Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

US TSYS

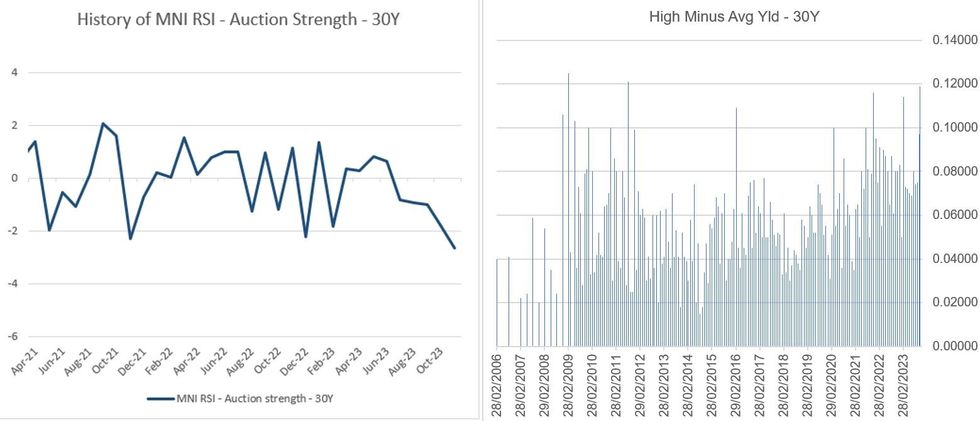

Thursday's 30Y Bond auction was historically weak and - while possibly a one-off - does not bode well for demand for duration without significant concessions.

- While we don't compile tail data that far back, multiple outlets/analysts have reported the 5.2bp was the largest for a 30Y sale since the 9.8bp in August 2011 after the US credit rating was downgraded from AAA by S&P.

- 30Y refundings are notorious for tailing. But there's no mistaking that the internals of the auction were very weak.

- The spread of the high yield minus the median yield - of 12bp - was likewise the highest since Aug 2011, dealer takeup of 24.7% was over double the average, and indirect awards were soft at 60% (10pp below average).

- The 5.2bp tail was actually quite close to November 2021's 5.1bp, but MNI's relative auction strength indicator came in at -2.66 for yesterday's sale, the lowest we've yet recorded.

Source: US Treasury, MNI Calculations

Source: US Treasury, MNI Calculations

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok