Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

EUROZONE DATA

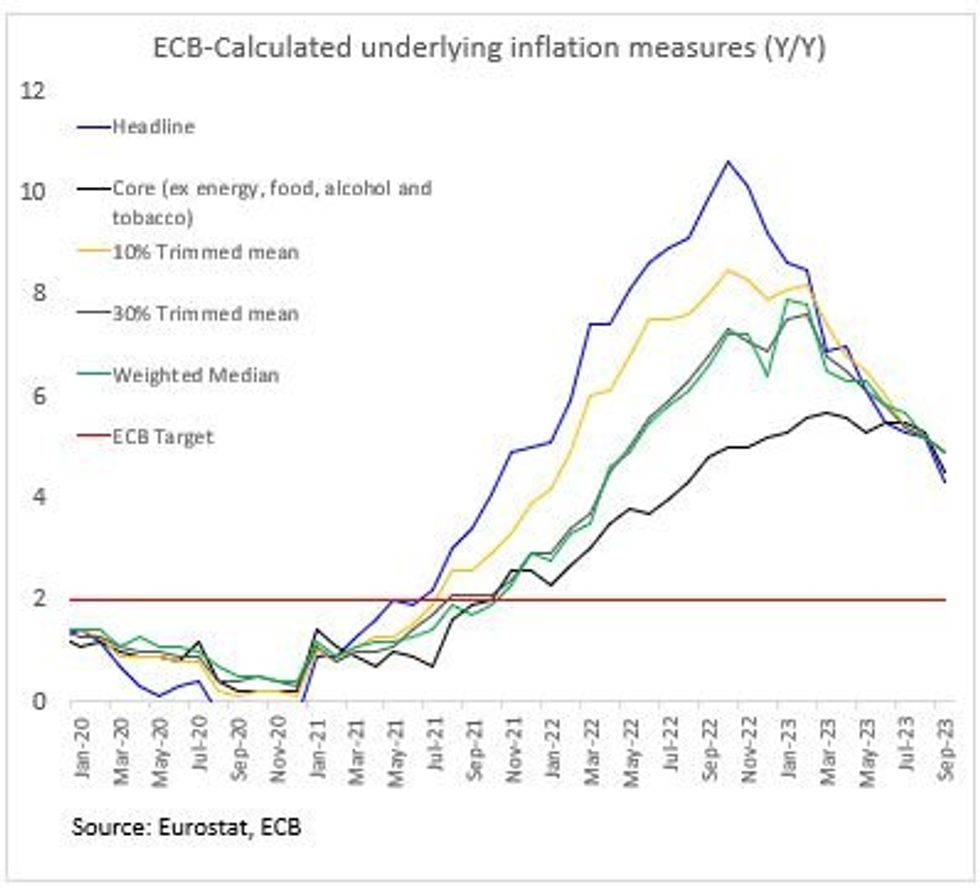

The ECB's measures of underlying inflation have been updated for the final September HICP data. While continued disinflation can be seen in some measures, those more focused on by the ECB (e.g. PCCI) show recent stickiness above the 2% target after significant progress in the preceding year.

- The overall PCCI (Persistent and Common Component of Inflation) index was 2.65% Y/Y (the same rate as July and August) - the rate peaked at 6.57% in June 2022.• ECB staff regard PCCI as a better (or at least as good) measure than any other underlying inflation indicator in terms of providing a medium-term forecast of the future headline HICP rate. As such, the stalling of the rate 0.6pp above the ECB's target may be a cause for concern.

- The PCCI rate excluding food and energy was more positive, printing at 2.11% Y/Y (vs 2.23% prior), the 8th consecutive month of disinflation.• Elsewhere, "Supercore" (another model-based approach) was 5.2% Y/Y (vs 5.5% prior) while the 10/30% trimmed mean and weighted median measures were all 4.9% Y/Y (vs 5.2% prior) - the first time any of the three have been below the 5.0% handle since May 2022.

- The ECB are firmly expected to hold rates at the upcoming October meeting, with the current terminal rate implied by the OIS market 4.031% in Dec 2023. Continued stickiness of key underlying measures may caution ECB members from signalling any loosening of policy in the coming months.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok