Free Trial

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

IDR

USD/IDR is now less than 1% away from the 15000 level. Onshore spot closed yesterday at 14868. The pair hasn't spent much time above this level from an historical stand point, but the Indonesian authorities don't appear set to launch a rate defence for the currency today.

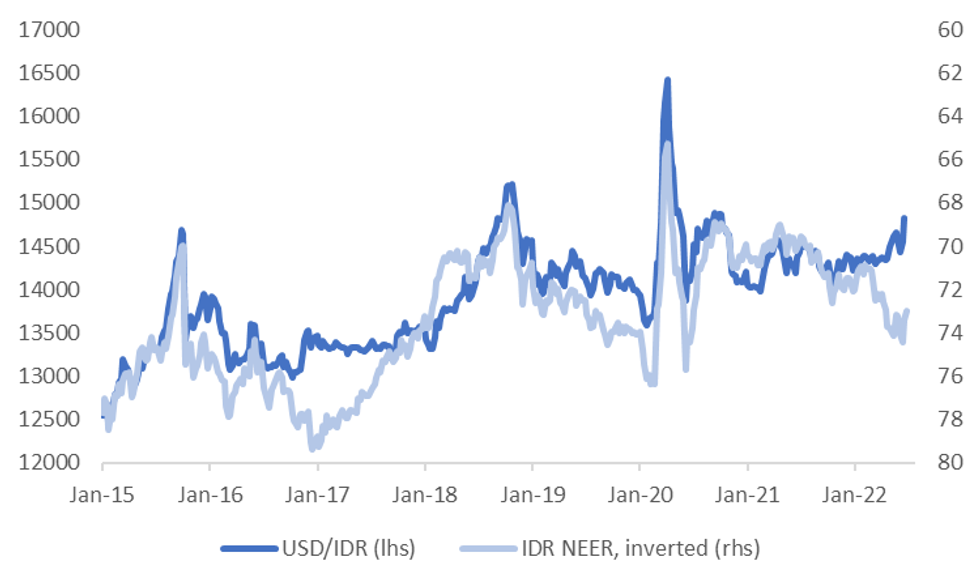

- A clear difference in the current context is IDR is still outperforming on a NEER basis. The first chart below plots USD/IDR spot against the IDR NEER, note that the NEER is inverted on the chart.

- Typically, bouts of USD/IDR strength coincide with NEER weakness as well. The current divergence reflects Indonesia's better terms of trade backdrop, which has driven trade surpluses and a much improved external position for Indonesia relative to past Fed tightening cycles.

- Such a backdrop has likely left BI more comfortable with the FX backdrop and less need to follow the Fed in lockstep.

Fig 1: USD/IDR Spot & IDR NEER Divergence

Source: J.P. Morgan, MNI - Market News/Bloomberg

Source: J.P. Morgan, MNI - Market News/Bloomberg

- Still, the best of the positive trade headwinds for Indonesia may be behind us. The outlook for broader commodity prices is growing gloomier given global recession risks.

- The market consensus also expects the current account position to slip back into a deficit this year, albeit a modest one (-0.2% of GDP).

- FX reserves have also fallen sharply despite this positive trade balance backdrop, $135.6bn versus the 2021 high of $146.9bn.

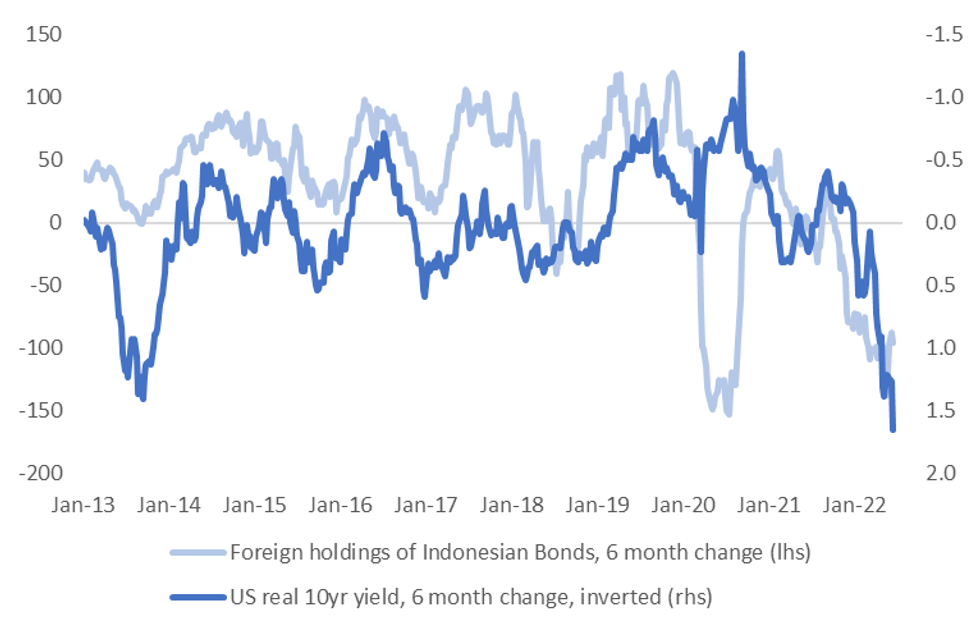

- There could also be more pressure for reserves via more outflows from local bonds by offshore investors. The second chart below overlays the 6 month change in foreign holdings against the 6 month change in the US real 10yr yield.

- Indonesia's real yield has slipped into negative territory, based off headline CPI and will decline further in coming months (absent domestic rate rises).

- The nominal ID-US 10yr spread is also sitting close to +400bps, a level we haven't spent too much time below from an historical standpoint.

- Whilst no change in BI rates is expected today (see our full preview here), a shift in the policy stance is unlikely to be too far away.

Fig 2: US Real Yield & Foreign Holdings Of Indonesian Bonds

Source: MNI - Market News/Bloomberg

Source: MNI - Market News/Bloomberg

Why MNI

MNI is the leading provider

of intelligence and analysis on the Global Fixed Income, Foreign Exchange and Energy markets. We use an innovative combination of real-time analysis, deep fundamental research and journalism to provide unique and actionable insights for traders and investors. Our "All signal, no noise" approach drives an intelligence service that is succinct and timely, which is highly regarded by our time constrained client base.Our Head Office is in London with offices in Chicago, Washington and Beijing, as well as an on the ground presence in other major financial centres across the world.

We are facing technical issues, please contact our team.

ok

Your request was sent sucessfully! Our team will contact you soon.

ok