Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER CYCLICALS

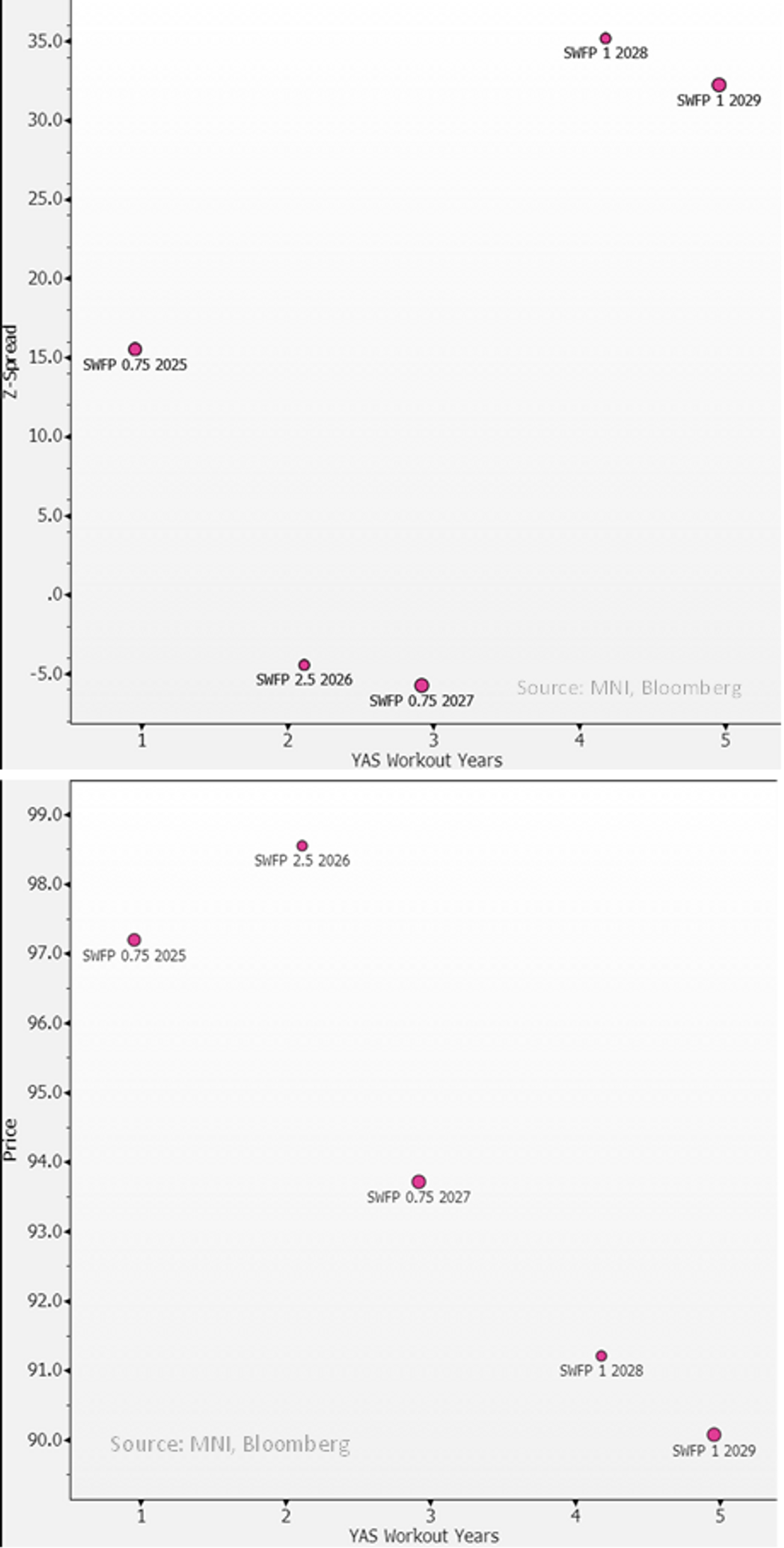

We've seen some strange moves on the Sodexo lines recently but we hear it's on thin flows/a lack of free-float.

- Curve is still dislocated after company completed a consent solicitation in mid-last year (at 0.25% fee) which enabled it to prevent a Event of Default trigger from bondholders on the Pluxee (PLXFP; NR, BBB+; S) spin off. It clearly met material subsidiary triggers in clauses with FY23 Pluxee operating profit making up 34% of group vs. the hurdle 10%.

- The spin-off was announced early last year which is when spreads headed negative. We are not sure why its stayed there (consent solicitation was voted on by August last year) - investors may be eyeing debt paydowns (it has done one par call on low coupon €25 but looks linked to consent solicitation hitting wall).

- New supply should be unaffected by above but that looks unlikely this year - front maturity is still a year away & leverage at 2.3x (at end of Feb) is still holding above target 1-2x.

- Moody's on Negative outlook, we expect it to stay there for now. Rating directions contingent on the pace of leverage reduction on both earnings growth (c+26%yoy on FY24 EBITDA) & any debt paydowns (gross currently €4.8b with €1.4b cash on hand). Debt paydowns over 1H (6m ending Feb 2024) included a par call on the €300m 1.125% May 25s (was 'terminated' during the consent solicitation process) and letting the €500m 24s roll off.

- In addition to € lines below, co does have $26 & 31s totalling $1.25b & a £250m 28s.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok