Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FRANCE DATA

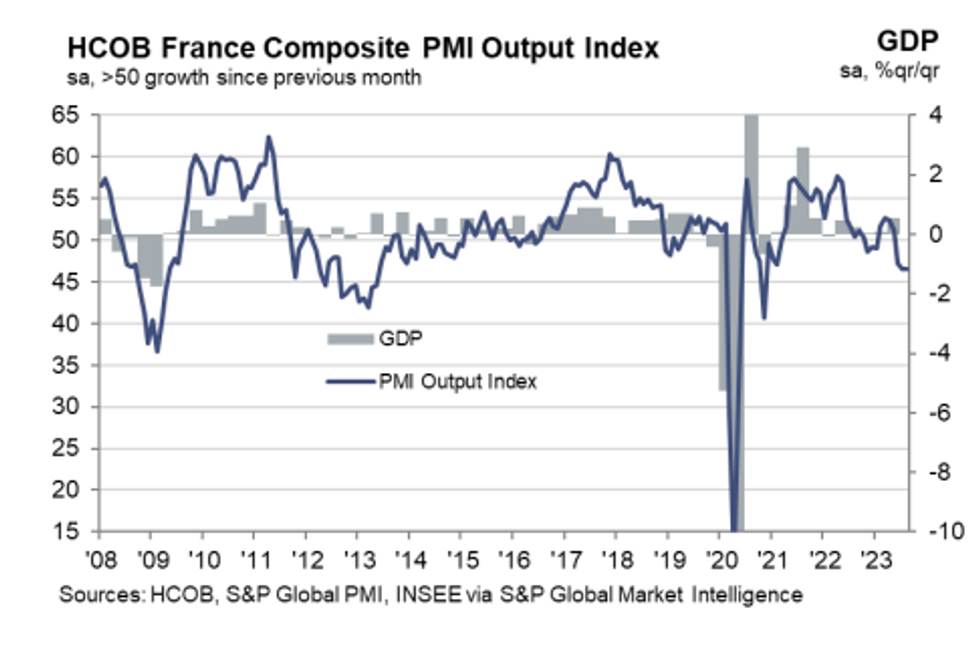

France's flash August PMI report points to further deterioration in economic activity as we go through Q3, most notably with the Services index dropping for the 3rd consecutive month to a 30-month low 46.7 versus an acceleration to 47.5 expected (from 47.1 Jul).

- While Manufacturing beat expectations by accelerating to a 5-month high 46.4 vs the expected 45.0 (45.1 Jul), overall Composite PMI was static at 46.6 vs the expected improvement to 47.1. Export orders fell sharply, continuing to present what the HCOB S&P Global report called a "considerable drag".

- That meant overall activity continued to contract at the quickest pace since Nov 2020.

- Weakness in the report was widespread: demand was poor, with new orders recording accelerated drops for both services and manufacturing firms, and backlogs were near 3-year lows. As such manufacturing continued its long output slump and services output volumes dropped at the fastest in 2.5 years.

- But interestingly while job creation weakened to the softest since Jan 2021, overall employment levels rose, driven entirely by services companies. As the report notes, that could mean that the French unemployment rate will continue to fall potentially to the lowest in over 40 years in Q3.

- As we go into the ECB's September decision, the Governing Council will take note that inflation rates continued on their downward trajectory, with overall input price inflation down to a 29-month low, and selling price inflation slowing to its weakest since April 2021.

- However that masked mixed sectoral dynamics: manufactured goods output prices fell but services charges rose. While it looks as though services disinflation is in the pipeline, it has not arrived yet, amid continued tightness in the services labour market.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok