Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

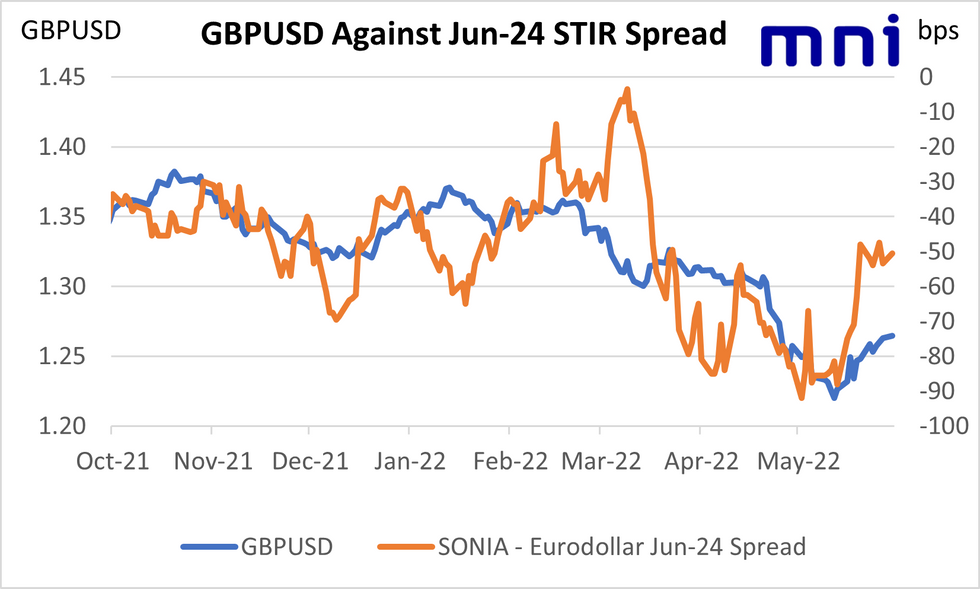

GBPUSD

- Over the past couple of weeks a gap has opened up between STIR future spreads and GBPUSD.

- The gap opened up notably after the release of strong UK labour market data on 17 May and then moved to its current level following the strong UK retail sales (around 50bp for ED-SONIA Jun-24 spread).

- The move in GBPUSD was much more muted for both of these releases, and as can be seen from the chart, GBPUSD has generally remained less volatile than the STIR spread over the past few months.

- However, it is notable that GBPUSD continues to grind higher over the past couple of weeks, narrowing the gap, but only slowly.

- So the question is, will GBPUSD move back to around 1.32, will the SONIA-ED Jun-24 spread move back down to -75bp, or will it be a combination of the two? We think GBPUSD may continue to grind a bit higher but for us the more probable answer would be that the SONIA-ED spread re-widens. We still think that 50bp BOE hikes look fairly unlikely and in that scenario its not going to take long for rates to be higher in the US than the UK.

- We also think that as the neutral rate in the US seems to be higher than in the UK, rates may already be starting to move into moderately restrictive territory in the UK this year, while it seems likely that in the US, it will take longer. The UK is also more exposed to energy price shocks than the US (with the integrated European gas networks and due to electricity generation differences) which could push real incomes down even more than currently projected in the UK. (Although the recent moves in US gap prices suggest this isn't just a European-centric move).

Source: MNI, Bloomberg

Source: MNI, Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok