Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

BOJ

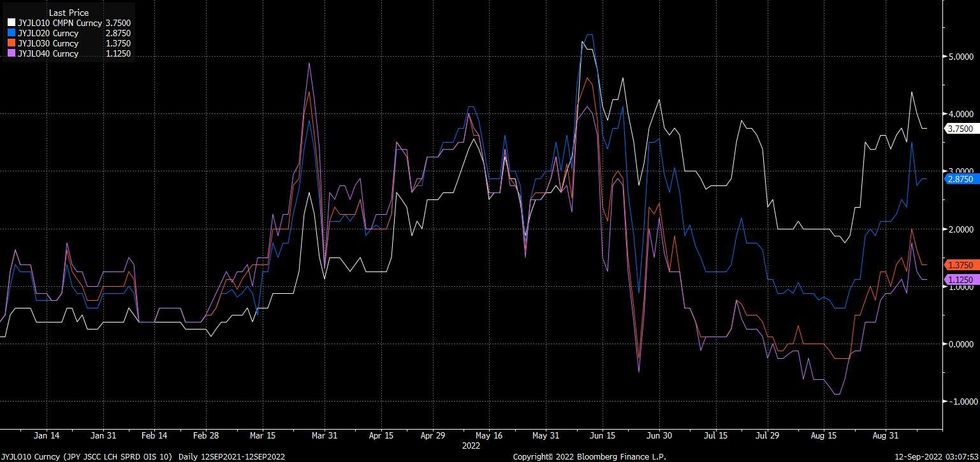

With 10-Year JGBs yielding close to the cap of the BoJ’s permitted trading range (-/+0.25%) we note that LCH/JSCC swap spreads covering the 10+-Year zone have widened recently, although they remain shy of their respective June highs, when foreign speculators were the driving force behind the (ultimately unsuccessful) challenge of the BoJ’s YCC settings.

- 10-Year swap spreads have re-widened, but still operate well shy of their mid-June peak.

- It would seem that the BoJ’s rhetoric and actions since mid-June have curbed at least some of the appetite for speculation surrounding capitulation re: the Bank’s current YCC settings.

- The BoJ has continued to conduct daily fixed rate operations. Last week saw the first offers received in such operations since June.

- Last week also saw the Bank step up the size of its regular 5- to 10-Year Rinban purchases.

- With global core bond yields on the up. and the higher for longer mantra headlining FOMC rhetoric, the BoJ is set to come under rounds of pressure in the months ahead, particularly with most being of the opinion that the BoJ will not alter its monetary policy stance through the end of Governor Kuroda’s current term (which ends in April ’23), a view that has received more of a backing in the wake of the Bank’s verbal and market-based commitments to its current policy settings.

Fig. 1: 10- to 40-Year LCH/JSCC Swap Spreads

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

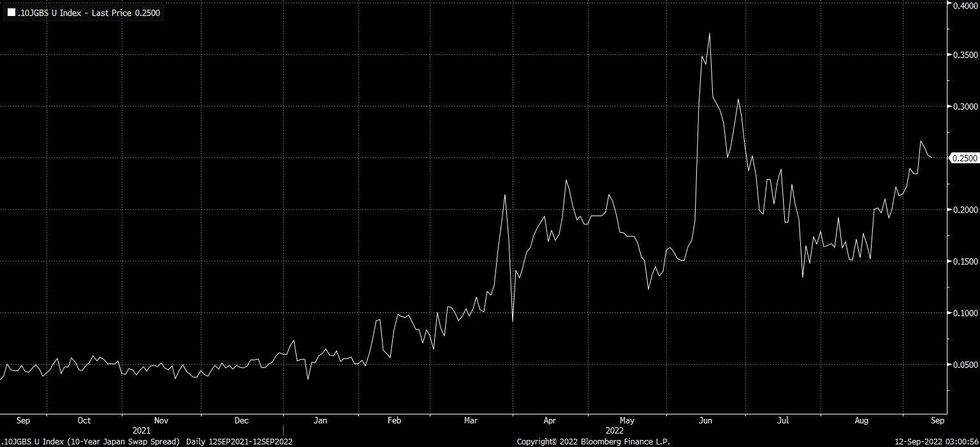

Fig. 2: Japan 10-Year Swap Spread

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok