Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

MARKET INSIGHT

Gas prices in Europe were the key driver of Bunds and gilts yesterday. Double digit price rises on the back of the colder weather and concerns about Russian supply (with the continued lack of inventory) have increased inflation concerns further.

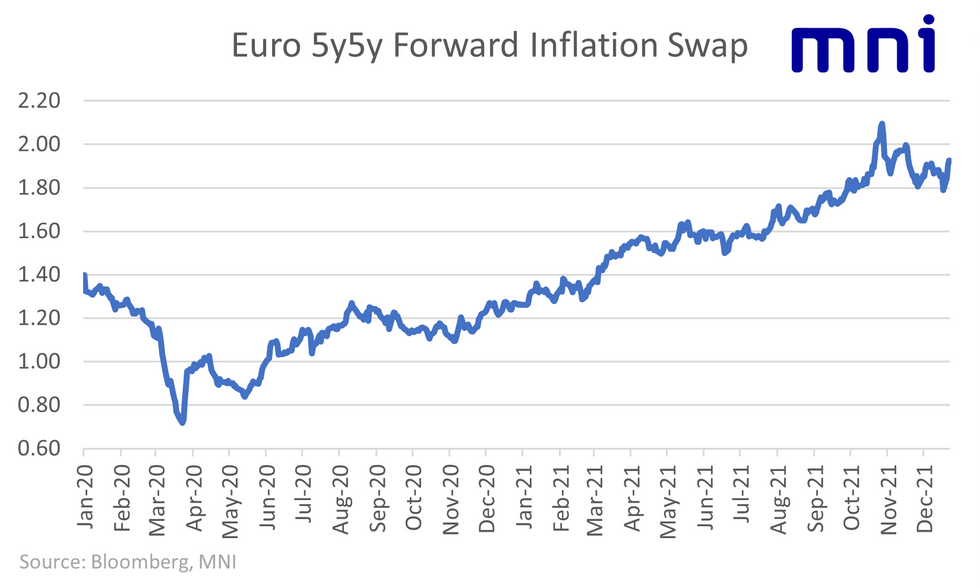

- Eurozone 5y5y inflation swaps saw their highest close since 7 December yesterday and hit an intraday high of 1.915%, not far off the top of their recent range (1.925% on 8 December). This is still some way off the 2.128% level seen in late October, and we have come off the highs this morning down around 3.8bp on the day (despite gas prices starting the day higher).

- The SONIA strip saw corresponding moves on the higher inflation outlook yesterday, with Greens/Blues seeing moves up to 13 ticks lower on the day, while the Euribor strip moved up to 5.5 ticks lower. The Eurodollar strip outperformed the SONIA strip, but underperformed moves in Euribor futures. Overnight moves have been more muted and marginally higher.

- Today we have a relatively light data calendar. We have already had UK GDP (which was revised up on the level but down on the quarterly growth rate for Q3) and we receive PPI from a number of European countries today. The highlight will be the third print of US GDP later today.

- With this in mind, there will be continued focus on political tensions with Russia, gas prices and any futher Omicron developments. Note that the Sun is expecting the UK to announce some post-Christmas Covid restrictions "before this weekend".

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok