Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CHINA RATES

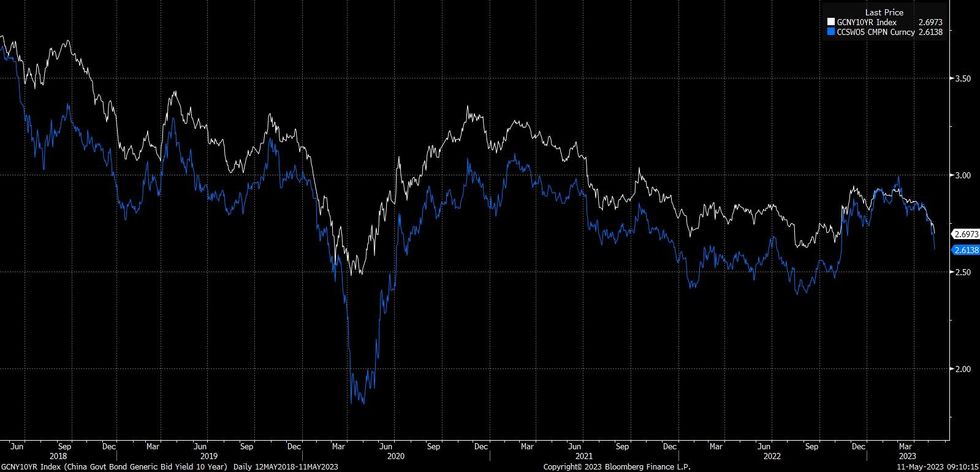

The softer than expected inflation data for April and yesterday’s RTRS sources piece suggesting that “China has told its “big four” state-owned banks to cut deposit rate ceilings on some products” (click for full story) weighed further on CGB yields & Chinese IRS swap rates on Thursday. Recently released, softer than expected credit data could apply further weight early on Friday (with the data breaker a run of firmer than expected readings).

- 10-Year CGB yields and 5-Year IRS rates were already back to levels that we haven’t seen since ZCS times owing to worry surrounding the uneven Chinese economic recovery (as noted earlier this week), but we are getting towards levels that would seemingly require a more meaningful easing bias/realisation of “backdoor” action from the PBoC.

- Nomura note that “the market’s focus on potential bank deposit rate cuts has been one of the drivers of lower China rates in recent weeks. If it materializes, it could be a signal that the PBoC is validating the recent move lower in money market rates. However, following the recent strong rally, we expect China rates to consolidate around current levels, assuming the upcoming credit data are not much lower than the currently subdued expectations of the market. Given the low readings of both CPI and PPI inflation, we believe the likelihood of a PBoC policy lending rate cut has increased, although it is not our baseline case.”

Fig. 1: China 10-Year Government Bond Yield & 5-Year Interest Rate Swap Rate (%)

Source: MNI - Market News

Source: MNI - Market News

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok