Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

CONSUMER STAPLES

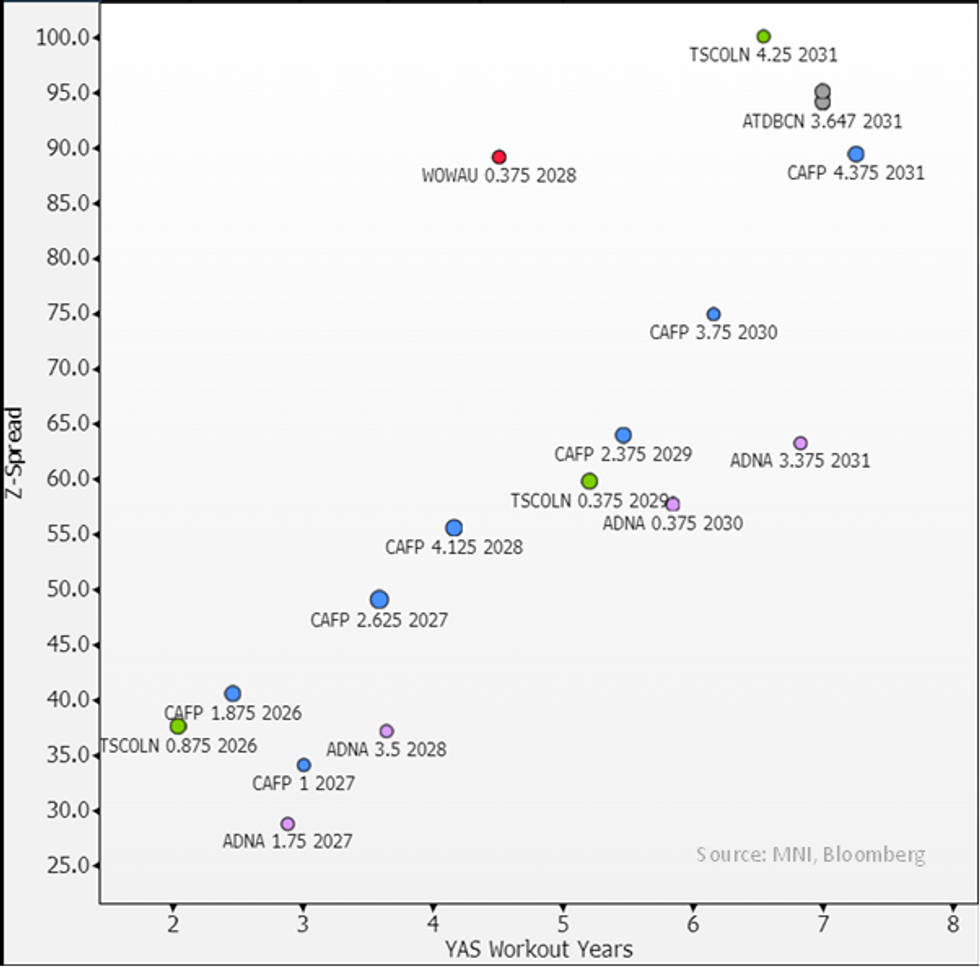

Screen cheap on €31s & flatteners, £ deal does not rule out local supply/refi on €470m July line coming up.

- It was in £ markets with a 10Y today. Docs look unaltered which has boosted our confidence on the bank sale not meeting default thresholds. We bring back a screen cheap on the 31s and don't mind flatteners against the 29s. Former should be clear of any EOD risk (trade at €102.6, voted on by bondholders) while flatteners will be exposed to large downside if par call does eventuate (which we see little to no risk of now).

- Leverage is at 2.2x vs target 2.3x-2.8x - we don't see rating risk on controlled moves within that (it was at 2.6x last year). We see Tesco bank sale as net positive (raters have noted neg. on loan book exposure previously). On the 60% ownership in stores it has (valued at £16.9b) we see risk limited with devaluations last year at -2%. Moody's in the past seemed to interpret it as a net positive noting it was "additional source of financial flexibility".

- Its only maturity this year was/is a July €470m outstanding (€750m issued) line. UoP on the sterling deal today is left broad - front maturity there was a £400m May 25. On balance we see refi on July line as still likely (i.e. today's £deal was net supply) particularly given headroom on leverage.

- Adding to that consensus has EBITDA growth at 3.7% in FY25 (12m ending Feb) which will help leverage cycle ~0.8x lower. Guidance from Tesco is for retail FCF of £1.4-1.8b, down from £2b in FY24 mainly on rising capex (+£200m) but will get cash inflow from closure on bank sale (its directing most of this to bumped up equity returns).

Previous RV note (flatteners 5bps in since)

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok