Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GERMAN DATA

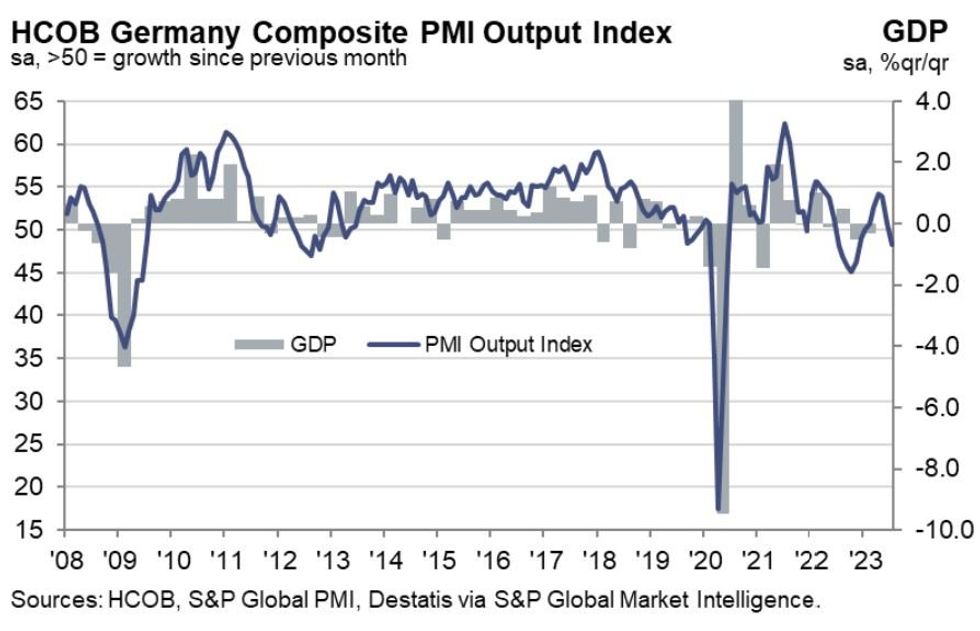

German Manufacturing activity contracted sharply per the July flash PMI reading of 38.8, which was well below the 41.0 expected and the 40.6 prior. Services also decelerated to 52.0 vs 53.1 expected (and 54.1 prior), with composite well into sub-50 territory at 48.3 vs 50.6 prior.

- While the Composite reading was merely an 8-month low, and Services a 5-month low, Manufacturing's slump represented a 38-month low with production falling at the fastest rate since May 2020 "amid rapidly declining demand for goods" (per the HCOB / S&P Global report).

- The Services outlook wasn't positive either: new business fell for the first time in 6 months and overall composite new orders posted the worst reading in 3 years amid a range of demand-hampering factors including " customer hesitancy, destocking, high inflation and rising interest rates".

- With backlogs declining quickly, expectations toward future activity were the worst since December 2022, and employment growth slowed to the joint-weakest in 2.5 years (Services hiring slowed, while manufacturing jobs dropped outright for the first time since January 2021).

- The "good" news was a continued deceleration in price pressures. The bad news is that there is a divergence here between manufacturers and the services sector. Overall costs were the lowest in nearly 3 years, but this was due entirely to a sharp drop for manufacturing prices (both input and output), vs service sector costs accelerating vs June (again, both input and output).

- This is a recessionary set of data, with the report noting that “over the last few months, we have seen a jaw dropping fall in both new orders and backlogs of work, which are now declining at their fastest rates since the initial Covid wave at the start of 2020. This doesn’t bode well for the rest of the year".

- The wrinkle here is that services inflation looks more stubborn than that of goods, which somewhat complicates the ECB's assessment of the overall inflation dynamics amid a clearly weakening demand picture.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok