Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MACRO CREDIT

- As we saw in ETF data earlier this week, $HY has reversed to inflows (across funds) for the week ending Wednesday. Some weakness in €HY inflows (& £HY) this week - no signs of that in spread performance (-33bps). $IG saw strong inflows at ~1.5% of total funds. We've seen demand carry over to primary performance - NIC's 1-2bps vs. 8.5bps last yr & longer-term avg's of ~5bps - books covered >3* on all of this weeks sessions. The strong metrics despite above consensus supply ($43b vs. c$30b) & if supply has been brought forward opportunistically, leaves less than $30b/week for remainder of the month to meet Jan expectations - well shy of Jan's first week of $57b where we saw spreads struggle. Financial supply yet to come (equal skew MTD), spreads trading in par as well (financials are ~1/3 of index weight).

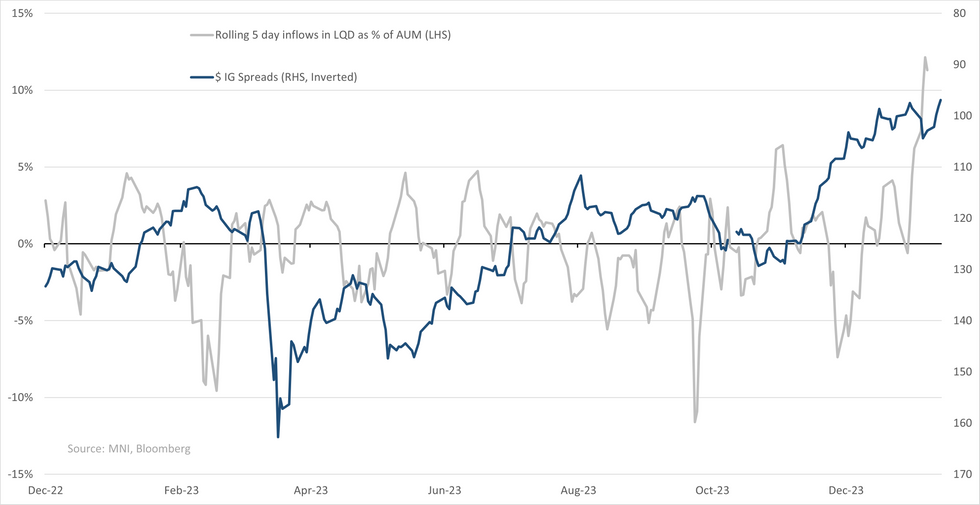

- Timely ETF data shows no reversal into week end - LQD (iShares iBoxx $ IG) saw $1.6b in inflows in the most recent session taking 5-day inflows as % of AUM to above 10% - highest levels in over a year. Investors are coming in with index yields at 5.1% vs. 6.4% in late Oct and index duration rising in the face of supply from 6.5 to 7. Its dropped protection/breakeven to 73bps (annualised) while spread breaks are approaching single digits. Though investors may find support from yesterday's CPI & last week's NFP- rates largely trading past any strength in both & holding onto most of last years peak easing priced. Forward curves pricing still has -ve roll for belly/long-end rates that erodes protection slightly for longs.

- US Govvie inflows seem to have been short lived, small outflows, € govvies reported ~flat. US equity faced (modest) outflows ahead of earnings season, continuing last weeks moderation in inflows. Chinese equities continuing to see inflows.

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok