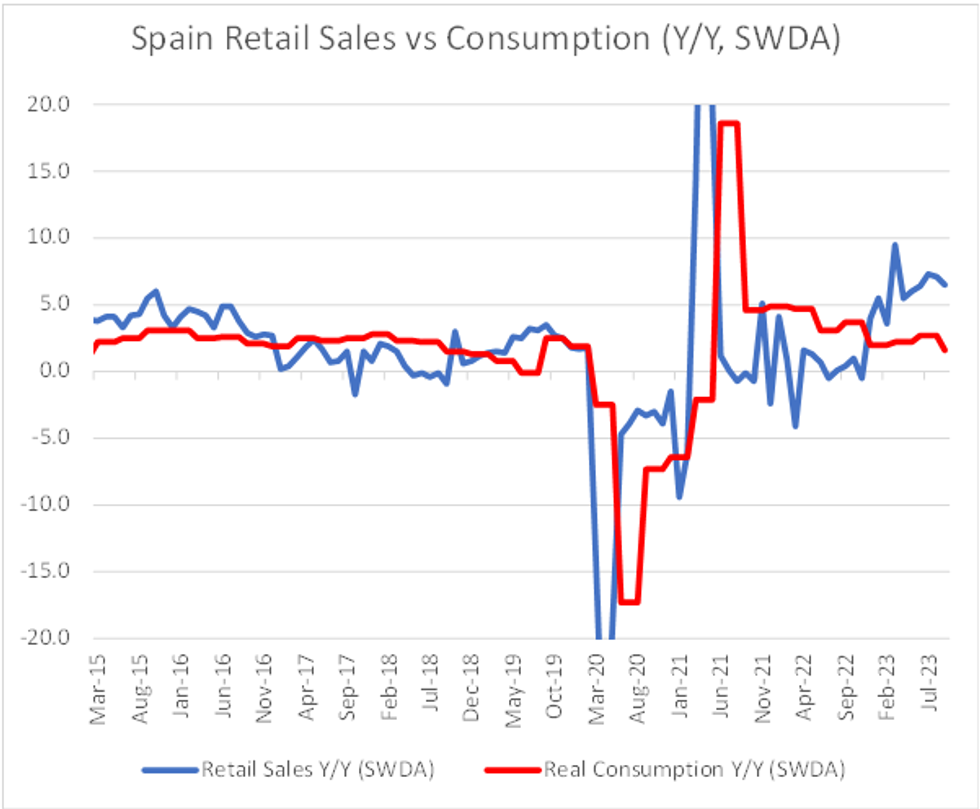

Spanish Q3 flash GDP printed a touch firmer than expectations, offset by downward revisions to Q2. The prints came in at +0.3% Q/Q SWDA (vs +0.2% cons; a revised +0.4% prior) and +1.8% Y/Y SWDA (vs +1.7% cons; revised +2.0% prior). Retail sales were lower in September at +6.5% Y/Y SWDA (vs +7.1% prior).

- Looking at the details of the GDP release, there is evidence of slowing overall activity in the Spanish economy, which is consistent with the general downtrend in the Spanish composite PMI since March (though September saw a slight uptick to 50.1 vs 48.6 in August).

- Y/Y consumption fell -1.1pp to +1.6% Y/Y, though the +1.2% Q/Q print was +0.1pp higher than the Q2 print. The slowdown in retail sales for September has been accounted for in the GDP print using provisional advanced results, according to INE.

- GFCF was -1.1pp Y/Y lower at +0.6% Y/Y and also turned negative Q/Q (-0.4% vs 1.9% prior) while both imports and exports remained negative on a quarterly and annual basis, with lower prints than seen in Q2.

- Hours worked rose on a quarterly and annual basis, aided by an increase in the number of full-time positions (consistent with the unemployment release yesterday).

- The release notes that revisions to today's figures may be more volatile than usual given the rapid tightening of monetary policy and volatility of prices.

- 10-year Spanish bond yields rose 2bps following the release, but have since fallen to intraday lows alongside core EGBs. 10-year Spain/Bund spreads sit 1.2bps tighter at 109.6bps.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok