Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

ITALY DATA

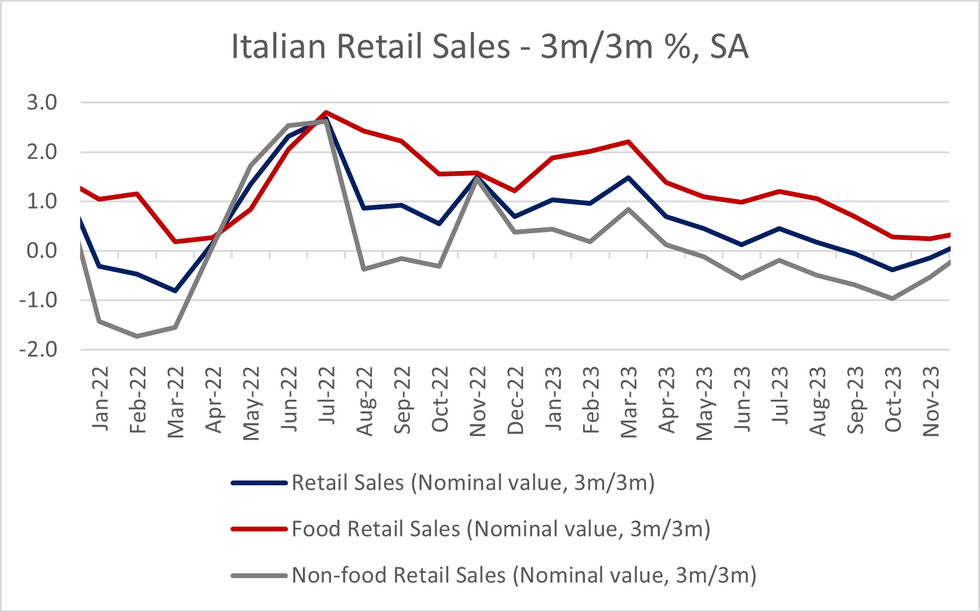

Italian retail sales (in nominal value terms) softened in December, falling -0.1% M/M SA (vs a -0.1pp downwardly revised +0.3% prior) and rising +0.3% Y/Y NSA (vs a -0.1pp downwardly revised +1.4% prior).

- However, the less volatile 3m/3m measure showed a third consecutive increase in nominal retail sales, to +0.21% 3m/3m SA (vs -0.15% in November and -0.38% in October).

- Measured in real volume terms, sales fell -0.21% 3m/3m SA (though have risen for a fourth consecutive month from -1.20% in September. The volume series is adjusted using the HICP index.

- The outlook for the Italian retail sector has shown tentative signs of improvement in recent surveys. The EC's retail trade confidence metric reached its highest level since April '23 in January (at 14.5 vs 11.3 prior).

- Additionally, consumer confidence in both the EC and ISTAT surveys rose in January. However, both remain in contractionary territory, with the EC measure at -16.0 (vs -16.1 prior) in January and ISTAT's at 96.4 (vs 95.8 prior).

- A reminder that in the flash Q4 GDP release (where Q4 GDP was estimated at +0.2% Q/Q and +0.5% Y/Y), ISTAT noted that domestic demand was a negative contributor, offset by a rise in net exports.

The combined real NSA volume of sales in November and December 2023 was -2.9% lower than the same months in 2022. This combination allows for a cleaner comparison of sales during the Black Friday/Christmas periods, where discounting etc. can lead to volatile monthly prints.

- Looking at the components of today's release, food sales in nominal value terms fell -0.2% M/M while non-food sales were flat. Compared to December 2022, food sales rose +2.2% Y/Y (vs +4.0% prior) and non-food sales fell -1.1% Y/Y (vs -0.5% prior). This was the 5th consecutive month that the annual rate for non-food sales was negative.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok