Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

GLOBAL

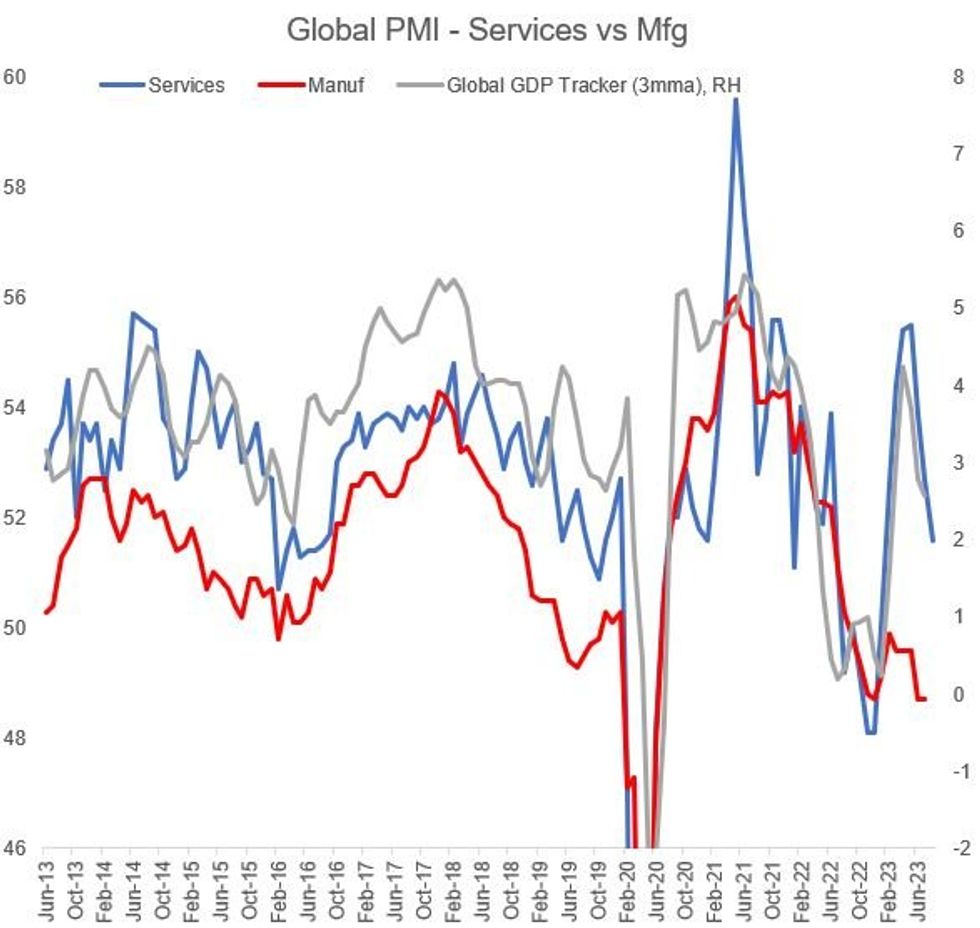

Based on today's flash August Services PMI readings (Eurozone 48.3 vs 50.9 Jul, UK 48.7 v 51.5 Jul, Japan 54.3 v 53.8 Jul, and US 51.0 v 52.3 Jul), the early read on the Global Services PMI (pending the official JPMorgan release on Sep 6th as well as China's August figures) is that it decelerated this month but remained in expansionary territory, at around 51-52.

- That compares to the recent peak of 55.5 in May, which decelerated to 52.7 by July. There hasn't been a contractionary Global Services PMI reading this year, but August's looks set to mark the lowest since January's 50.0.

- While Manufacturing PMIs' decline appears to have flattened out at weak/contractionary levels, they haven't been nearly as useful a guide to overall economic activity in the past year or so as Services, since supply chain issues began clearing up and consumer demand switched heavily to services from goods.

- If confirmed at just above 50 (and especially when considering the ongoing weakness in manufacturing growth), the Services PMIs point to below-trend global GDP growth of 2% in the 3 months to August, close to the pace of expansion seen in May 2022 as the Russia-Ukraine conflict and China Covid lockdowns weighed on activity.

Source: MNI, S&P Global, JPMorgan, BBG GDP Tracker

Source: MNI, S&P Global, JPMorgan, BBG GDP Tracker

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok