Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

JPY

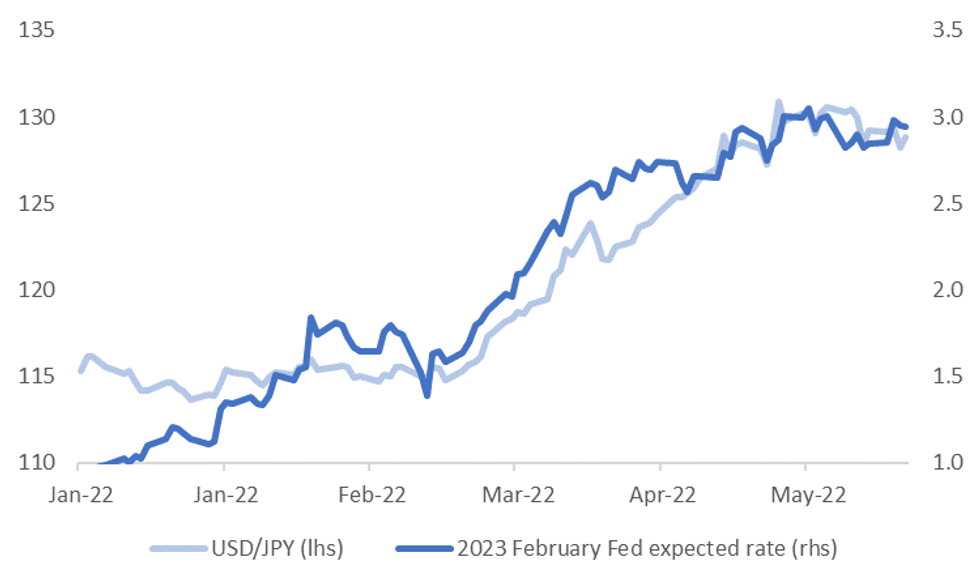

This time last week we noted that USD/JPY may struggle to make fresh highs if we saw a rangebound US Tsy environment and plateauing of Fed expectations (see this link).

- USD/JPY hasn't made fresh highs over this period, with a couple of sharp falls, however, dips remain supported, particularly sub 128.00, as was seen both last Thursday and today.

- Fed hiking expectations have edged higher over this period. The February 2023 implied rate sits close to 2.94%, up from the low 2.80% region last week, see the first chart below. Some of the major shifts in the Fed outlook have led USD/JPY moves, particularly since February.

Fig 1: USD/JPY & Fed Rate Expectations

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

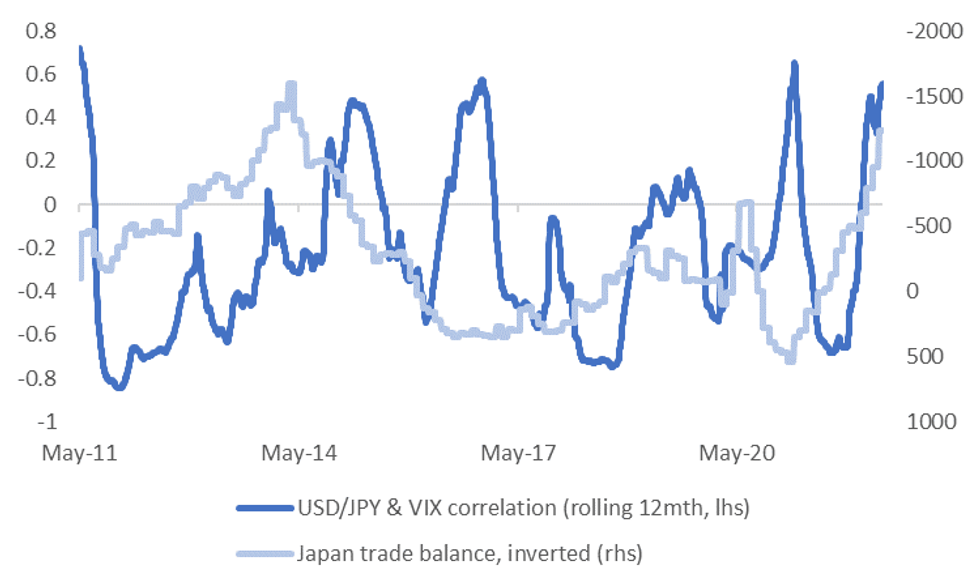

- The other factor to be mindful of is that the correlation between USD/JPY and the VIX index is quite positive at the moment, see the second chart below. The other line on the chart is Japan's trade balance, which is inverted.

- The basis for the chart is that when Japan is running a trade deficit, as it is at the moment, there is likely to be less support for the yen during risk off periods, as it has less external support to draw on. This is borne out in the chart to some degree, although the relationship is far from perfect.

- Today's Japanese trade data, for April, still showed import growth comfortably running ahead of export growth.

- Correlations can obviously change quickly, but for the moment risk off moves are not providing as much support to the yen than otherwise might be the case.

Fig 2: USD/JPY & VIX Correlations

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

MNI London Bureau | +44 0203-865-3809 | anthony.barton@marketnews.com

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok