Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS SUMMARY

There was no let-up to Tsy weakness in overnight trade, with the long end getting hit once again. Double-digit rises in Aussie and Kiwi yields seen as the catalyst in Asia-Pac trading, with weakness continuing in the European session.

- The 2-Yr yield is up 1bps at 0.1328%, 5-Yr is up 6bps at 0.6608%, 10-Yr is up 6.7bps at 1.4424%, and 30-Yr is up 6.2bps at 2.2949%.

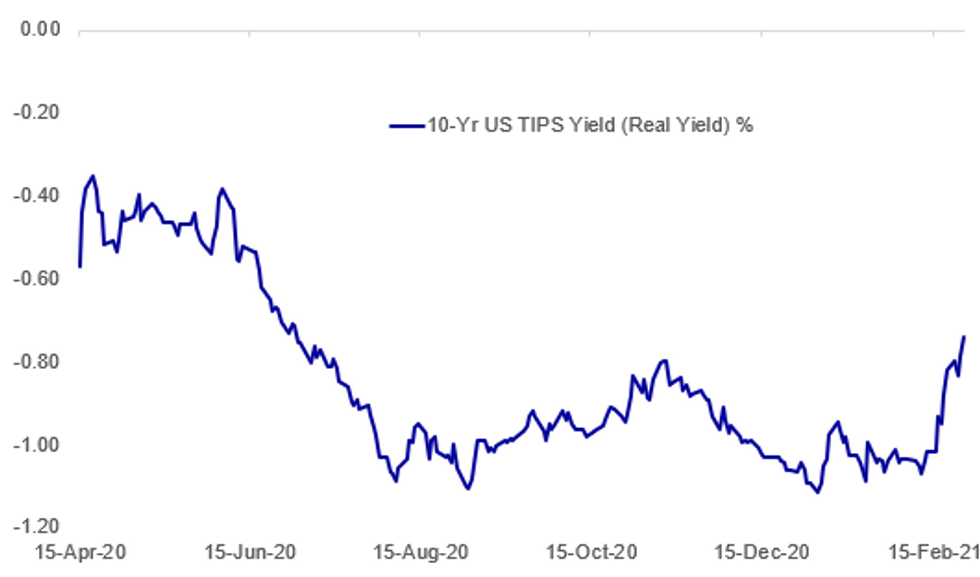

- 10-Yr real yields hit the highest levels since Jul 2020 (albeit still negative w 10 TIPS at -0.7316%); 2s30s nominal since 2015, 5s30s since 2014.

- 0830ET data: jobless claims alongside Jan prelim durable goods orders and second reading of Q4 GDP. Pending Jan home sales at 1000ET, with KC Fed Mfg at 1100ET.

- Another busy schedule of Fed speakers today: 0830ET is Atlanta's Bostic, 1030ET StL's Bullard, 1110ET VC Quarles, 1500ET NY's Williams.

- In supply, 1130ET sees $65B of 4-/8-week bill auctions; 1300ET is $62B 7Y Note auction. NY Fed buys ~$1.75B of 20-30Y Tsys.

BBG, MNI

BBG, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok