Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

FED

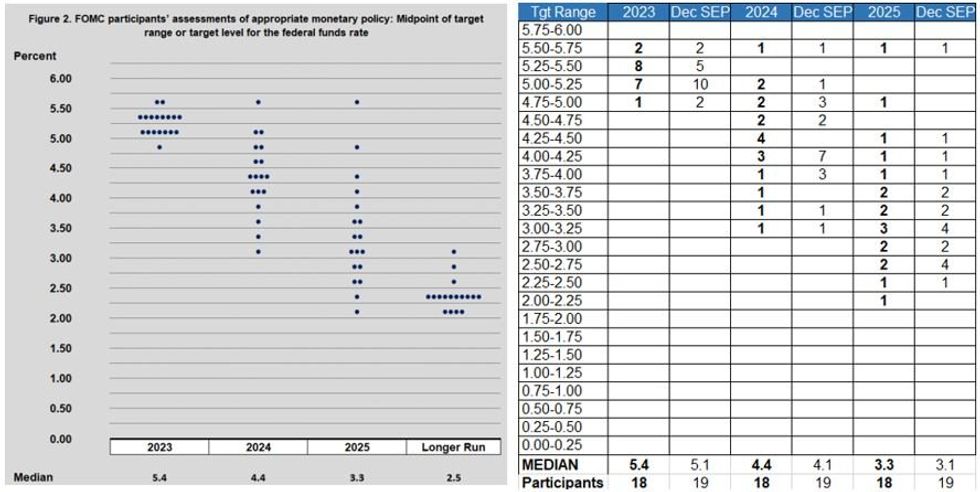

As Chair Powell said in December of the SEP Dot Plot 2023 terminal rate median, “if the inflation data come in worse, that could move up [from 5.1%]. And it could move down if inflation data are softer.”

- The inflation data have not come in softer since then, with the labor market continuing to impress to the upside. And Powell in early March accordingly said “The latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated.”

- That means the FOMC medians are likely to be revised accordingly in this week's projections. However, any increase in the signalled terminal rate is likely to be tempered by rising uncertainty over financial stability.

- In a close call, we see the 2023 median dot revised up to 5.4% from 5.1%, with the 2024 dot lifted from 4.1% to 4.4%. This would imply a couple more 25bp hikes beyond March (May and June) as the baseline case this year, with the same 100bp magnitude of cuts in 2024 as forecast in the December projections.

- The high-low range for 2025 could be wider, with the end-year rate probably nudged up slightly (we have pencilled in a split between 3.125% and 3.375% for a 3.25% ie 3.3% median. Though the end-2025 outlook entails a low-conviction view for us – and, we suspect, the FOMC itself.

- As reflected in our Instant Answers, there will be additional attention paid this time to the number of dots (if any) pointing to a hold for the rest of the year (ie 4.9% assuming a 25bp hike this week), and/or any cuts. Either is expected to be limited.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok