Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

USD

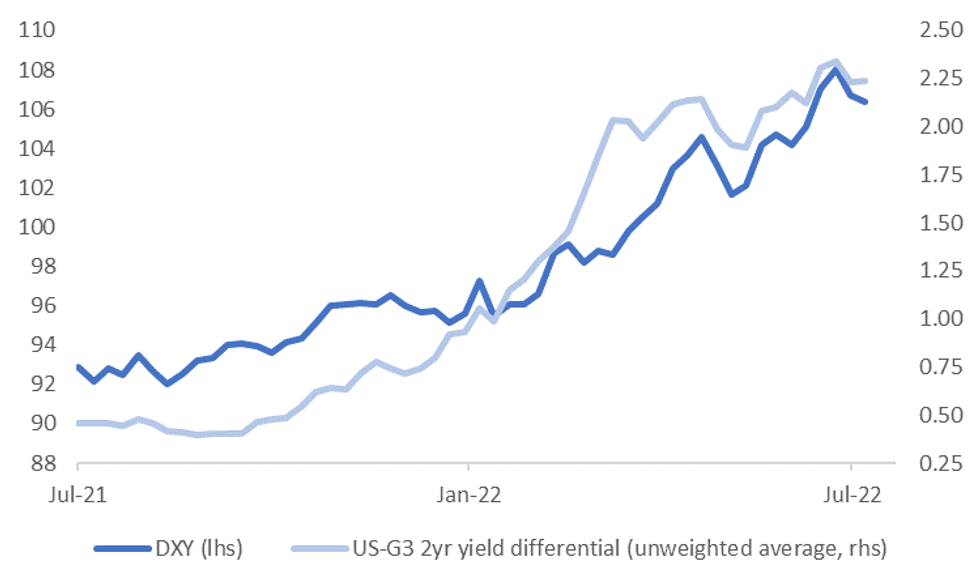

The DXY is not too far away from recent lows close to 106.00 (currently at 106.30). A break below 106.00 will have the market targeting the mid June highs of close to 105.80. Certainly yield momentum for the USD has waned, see the first chart below, although DXY weakness looks a little overdone at present levels.

- A lot is likely to depend on near term data momentum. Whilst the Citi US EASI index remains at depressed levels (last -53.50), it is up from recent lows.

- A number of major US banks upgraded their forecasts for tonight's GDP following better than expected partials (durable good orders and trade). The Atlanta Fed GDP nowcaster is up from its recent trough as well but is still negative at -1.2%.

- Avoiding another negative quarter of growth would certainly allay recession fears and should aid the USD against the likes of EUR and JPY, all else equal, particularly given the EU's on-going economic plight. Eurozone economic data momentum remains quite downbeat and focus is centred on gas supply issues as we progress through H2.

Fig 1: DXY & 2yr U.S. Yield Differential With G3 Economies

Source: MN - Market News/Bloomberg

Source: MN - Market News/Bloomberg

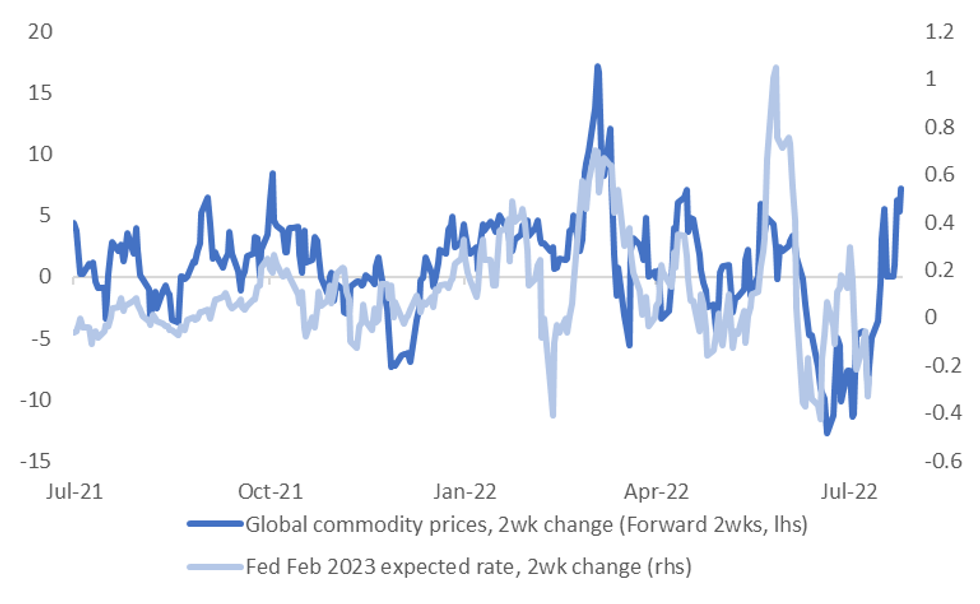

- Beyond the near term data picture, the focus will shift to further Fed action. Interestingly, the recent rebound in commodity prices suggests we won't see much more downside in terms of Fed expectations for early 2023, see the second chart below.

- There are some obvious caveats around this relationship though. Firstly, the link may not be as strong going forward given the extent to which the Fed funds rate has already been raised. Fed Chair Powell moved away from stringent guidance at the press conference on Wednesday. This makes sense with the policy rate operating around neutral levels.

- US real yields have also moved off their recent highs, with the 10yr measure slipping back to 36bps, from early July highs above 70bps.

Fig 2: Will Fed Expectations Continue To Be Lead By Commodity Prices?

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok