Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

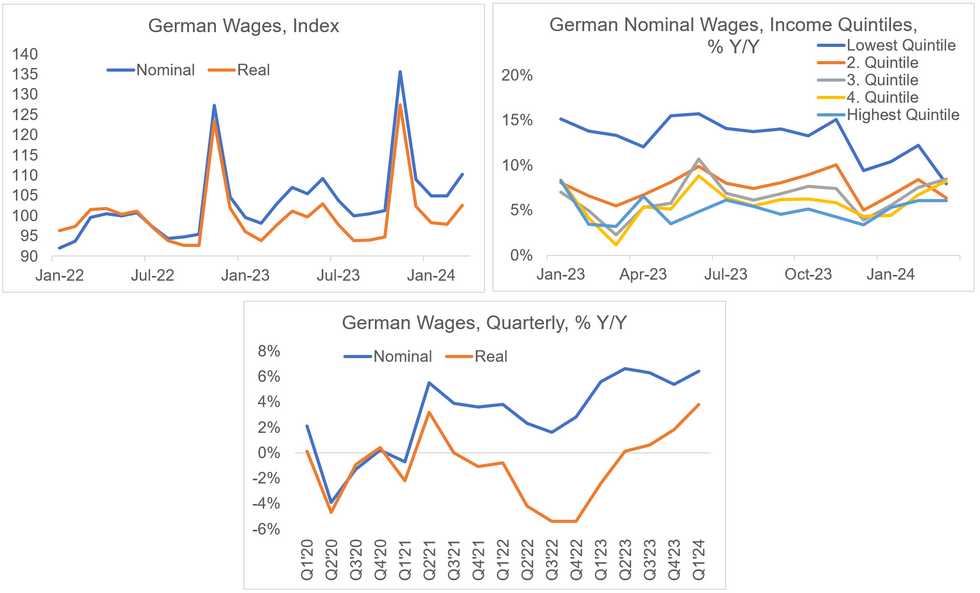

German real wages rose by 5.0% Y/Y in March (vs +4.3% Feb). This brought Q1 growth to 3.8% Y/Y (vs 1.8% prior), the highest quarterly growth rate since inception of the series in 2008, and the fourth consecutive quarterly rise - following negative real wage growth between Q4'21 to Q1'23. (The March rise was also the series high albeit only extending back to 2022)

- Nominal wages rose 7.3% Y/Y in March (vs +6.8% prior) and 6.4% Y/Y in Q1 (vs +5.4% prior); the real series is deflated by CPI.

- The print does not come as a major surprise after data last week showed a negotiated wages rise of +11.7% in March, which was driven by broad-based contract expiries in the sector ('GERMAN DATA: Negotiated Wages Warrant Upside Risks to Overall EZ Figure' - MNI, May 22).

- One-off inflation reimbursements had a strong positive impact on the Q1 figure, Destatis added, which was in line with MNI's expectations based on previously reported developments ('GERMANY: 3/4 Employees Covered by Collective Agreements Received Inflation Reimbursement' - MNI, March 14).

- Breaking down income stratification by full-time employees based on earnings, the lowest paid quintile saw strong nominal wage growth at +7.9% - the wage growth rate here was slower than previously, though (12.2% prior, 13.7% 2023 average).

- The acceleration in the overall reading was meanwhile driven by the 3rd and 4th quintiles.

- Overall this increase is seen as a catch-up for German employees after the inflation surge eroded real wage gains.

- But continued real wage inclines would portend a recovery in consumer spending going forward, especially considering the uptick was driven by quintiles around the median household. This could provide positive underpinnings for overall GDP growth, which has been driven so far this year by net exports and construction.

MNI, Destatis

MNI, Destatis

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok