Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US DATA

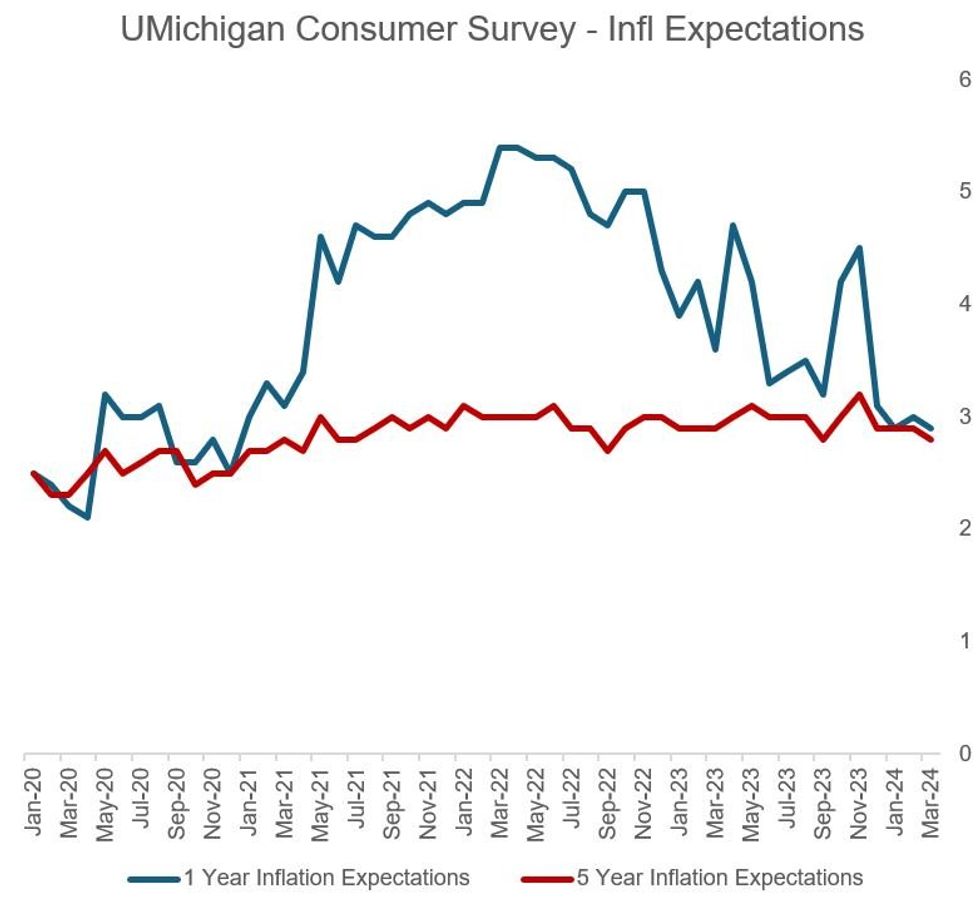

Softer inflation expectations are the story of March's final UMichigan consumer survey release.

- 1-year inflation expectations unexpectedly fell to 2.9% in the final report, from 3.0% in the prelim (and vs an expected rise to 3.1%). 5-10 year expectations dipped to 2.8% from 2.9% prior/prelim.

- That's the joint-lowest 1-year ahead inflation expectation in the survey since December 2020 (joint with Jan 2024), while the long-term inflation expectation was the joint-lowest since September 2022.

- That appears to have underpinned the strongest overall sentiment reading (79.4, vs 76.5 expected/prelim) since July 2021. The text from the UMichigan survey suggests as much and could give some additional confidence to FOMC doves that the public is buying the message that disinflation, in the words of the report, "had truly turned the corner" lower:

- "Inflation expectations continued to come into focus for consumers...Consumers were unmoved by the slight uptick in realized inflation seen in the most recent CPI print and did not appear to alter their expectations in response...when the slowdown in realized inflation stalled in mid-2023, consumers’ uncertainty over inflation increased again, a sign that they were unconvinced that inflation had truly turned a corner. Data from recent months suggest that consumers made up their mind in December 2023. Not only did inflation expectations fall sharply, so did inflation uncertainty, demonstrating the consensus among consumers. As such, consumers are now broadly in agreement that inflation will continue to slow both over the short term and the long term."

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok