Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

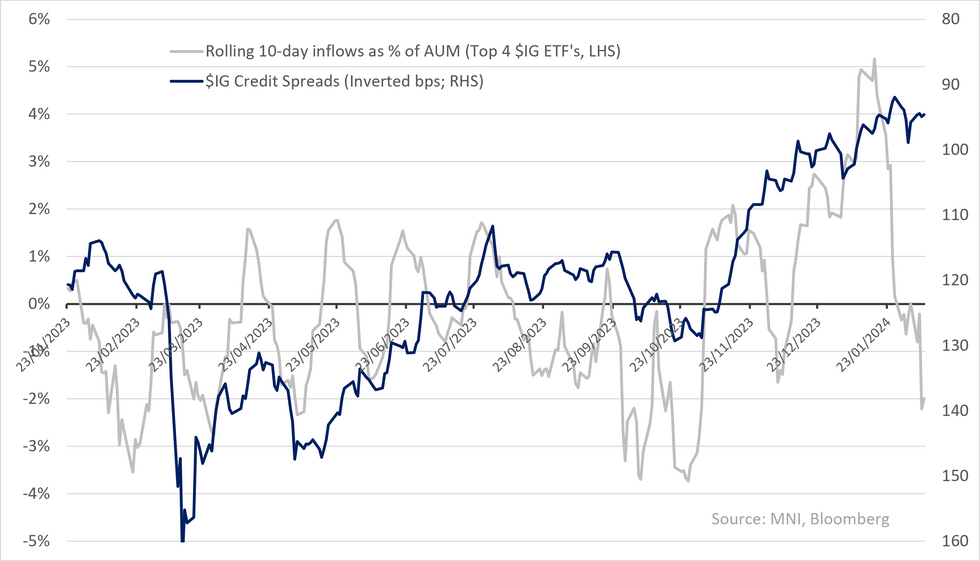

Seems €IG outflows over the week to Wed. were limited to ETF IEAC - net flows came in positive across both €IG/HY. $IG continued to see outflows as ETF's were showing - still at a relatively muted pace still with little impact on primary or secondary. Bloomberg reported trace data to yest. showed a pick up in tightening of primary issues in secondary (64% tightened this week up from 19% last week) - an impressive feat given (ex. APD) most came tight to secondary & broader secondary spreads traded flat this week. $HY & £IG flows were flat.

$IG ETF outflows yesterday continued at a relatively high pace (below). MTD issuance is at $43b (c$150b) leaving a slower ~$35b/week for the remaining 3 weeks to meet expectations. Higher rates post-NFP hasn't stopped $issuers this week (though supportive vol/macro backdrop) - still a risk supply accelerates on rates rallies from here. Similar story in €/£ - strong financials supply taking WTD to €28b (c€20b) - little impact on secondary headline spreads - fins underperforming corp's by 2bps this week noting we had bank earnings vol as well.

Outside of credit US equities reversed to relatively strong outflows, while Chinese equities saw very strong inflows on rumoured policy support - that's mirrored in secondary $ China corp spreads (-6bps) & equity performance (~+5%).

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.