Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE

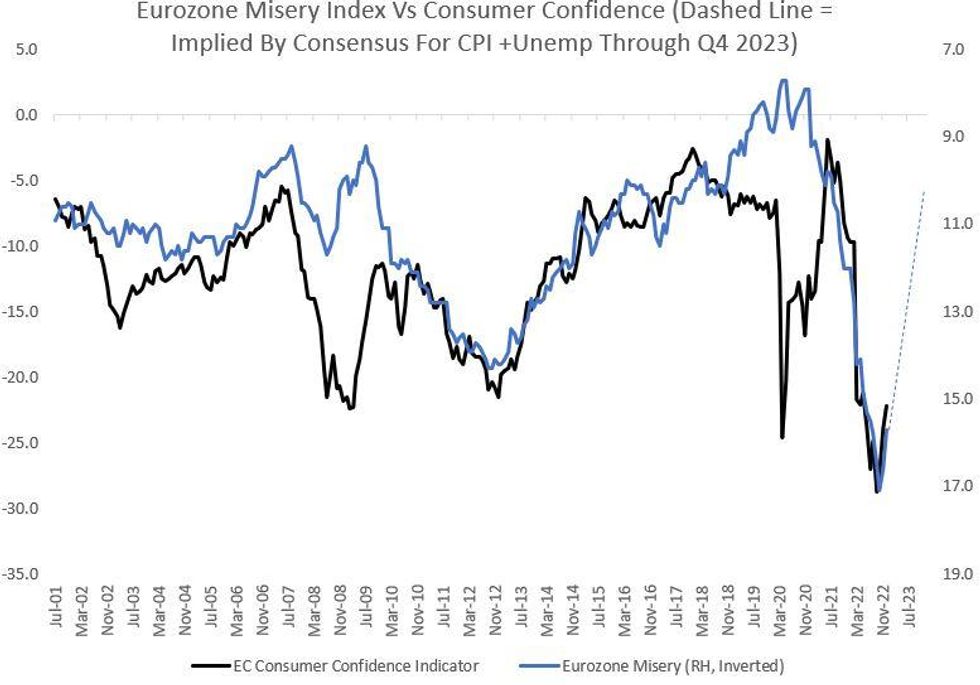

The improvement in eurozone inflation and unemployment outlooks bodes well for a further rebound in consumer confidence. Our Eurozone Misery Index (CPI Y/Y + Unemployment) remains highly correlated to consumer sentiment.

- Although eurozone core inflation continues to climb (to a record 5.2% in Dec), the upward turn in consumer sentiment is fully explained by headline CPI decelerating (10.7% in Oct to 9.2% in Dec).

- Assuming the unemployment rate doesn't rise much in the coming months (consensus has it rising 0.7pp to 7.2% in 2023), it will probably take significant further headline disinflation for a major improvement in confidence.

- But that is what's expected: CPI is seen in the BBG survey as collapsing to 3.5% by Q4, which added to the unemp rate suggests a Misery Index of between 10-11%, bringing consumer confidence closer to normal non-recessionary levels (see chart).

- The coming months will pose a dilemma for ECB policy in this regard.

- Headline inflation is set to continue falling, which bodes well for household inflation expectations remaining contained, and avoiding second-round effects. But with consensus (and the ECB's latest projections) still expecting a recession, stronger growth and consumption prospects than had been feared late last year mean consideration will have to be given to upside risks to activity and still-stubborn core inflation.

- This would give the ECB more impetus to continue hiking rates after the 100bp priced for Feb and Mar combined is delivered. MNI's ECB sources piece out Wednesday quoted a source saying "markets already assume a slowdown...we might have in the end to overshoot" on rate hikes.

- Currently, 139bp of hikes is seen to the July peak, equivalent to a depo rate just under 3.40%. That may yet prove a floor rather than a ceiling, with growth expectations likely to have bottomed, improving confidence pointing to stronger activity, and increasing focus on core rather than headline inflation.

Souce: EC, Eurostat, BBG Survey, MNI

Souce: EC, Eurostat, BBG Survey, MNI

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok